It is critical that the Angolan authorities get a full picture of the efficiency shortcomings of past major investments, and that bold reforms are undertaken to make public investment more efficient.

Policy, Governance and Reform

Research paper

Published 14 September 2018

Updated 11 December 2020

ISBN: 978 1 78413 264 4

It is critical that the Angolan authorities get a full picture of the efficiency shortcomings of past major investments, and that bold reforms are undertaken to make public investment more efficient.

This chapter outlines the origins of Angola’s post-war fiscal situation. It illustrates how the government prioritized infrastructure investments and allocated significant public resources to infrastructure projects. Using the energy and transport sectors as examples, the chapter assesses what Angola gained from its investments, and whether objectives were set and achieved. While analysis is constrained by the limited availability of disaggregated data detailing infrastructure investments and outputs, it has been possible to gather sufficient data to provide a sense of the limited results achieved in these two sectors.

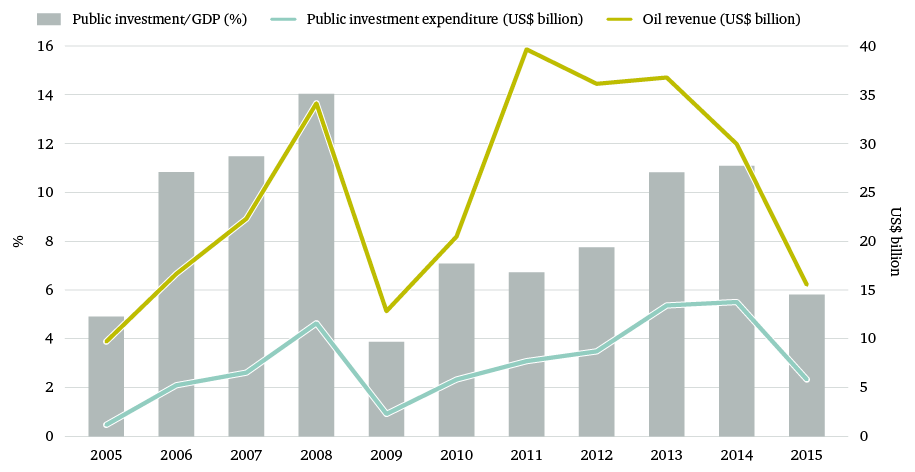

Official figures for government revenue show that, between 2006 and 2015, the country collected a staggering US$267.2 billion in oil-related receipts. This sum includes taxes collected directly from oil companies, as well as proceeds from the state-owned oil company, Sonangol.7 As can be seen in Figure 1, the revenue stream was volatile even in the years generally characterized by high oil prices. Nonetheless, on average the government secured around US$27 billion per year during the decade. By comparison, the entire sum of development aid provided to Africa in 2013 amounted to US$55.7 billion.8 In the same year, Angola’s oil revenue was US$37.1 billion.

In addition to receiving oil revenue, the Angolan government negotiated a series of credit lines with Chinese financial institutions. These credit lines were used predominantly to finance infrastructure investments.9 While the arrangements were substantially less transparent than public-sector oil revenues, it is known that the most recent extension of such credit lines was negotiated during an official visit by President dos Santos to China in October 2015, when a reported US$6 billion was promised. If accurate, this would bring the accumulated stock of debt under Chinese credit lines to US$35 billion, a sum corresponding to an average of roughly US$3 billion per year over the preceding decade.10

These figures confirm that Angola has been effectively awash with cash since the mid-2000s, a situation that in turn raises important questions about governance. Analysis of Angola’s oil-driven boom and the implications for infrastructure development must consider best practice in management of revenues derived from exhaustible natural resources. Options range from using the money to clear government debts and invest in physical assets on a ‘spend as you go’ basis to creating funds for stabilization or pure saving/investment purposes. In the early post-war years, the government took a relatively cautious approach, with public investments not exceeding 6 per cent of GDP. However, amid rising oil prices and mounting pressures on the ruling People’s Movement for the Liberation of Angola (MPLA) to demonstrate tangible economic progress before the country’s first post-war elections, the government increased spending steeply. At the same time, an ever-larger share of resource revenue was spent rather than saved or prudently managed. Given that oil prices during this period exceeded relatively conservative budget estimates, the government ended up collecting more revenue than anticipated. In 2003–05, the government spent 40 per cent of this excess revenue and saved 60 per cent. However, in 2006–08 spending was equivalent to 140 per cent of excess revenue, which resulted in a growing budget deficit.11 In other words, there was a marked shift away from the relatively cautious fiscal approach of the early post-war years.

