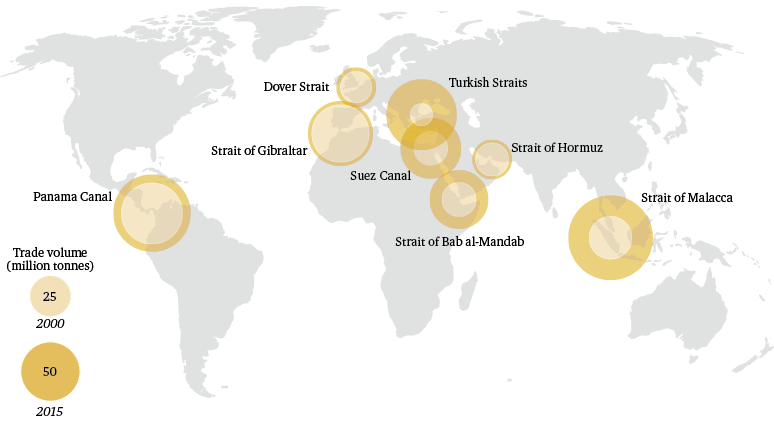

Growing international trade means that chokepoint dependency is likely to increase for the foreseeable future. Some chokepoints will come under more pressure than others. Rapid and continued growth in exports from the Black Sea region will increase dependence on the Turkish Straits, particularly for wheat. At the same time, sustained demand growth in China (averaging around 14 per cent a year for soybean imports over the past 15 years) will continue to increase shipments from crop exporters in the West via the Panama Canal and the Strait of Malacca.

Second, climate change is increasing the threat of disruption by acting as a hazard multiplier across all three categories of chokepoint risk. It will increase the frequency and severity of extreme weather, leading to more regular closures of chokepoints and greater wear and tear on infrastructure. Rising sea levels will threaten the integrity of port operations and coastal storage infrastructure, and will increase their vulnerability to storm surges. Climate change is expected to aggravate drivers of conflict and instability. It will also lead to more frequent harvest failures, increasing the risk of governments imposing ad hoc export controls.

Climate change may also increase the risk of concurrent supply disruptions. As extreme weather events become more common, the chances of coincidental disruptions occurring at different locations are likely to increase. Examples might include distant chokepoints being simultaneously disrupted by different weather systems, or a major chokepoint in one part of the world being closed during a harvest failure in a crop-growing region elsewhere. In such circumstances, market impacts are compounded. For example, if a hurricane comparable in ferocity to Hurricane Katrina in 2005 were to shut down US exports from the Gulf of Mexico at the same time as extreme rainfall rendered Brazil’s roads impassable (the latter happened in 2013), up to 50 per cent of global soybean exports could be affected. If this in turn occurred in conjunction with a Black Sea heatwave similar to the one recorded in 2010, around 51 per cent of global soybean shipments, together with 41 per cent and 18 per cent of global maize and wheat exports respectively, could be halted or delayed.

Chokepoint failures threaten to compound market fragility by contributing to higher costs and longer delays in delivery, and by making major supply disruptions more likely

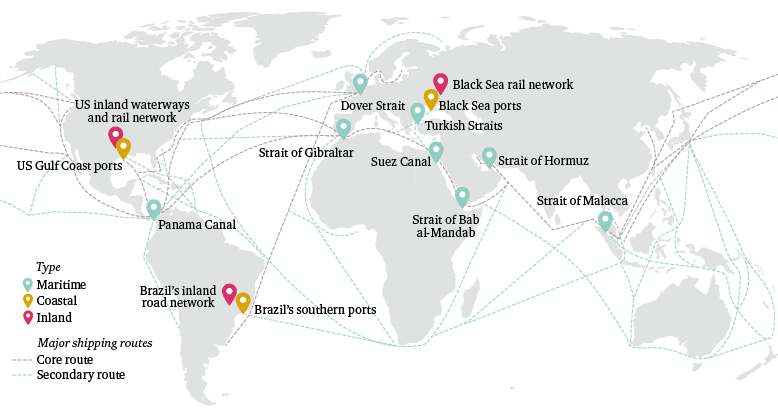

Third, chronic underinvestment in infrastructure is creating a double deficit – of capacity with respect to growing trade volumes, and of resilience with respect to climate change. The US’s inland waterways are old, congested, vulnerable to drought and flood, and likely to start failing in the near future; its Gulf Coast ports are vulnerable to hurricanes and storm surges. Brazil’s roads are poor and often rendered impassable by rain and subsidence. The Black Sea region requires significant investment in transport infrastructure, but regional instability is a deterrent to this. Each of the above-mentioned regions must mobilize significant investment in the coming decades to prevent bottlenecks and climate vulnerability worsening, but all face challenges in doing so.

