The EU’s fossil fuel import dependency also extends to coal. However, while the EU imports nearly half of what it consumes, coal has been declining in the energy mix and now accounts for a minor share of total EU energy consumption as member states have increasingly switched to gas and renewables for electricity generation. Although there was an uptick in the EU’s use of coal during the 2022 energy crisis, this increase was sharply reversed again in 2023.

The EU’s high import dependency for fossil fuels can be very costly. In 2023, for example, high prices meant that the EU paid foreign fossil fuel suppliers, including Russia, €416 billion (a sum equivalent to 2.7 per cent of the EU’s GDP in that year).

Barriers to rapid scale-up of nuclear power

Nuclear power is a significant part of the EU’s energy mix, accounting for 24 per cent of electricity produced and 12 per cent of all energy consumed in 2024. The gas price shock following Russia’s full-scale invasion of Ukraine in 2022 sparked renewed interest in nuclear power. However, the prospects for a major expansion of nuclear power in the EU are poor. Only one reactor is currently under construction in the EU (although 12 more are planned, mainly in Central and Eastern Europe). Out of the 100 reactors in operation in the EU, more than four-fifths are over 30 years old and reaching the end of their operational lifetimes. The planned level of new builds is insufficient to replace capacity that is set to be retired, so the share of nuclear power in the EU energy mix will almost inevitably fall in the near term.