The post-civil war infrastructure investment boom can be broken down for analytical purposes into three distinct periods: the early post-war years of 2002–05, when US$4.2 billion (US$1.1 billion per annum) was spent; the mid-post-war years of 2006–09, when US$26.9 billion (US$6.7 billion per annum) was spent; and the late post-war years of 2010–15, when US$56.3 billion (US$9.4 billion per annum) was spent.12 In total, spending amounted to US$87.5 billion, corresponding to roughly a third of oil revenue.13 As Figure 1 illustrates, the rise in investment not only coincided with rapid GDP growth but was also a function of the increased role of public-sector capital spending in the economy. As a share of GDP, public investment increased sharply between 2005 and 2008, peaking at 14 per cent. The global financial crisis led to public investment plummeting to 4 per cent of GDP in 2009, before a gradual recovery to 11 per cent of GDP in 2014. Figure 1 also clearly suggests that fluctuations in oil revenue were a factor in determining levels of infrastructure investment.

In 2011, an ambitious study of infrastructure development in Angola was published as part of the World Bank-led Africa Infrastructure Country Diagnostic (hereafter referred to as the ‘AICD study’) project.14 The study found that, although Angola’s infrastructure needs were considerable, a ‘basic infrastructure platform’ could be established by investing US$2.1 billion per year for a decade, with 70 per cent of the overall amount required for capital investments and 30 per cent required for maintenance. The study also claimed that meeting Angola’s infrastructure needs would entail spending in the region of 7 per cent of GDP,15 compared with an average of 14.5 per cent in sub-Saharan Africa as a whole. However, the AICD study warned that Angola’s infrastructure investment strategy was skewed towards transportation projects. It also identified massive inefficiencies that have raised actual infrastructure spending to around US$4.3 billion per year, or around double the estimated amount needed. As illustrated above, actual spending since 2011 seems to have exceeded even these figures by some distance; according to the AICD study, Angola should have been able to satisfy its infrastructure needs both in terms of investments and maintenance, yet could not do so.

Documenting what Angola gained from its investments in infrastructure in the first 15 years after the end of the civil war is complicated by the difficulty of accessing detailed public spending data. Most of the necessary data are not publicly available, and in some cases the data probably do not even exist due to poor record-keeping and the practice of significant off-budget spending (e.g. through credit lines and investments through Sonangol). It is useful, nonetheless, to review such data as are available for different sectors in order to piece together a partial picture of what has been achieved. The data provide a sense of the limited value for money that most investments in Angolan infrastructure have delivered, as well as illustrating the need for more transparency. For the purposes of this paper, the analysis of public spending focuses on the energy and road sectors, as these have been given high priority by the government.

Periodic two-year government plans, beginning in 2003–04 and repeated until 2008, outlined a substantial commitment to investments in numerous sectors, including transport, energy and water. These documents set benchmarks for project success or failure, which typically consisted of indicators such as sector investment levels, sector growth and numbers of jobs created.16

The National Development Plan (NDP) for 2013–17 has taken the commitment demonstrated in earlier government plans a level further: covering a five-year rather than two-year period, it is based on an analysis of socio-economic developments in 2007–12, an assessment of the international economic outlook, and a macroeconomic framework. It outlines medium- and long-term national objectives, as well as 11 specific policy areas on which successful implementation depends. Relatively detailed objectives and indicators are set out on a sector-by-sector basis. The NDP includes 20 transformative projects (projectos estruturantes) with designated national priority status, costed at US$50.7 billion in total. In addition, three clusters of projects are earmarked for private investments valued at US$10.1 billion. The cost estimates are highly aggregated, however, which makes it difficult to assess if they are realistic. The NDP also outlines a medium-term development expenditure framework and a financing strategy, although neither is sufficiently detailed.

Despite the NDP’s relatively extensive scope and attempt at prioritizing activities, it has no explicit connection to the PIP, which is the key policy instrument to inform the government’s annual budgeting process and determine the level of government spending on public investments. The NDP has proven to have overambitious targets relative both to the capacity of the public administration to implement and oversee plans, and to the capacity of the private sector to deliver. Since 2015, financing has also become an issue as the economic and fiscal crisis has greatly reduced revenues that could be used for financing public investments.

The government still does not publish information about completed infrastructure projects, their final costs, or the extent to which they deliver the benefits expected of them.

