3.1.1 Weather and climate hazards

Weather poses both acute and chronic threats to the smooth operation of chokepoints. The cumulative impacts of high and low temperatures, heavy rainfall, drought, high winds, storms and storm surges can reduce the efficiency, integrity and capacity of transport infrastructure, potentially leading to temporary but severe disruptions.

Climate change will have a multiplying effect on weather-related hazards. While changes in average temperature and rainfall are expected to unfold gradually – and may lessen weather risks in certain regions – these changes are predicted to have a compounding and non-linear effect in terms of their contribution to extreme weather conditions and acute events. By way of example, researchers estimate that a sea-level rise of one metre would render a one-in-100-year flood event in the Indian city of Kolkata 1,000 times more likely.

Weather poses both acute and chronic threats to the smooth operation of chokepoints

Over time, weather-induced wear and tear heightens infrastructural vulnerability to extreme climate events, which themselves are expected to intensify in severity and frequency as climate change progresses. Shorter intervals between extreme events may make both routine maintenance and disaster recovery more challenging, and limit the time available to prepare for the next shock. In the absence of efficient and robust response and recovery plans, each high-impact event may have a compounding impact upon the next, undermining both the short-term and long-term integrity of physical structures.

3.1.1.1 Rainfall extremes

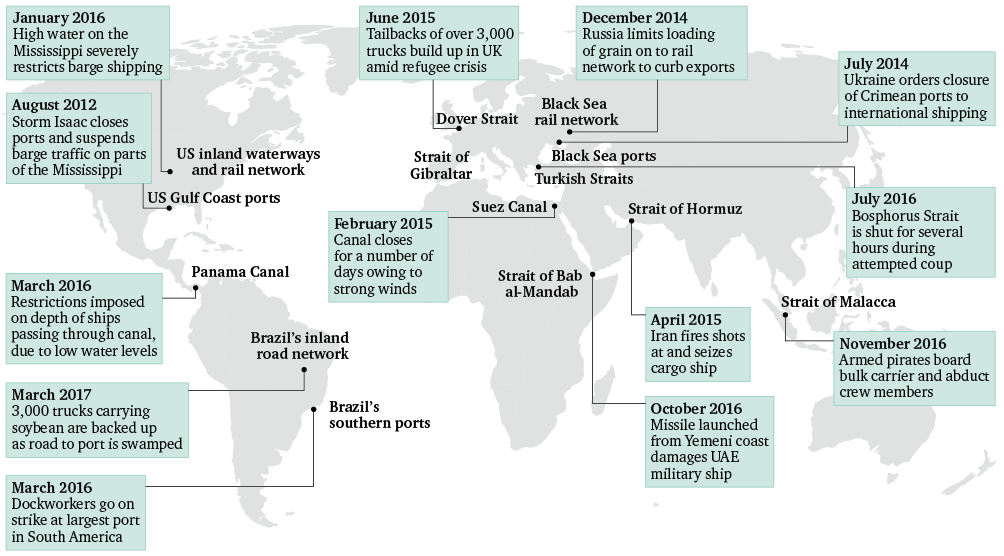

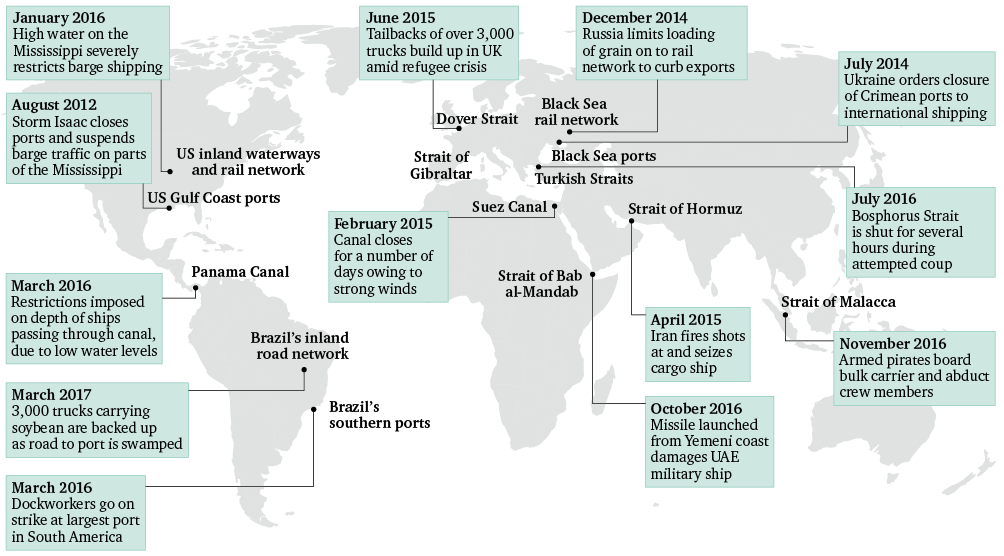

Heavy rainfall and surface flooding pose a risk to port infrastructure and storage facilities. Impacts will be greater where options for shifting trade to other modes of transport and export routes are limited. For example, in the case of disruption to US waterways, congestion on roads and railways could limit the scope to transport grain exports by truck or train. Flooding and drought as a result of climate change are forecast to bring more regular interruptions to trade along US transport corridors; the 2012 drought that caused water levels along the Mississippi to fall to record lows severely delayed the delivery of fertilizers to farmers in the Midwest. Extremes in rainfall also pose an operational hazard to man-made canals: a particularly strong El Niño event in the spring of 2016 brought long periods of dry weather to Central America, causing water levels to drop in the Gatún and Miraflores lakes either side of the Panama Canal and leading to the introduction of depth restrictions that affected nearly a fifth of vessels using the canal.