The outlook for increasing chokepoint risk must also be understood in the context of mounting pressures on agricultural markets. Growth in cereal yields has fallen behind projected growth in cereal demand. Climate change is expected to exert a further drag on crop yields and become an increasingly destabilizing influence on global harvests. As a consequence, international markets are likely to become tighter and more volatile while dependence upon them increases. Chokepoint failures threaten to compound market fragility by contributing to higher costs and longer delays in delivery, and by making major supply disruptions more likely.

Which countries are most at risk?

Countries vary significantly in their exposure to chokepoint disruption. The criticality of a given chokepoint to a particular country depends not only on the share of imports that pass through it, but on how easily supply can be rerouted or secured through alternative means in the event of the chokepoint’s closure. For example, although almost 87 per cent of China’s grain and fertilizer imports are shipped through at least one maritime chokepoint, only 4 per cent pass through chokepoints for which no alternative route exists.

Conversely, just over a third of grain imports for the Middle East and North Africa (MENA) – the most food import-dependent region in the world – pass through at least one maritime chokepoint for which there is no alternative route. MENA countries rely on grain exports from the Black Sea, transported via Russian and Ukrainian railways and ports and on through the Turkish Straits; should these straits close for any reason, no alternative maritime routing option exists. This high degree of chokepoint exposure is compounded by proximity to the three Arabian maritime chokepoints (the Suez Canal, the Strait of Hormuz and the Strait of Bab al-Mandab), which determine market access for many countries in the region. Historical links between food insecurity and political/social instability make the region’s extreme exposure to chokepoint risk a particular cause for concern.

Structural vulnerabilities in poor countries amplify the potential consequences of chokepoint disruptions. In these countries, household spending on food and levels of pre-existing undernutrition are high, and the capacity of governments to respond is low. At the same time, the poor quality and limited extent of transport infrastructure – such as deep-water ports, railways and silos – in many developing countries also create local chokepoints and contribute to higher food prices.

Structural vulnerabilities in poor countries amplify the potential consequences of chokepoint disruptions

Among low-income food-deficit countries (LIFDCs), a cluster of African countries have high exposure to maritime chokepoints with no alternative routes. Many LIFDCs are also dependent on US exports and thus heavily exposed to US inland and coastal chokepoints. For example, Honduras sources 77 per cent of its maize imports and 88 per cent of its wheat imports from the US, and in Ethiopia the shares are 36 per cent and 27 per cent.

The risk of chokepoint disruption is by no means a concern for low-income countries alone. Japan and South Korea rank among the most exposed countries in the world, despite also being two of the richest. Though not considered food-insecure by traditional metrics, both countries rely heavily on food imports that transit one, two or three chokepoints. Just under three-quarters of Japan’s maize and wheat imports pass through the Panama Canal; and one-third of South Korea’s wheat and maize imports pass through the Suez Canal, Strait of Bab al-Mandab and Strait of Malacca.

Chokepoint risks are poorly understood and poorly managed

Despite their importance to the availability and price of food, chokepoints are systematically overlooked in assessments of strategic food security. This stands in marked contrast with analyses of energy security, where chokepoint risk has been a key consideration for years and international governance mechanisms have emerged to manage it.

The most obvious exception to this picture is China, which is acutely aware of its exposures. It actively invests in overseas infrastructure to relieve pressure on existing chokepoints (e.g. as a major investor in Brazilian infrastructure); to diversify supply routes (e.g. through construction of a railway across South America to lessen reliance on the Panama Canal); and to increase its operational footprint along its supply chains (Chinese companies are ubiquitous owners and operators of ports and trans-shipment hubs).