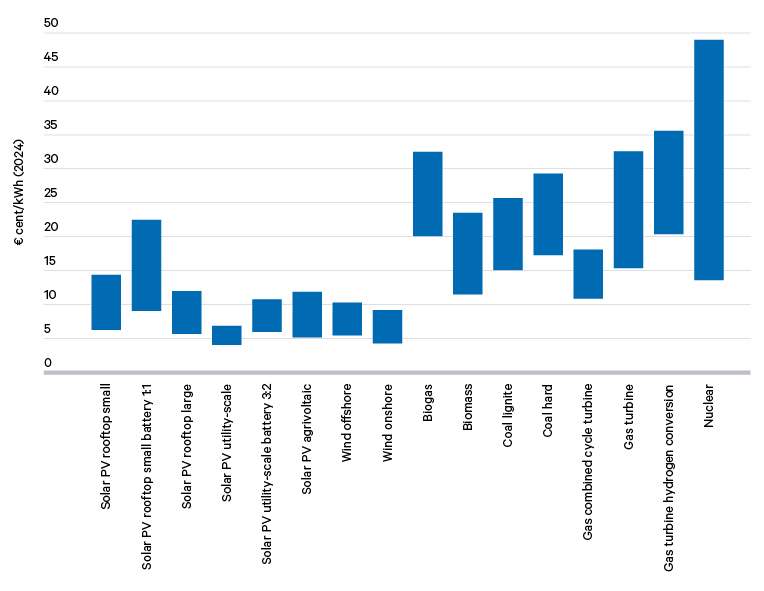

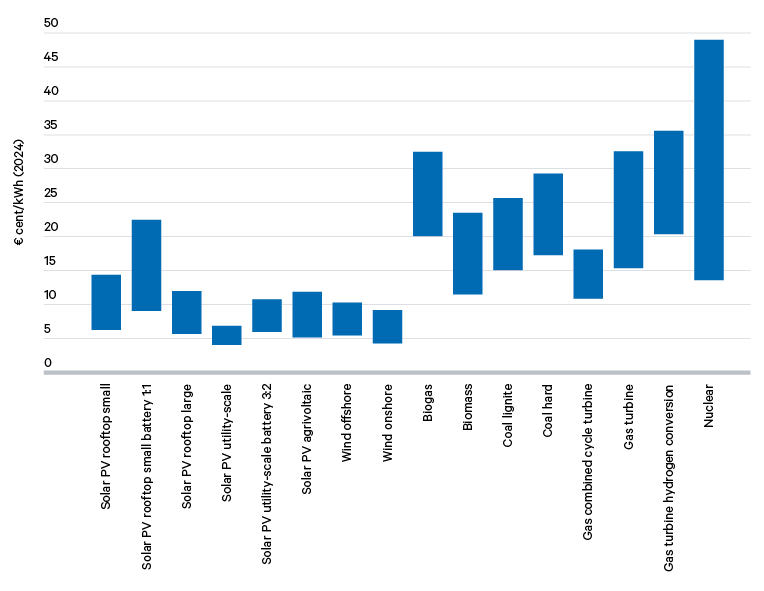

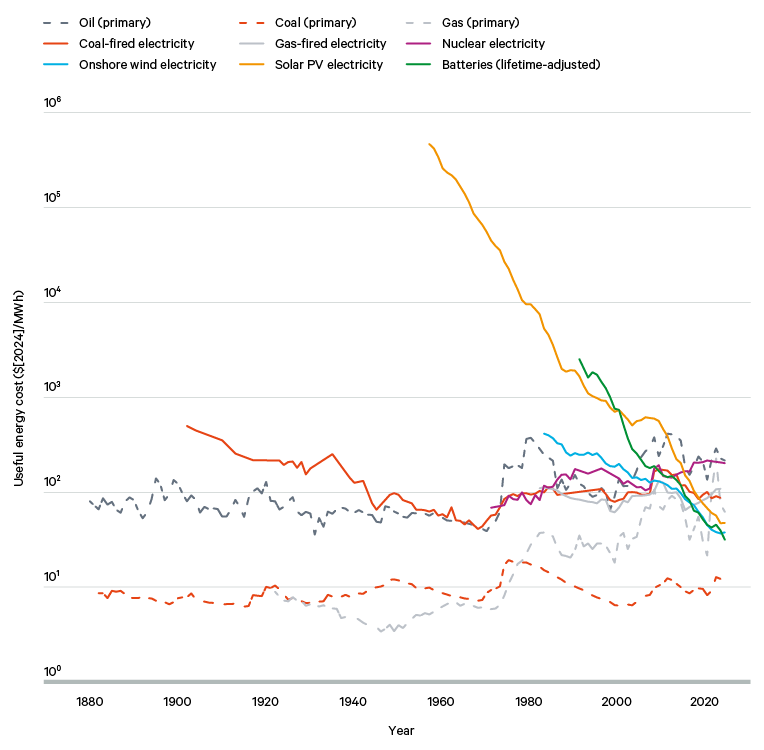

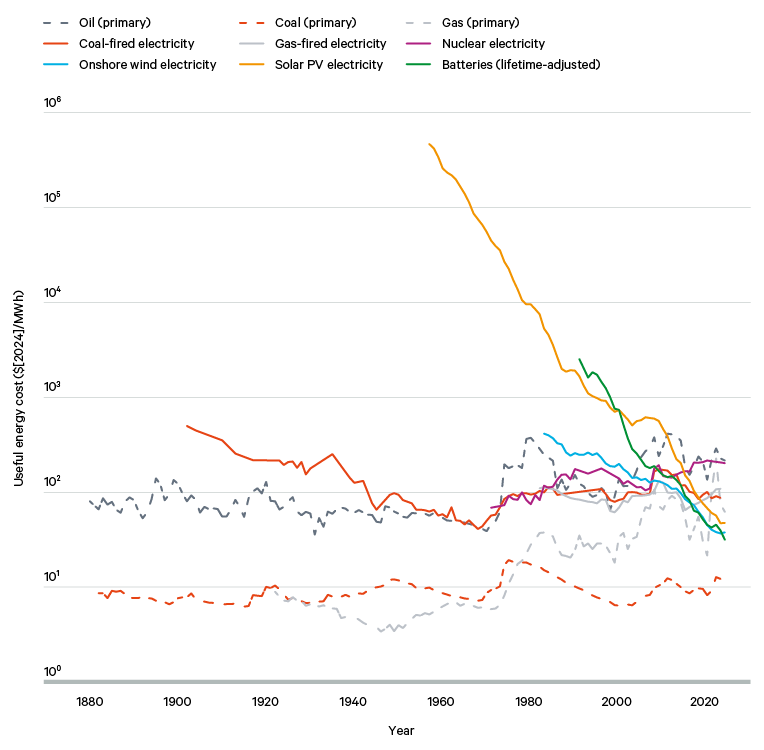

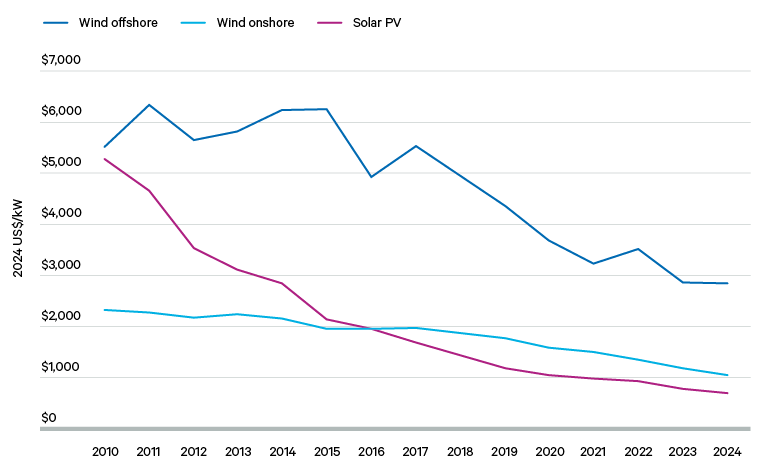

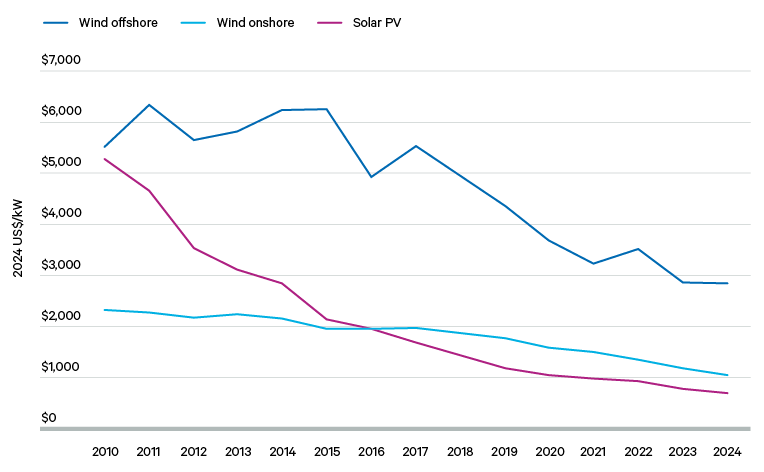

The primary obstacle to building new nuclear power stations in the EU is cost. A typical pair of reactors requires an investment of up to €50 billion. As this is far beyond what most utility companies are willing and able to provide, expansion of nuclear power necessitates significant, long-term support from taxpayers and/or electricity consumers for construction, financing, revenue stability and decommissioning. Consequently, the levelized cost of electricity (LCOE) from nuclear generation in the EU is much higher than for other sources: in 2024, the LCOE for nuclear power was $165/MWh, compared with $60/MWh for onshore wind and $50/MWh for solar PV. A 2025 article in the journal Energy, taking Finland as a case study, found that an energy system based on nuclear power would cost 71–84 per cent more in 2050 than a system based on renewables.

A related problem is the long timelines involved. Construction times for nuclear reactors have increased steadily since the first wave of projects in the post-Second World War period, when units were smaller and regulations were looser. Of the 69 reactors that began generation globally between 2015 and 2024, the average time between breaking ground on construction and the finished reactors being connected to the grid was 9.4 years.

Major time and cost overruns are common, usually as a result of repeated technical setbacks. The Flamanville 3 reactor in France began generating electricity in 2024, 17 years after construction had begun; it had originally been scheduled to open in 2012. Finland’s Olkiluoto-3 reactor opened in 2023, 18 years after the start of construction; it had been scheduled to open in 2009. Many nuclear power projects are cancelled: a 2025 study by Global Energy Monitor found that a quarter of all European nuclear power capacity ever planned ultimately never entered operation.