3.1.1.2 Sea-level rise

Climate change will result in higher sea levels due to thermal expansion of the oceans and meltwater from glaciers and ice sheets. Considerable uncertainty surrounds the modelling of sea levels, but the best available science anticipates a global rise of 0.44–0.74 metres above 1986–2005 levels by 2100. It is important to note that this may be an underestimate, given the potential for non-linearities and tipping points to create faster change than many models currently capture.Higher sea levels will lead to more damaging storm surges that threaten port and coastal structures. The port of New Orleans on the US Gulf Coast and the Dutch port of Rotterdam, northeast of the Dover Strait, are among the most exposed to storm surges and high winds in terms of at-risk asset value and population size, while the integrity of coastal structures in Brazil, including major port areas, is expected to be compromised by climate change impacts on wave height and sea level.

3.1.1.3 Tropical storms

While storm activity is influenced by a range of factors, available evidence suggests that rising ocean temperatures are likely to bring more frequent and severe storms and tropical cyclones. Stronger storms are likely to combine with higher sea levels to produce more severe storm surges and greater damage to infrastructure. Climate change may bring cyclone activity to the Strait of Hormuz. Meanwhile, ports along the Gulf Coast of the US are already exposed to tropical cyclones. An assessment of the economic risks posed by climate change to US infrastructure envisages up to US$50.6 billion worth of annual coastal storm damage being wrought on Florida’s infrastructure within 25 years.

The integrity of coastal structures in Brazil, including major port areas, is expected to be compromised by climate change impacts on wave height and sea level

3.1.1.4 Climate change as a hazard multiplier

Climate change is likely to aggravate socioeconomic and political risks. Extreme weather events and more frequent harvest failures are expected to increase human displacement, indirectly amplifying the risks of inter-group violent conflict and civil war by exacerbating conflict drivers such as poverty, economic shocks and localized resource scarcity. As coastlines and maritime borders are redrawn by rising sea levels, the risk of territorial disputes may increase. Climate-induced food supply shortages may prompt the more regular imposition of unilateral trade measures. One preliminary analysis found that a global agricultural production shock that would have been defined as a one-in-100-year event in 1951–2010 could become a one-in-30-year occurrence by 2040, increasing the risk of export bans and food price crises.