However, the lack of cooperative approaches for dealing with food chokepoint risk is troubling, as it raises the prospect of uncoordinated, unilateral responses as states scramble to secure supply in the event of a major disruption, deepening the crisis as they do so.

Recommendations

Reducing chokepoint risk in the food system is a long-term project. New institutional and governance arrangements need to be negotiated and implemented at international and national level, existing infrastructure strengthened and new infrastructure built. Work must begin now for the necessary measures to be in place before climate change becomes a major source of disruption and instability. This report proposes five areas for action.

1. Integrate chokepoint analysis into mainstream risk management and security planning.

If supply chain risks are to be managed effectively, analysis of chokepoint dependence and chokepoint risk needs to be incorporated into risk management and security planning across a range of sectors – food security, national security, disaster risk management – at international, national and subnational level.

The United Nations (UN) should identify critical food security corridors around which memoranda of understanding may be developed for the protection of critical food trade through maritime chokepoints in the event of a disruption.

The United Nations should identify critical food security corridors

Governments in food-importing countries should undertake assessments of exposure and vulnerability to chokepoint risk at the national and subnational level. This process should be led by government agencies, in collaboration with international organizations such as the World Bank and UN Food and Agriculture Organization (FAO), bringing in donor agencies where appropriate.

Donor governments should commit funding to develop infrastructure disaster resilience strategies with national governments, agencies and a range of stakeholders to ensure effective coordination in disaster response and to mitigate negative food security outcomes.

Governments in at-risk countries should share knowledge, to the extent that it exists, on chokepoint risk assessment and management. One historical example was the US’s sharing of lessons learned, in terms of disaster response and recovery strategies, with other climate-vulnerable nations following Hurricane Katrina in 2005. These lessons were then used to inform the development of those countries’ own national contingency plans.

Providers of food security indicators should incorporate chokepoints in their analyses. For example, food security assessments produced by the FAO, the World Bank, the Famine Early Warning Systems Network (FEWS NET), the Economist Intelligence Unit and Maplecroft should take account of chokepoint risk.

2. Invest in infrastructure to ensure future food security.

This report argues that one of the biggest risks to agricultural trade is a lack of adequate infrastructure. Closing the infrastructure gap is not simply a question of more construction; new developments must be able to withstand increasingly hostile weather as they age.

The G20 should establish a taskforce on climate-compatible infrastructure. Building on the work of the Global Infrastructure Hub and the Task Force on Climate-related Financial Disclosures, the taskforce should establish common principles and guidelines for critical infrastructure that is resilient to future climate impacts.

The G20 should establish a taskforce on climate-compatible infrastructure

Governments should set up national-level independent infrastructure committees to advise on investment and policy decisions relating to major transport infrastructure. These committees should be cross-government in structure and should sit outside of parliamentary cycles to ensure a long-term, cross-sectoral perspective.

Multilateral development banks should prioritize investment projects that diversify food supply sources when taking decisions on funding – whether for regional trans-shipment hubs, transport infrastructure to boost market connectivity and support ‘multimodality’, or strategic reserves and storage infrastructure.

Governments should adopt a ‘landlord’ model of public ownership and private concessions for critical infrastructure in countries in which state-owned railways, roads, waterways or ports are failing as a result of poor management or underinvestment.

Governments in major food-exporting regions facing infrastructure financing deficits should seek strategic ‘win-win’ investment partnerships with key trading partners willing to finance infrastructure to relieve pressure on inland and coastal chokepoints.

International financial institutions and donors should continue to invest in agricultural extension services, agricultural research and development, and the cultivation and scaling up of alternative crops to support a diversified grain production base (particularly for crops with a relatively high tolerance to climate stresses) and so reduce exposure – both at national and systemic level – to chokepoint disruption.

3. Enhance confidence and predictability in global trade.

New governance measures are needed to counter the contagious spread of export controls – such as those seen during the 2007–08 food crisis. Where possible, policies and investment should promote the diversification of the global grain production base, and reduce dependence on a small number of exporting regions and their inland and coastal chokepoints.

The World Trade Organization (WTO) should instigate a process to continually reduce the scope for export restrictions. An outright ban on such restrictions would be ideal; a less ambitious approach could include clarifying and strengthening WTO rules to make it harder for governments to introduce ad hoc policies.