The advent of small modular reactors (SMRs) as a design innovation holds the promise of reduced costs and construction times. Several SMRs are in operation in China and Russia, but SMR development in Europe is at an earlier stage, with both technical and (above all) commercial hurdles still to be overcome. The European Commission hopes to deploy SMRs by the early 2030s, but acknowledges problems with ‘limited market uptake and slow commercialisation’ to date.

In the short to medium term, the simplest and most cost-effective means of maintaining – or at least slowing the decline of – the share of nuclear energy in the EU’s energy mix is likely to be through extending the lifetime of existing reactors, as Belgium is doing. However, this can only be sustained for so long.

Nuclear fuel supply is also an area of continued vulnerability, particularly given Russia’s importance to the markets for both natural and enriched uranium. The EU does not mine natural uranium but relies on imports. In 2024, the EU imported 34 per cent of its supply from Canada; the next largest source was Kazakhstan (24 per cent), followed by Russia (16 per cent), Australia (11 per cent) and Niger (8 per cent). Once imported, natural uranium is enriched at facilities within the EU. The supply of EU-enriched uranium met 64 per cent of EU demand in 2024, with the rest sourced primarily from Russia (24 per cent).

Five EU member states – Bulgaria, Czechia, Finland, Hungary and Slovakia – have Russian-designed reactors; the operators of these facilities rely on Rosatom, Russia’s state-owned nuclear company, for spare parts and maintenance.