3.1.2 Security and conflict hazards

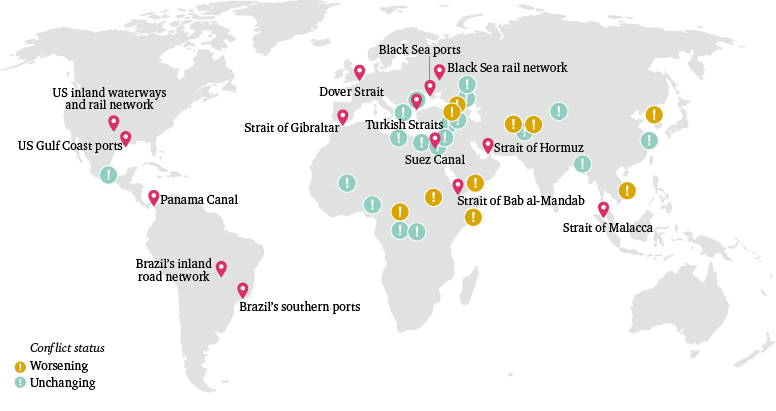

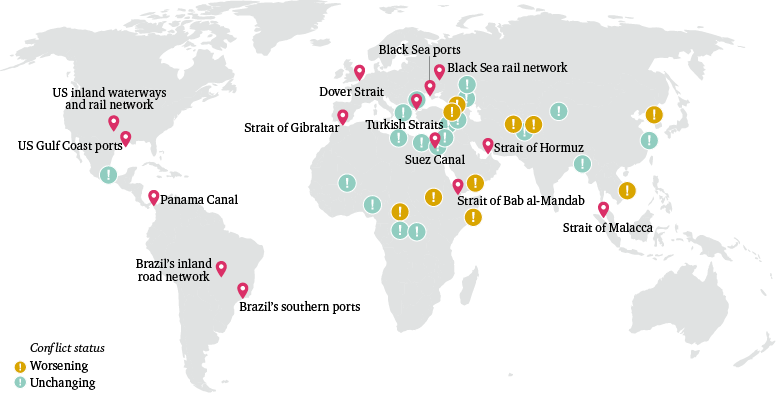

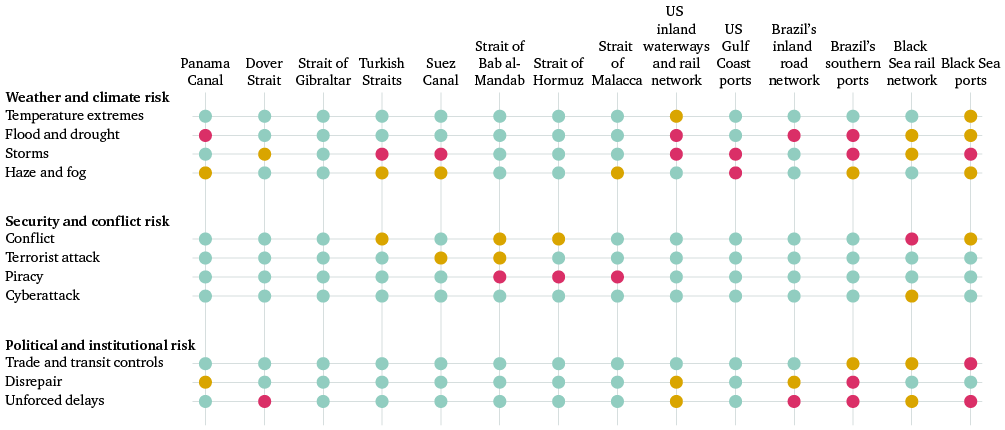

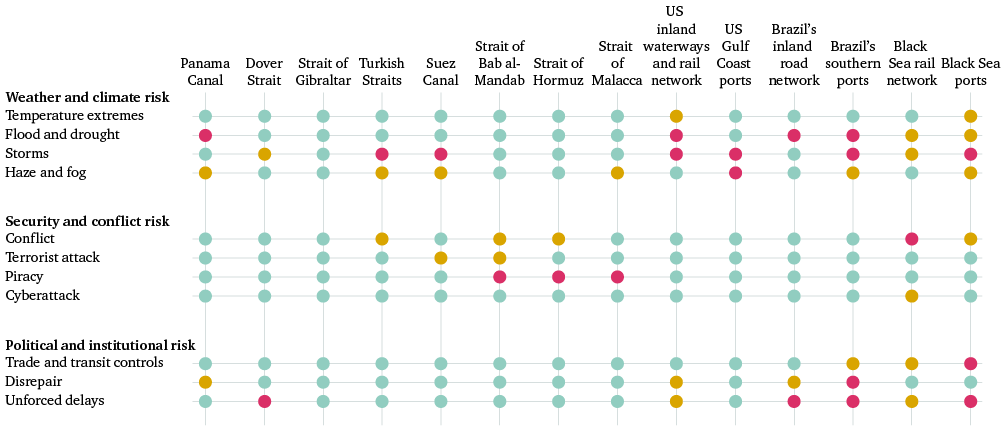

Transnational trade routes for critical resources often involve transit through conflict-affected or weakly governed areas, with the result that certain chokepoints are at risk from instability (see Figure 20). For example, the Suez Canal, Turkish Straits, Strait of Bab al-Mandab, Strait of Hormuz and ports in the Black Sea all border on, or are located in, states for which the Fund for Peace has issued a warning, alert or high alert about the possibility of state failure.

As well as having direct impacts on operations and infrastructure, political and social instability can affect chokepoints indirectly. For example, ongoing conflict has troubled potential investors in the Black Sea; in 2014, foreign direct investment (FDI) in the Black Sea region was less than 2 per cent of GDP, and gross foreign investment had fallen to its lowest level since 2008. Populations displaced by conflict can also disrupt chokepoints. For example, migration across the Dover Strait in 2015 and 2016 caused traffic restrictions and border force strikes, leading to delays and higher transport costs for industry.

3.1.2.1 Armed conflict

Globally, the incidence of armed conflict appears to be in long-term decline: the number of active conflicts worldwide fell from 63 in 2008 to 40 in 2015, though wars have also become more intense. Despite this global trend, it is reasonable to assume that certain regions will remain vulnerable to conflict for the foreseeable future, with implications for the security of particular chokepoints. The risk of conflict in the Middle East will remain, for example, with continued implications for the security of the Arabian chokepoints. Terrorist attacks in Egypt’s Sinai Peninsula, to the east of the Suez Canal, are becoming more common. The war in Yemen persists, with little hope for imminent peace. And the risk of armed conflict in Turkey is non-trivial: the country shares borders with conflict-ravaged Syria and Iraq; there has been a recent upsurge in terrorism in the region; and a recent coup attempt and subsequent crackdown in Turkey itself have highlighted concerns about stability. Moreover, the potential for an escalation in tensions between Turkey and Russia remains (see Box 5). Each of these factors has implications for the security of the Turkish Straits.