Developed food-exporting countries should reform trade-distorting farm support. Such support promotes systemic reliance on a handful of mega-crops and a small number of grain-exporting regions. Instead, public funds should be directed to supporting alternative sources of grain production around the world, in order to diversify global production and reduce import dependence elsewhere. A priority should be to direct such funding to farming in sub-Saharan Africa, where yield gaps remain while cereal demand is growing rapidly; this could be complemented with funding to support production of alternative crops.

4. Develop emergency supply-sharing arrangements and smarter strategic storage.

Strategic reserves, and provisions for their release and distribution at times of supply shortage or when prices are rising, are critical to managing chokepoint risk. However, unlike oil markets, no international institution exists to manage the risk of a major supply interruption in agricultural markets.

The FAO, UN World Food Programme (WFP) or Agricultural Market Information System (AMIS) should establish an emergency response mechanism among major players in the global food trade, modelled in part on that of the International Energy Agency in oil markets, to agree rules on coordination during acute market disruptions, including on the release and sharing of stocks and on measures to relax ‘biofuel mandates’.

Grain-trading partners should pursue collaborative arrangements to store grain in destination markets – that is, beyond the location at which chokepoints could interrupt supply. This would involve exporting countries entering into extra-territorial storage agreements with importing countries – whereby the exporter stores grain in the importing country – to provide assurance over availability in the event of supply dislocations. Agreements would need to specify emergency access rights and pricing arrangements.

Governments in food-deficit regions should agree storage and emergency sharing arrangements at regional level

At-risk countries – such as those in the Horn of Africa and the MENA region – should ensure sufficient domestic stocks are available to meet needs during plausible worst-case supply disruptions. Where government capacity to manage stocks is lacking, arrangements to outsource stockholding at target levels to the private sector could be explored.

Governments in food-deficit regions should agree storage and emergency sharing arrangements at regional level to reduce collective vulnerability to chokepoint disruption. Facilities should be positioned strategically to bypass potential blockages and to spread the risk of damage or obstruction.

5. Build the evidence base around chokepoint risk.

Strengthening the evidence base around the importance of chokepoints to food security, and enhancing understanding of the nature and severity of disruptive hazards, are key first steps in the translation of chokepoint analysis into policy. These steps will require both new avenues of research and new modes of thinking about critical infrastructure.

Researchers should connect existing models of transport network dynamics with real-time food trade data to enable the modelling of rerouting options in cases of major disruption to maritime or coastal chokepoints. Expanded data functionality could provide the basis for the development of disaster management strategies. Where data are not open-source, research councils should support partnerships between the private sector and the research community that advance understanding of chokepoint risk while protecting commercially sensitive data.

AMIS should work with governments to harmonize nationally reported, macro-level transport infrastructure and asset data

AMIS should broaden its scope to include systemic chokepoints. An expanded remit should include risk assessment relating to the capacity and performance of systemic chokepoints, and evaluation of potential disruptions to them. In addition to raising awareness of chokepoint-related food security risks, such an initiative would promote the monitoring, disclosure and harmonization of data at national level, ultimately supporting better risk management.

Multinational institutions should integrate ongoing monitoring of chokepoint congestion and failures within existing frameworks for tracking infrastructure investments and infrastructure performance, to inform the identification of investment priorities. Examples of frameworks that could be adapted for this purpose include the OECD’s International Transport Forum (ITF) and the World Economic Forum’s Global Competiveness Report.

AMIS should work with governments to harmonize nationally reported, macro-level transport infrastructure and asset data, and to track spending and performance in the sector as a means to inform and attract multilateral and private-sector financiers.

Climate scientists and infrastructure industry associations should bridge the gap between climate impact modelling and infrastructure resilience planning, through industry-led dialogues that centre on the needs and constraints of infrastructure operators, and that support the downscaling of climate projections to sub-regional or project level.

Research councils and other funders should establish multidisciplinary frameworks to encourage the research community to address key knowledge gaps in the fields of food security, transport networks, disaster resilience, infrastructure development, infrastructure governance, risk assessment and climate science. Research is most urgently needed on at-risk food-importing regions and climate-exposed food-supply hubs.