Reliance on Russian technology and components is a further source of risk. Five EU member states – Bulgaria, Czechia, Finland, Hungary and Slovakia – have Russian-designed reactors; the operators of these facilities rely on Rosatom, Russia’s state-owned nuclear company, for spare parts and maintenance. The degree to which the use of Russian raw materials, equipment, technology and expertise is integral to the EU’s civil nuclear sector, combined with the long waits for alternative fuel supplies suitable for Russian reactors, means that the bloc is still effectively locked into nuclear energy relationships with Russia. For this reason, the European Commission’s plans to end Russian energy imports by the end of 2027 do not yet cover nuclear fuel and parts.

How renewable energy and electrification can contribute to energy security

In light of the above challenges and constraints, shifting to an energy system based on renewables and electricity offers the clearest path towards improved energy security. The principal benefits are outlined in more detail below:

Protection against supply shocks

Energy systems based on fuels (whether fossil fuels or nuclear) require a continuous flow of inputs. Trade interruptions can have immediate and costly impacts. For example, as gas prices spiked in the summer of 2022, EU governments spent €379 billion (2.4 per cent of GDP) that year on energy subsidies, up from €213 billion (1.3 per cent of GDP) the previous year. Energy systems based on renewables are not exposed to this risk. A sudden drop in imports of raw materials, components or finished products may disrupt manufacturing or deployment of new sources of generation, but it will not cause existing generation to be cut off abruptly. However, as with all systems based on electricity, supply can be interrupted if generation, storage or grid infrastructure fails, is remotely disabled, or is damaged or destroyed.

Protection against price volatility

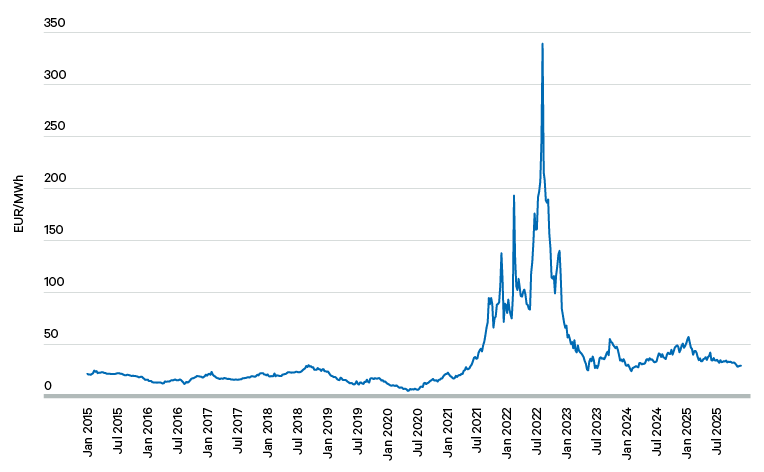

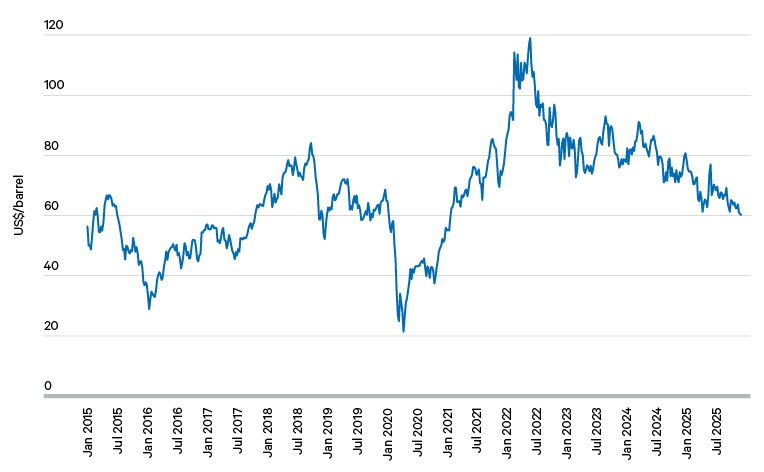

Gas and oil are internationally traded commodities, and their prices are highly sensitive to geopolitical turbulence. Both fuels have exhibited significant price volatility in recent years. As can be seen in Figure 7 below, gas price volatility – as well as the gas price itself – remains markedly higher for the EU than before the 2021–22 price shock. This is in large part a consequence of the EU’s forced move away from importing gas via pipeline from Russia, a move that has resulted in EU buyers competing with Asian buyers for shipments on the global LNG market.