Although the detail and quality of data on infrastructure investments have improved in the past few years, more needs to be done. The government still does not publish information about completed infrastructure projects, their final costs, or the extent to which they deliver the benefits expected of them. Annual budget execution reports, published from 2010 onwards, disclose the level of actual expenditure versus the budgeted figure in each year. The reports indicate that the level of actual spending achieved has varied from 30 per cent of that budgeted in 2009 to 97 per cent in 2011 and 2012, and back down to 48 per cent in 2014 – the reduced 2014 figure reflected the fact that the PIP was the first programme to be halted as revenue dropped. Figures on the overall amount of money spent do not, however, reveal anything about the number of infrastructure projects completed or their final costs. Although quarterly implementation reports document progress against objectives in the NDP, these are produced exclusively for the government. They are not even shared with parliament, which is consequently unable to perform its duty of holding the executive to account. However, the 2013–17 NDP does provide some indications of achievements up to 2012, as well as the level of ambition for the next five years.

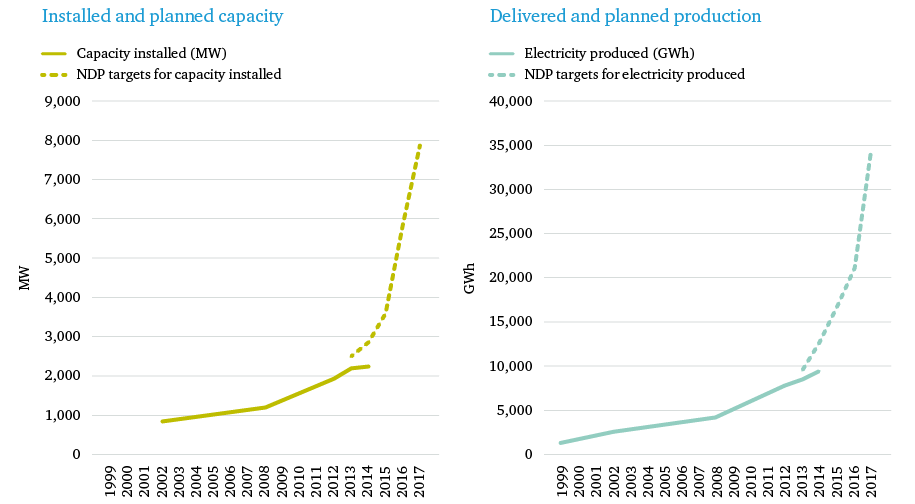

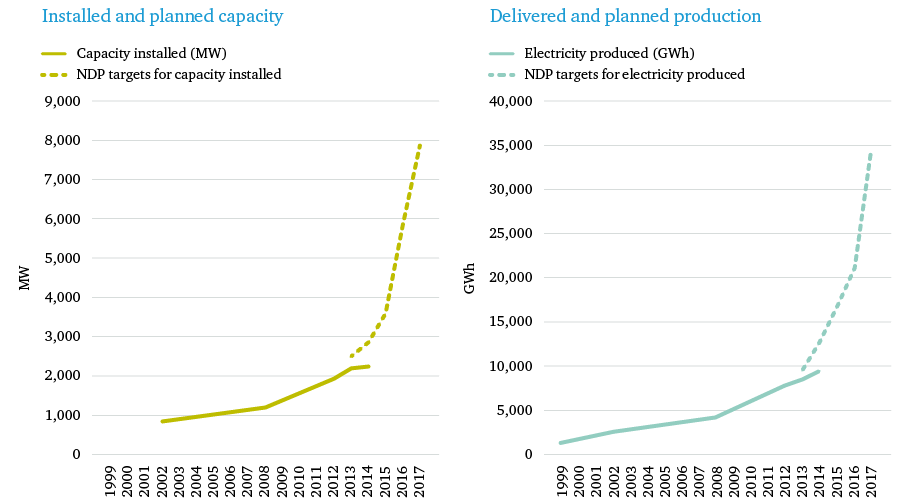

The energy sector in Angola is underdeveloped, with only 30 per cent of the population having access to electricity in 2015.17 There is huge potential for hydropower, solar power and natural gas-based generation, and expanding production has been one of the biggest priorities of the government over the past decade. Generation capacity and production have both increased massively, thanks to investment valued in the tens of billions of US dollars – although capacity and production have still fallen short of the targets in the NDP. Generation capacity rose from around 830 MW in 2002 to 2,230 MW in 2014, slightly lower than the levels in Mozambique (2,682 MW) and Zambia (2,452 MW). However, installed capacity in all three countries is dwarfed by that in South Africa (46,963 MW).18 A high proportion of Angola’s generation capacity is operational, and the country produced an estimated 4,133 GWh of electricity in 2008, more than three times as much as in 1999 when around 1,295 GWh was generated.19 By 2014, annual production had reached 9,480 GWh.

The authorities have ambitious plans to build on this initial success with further increases in capacity and production. The target set out in the 2013–17 NDP was for generation capacity to increase fourfold, from 1,917 MW in 2012 to 7,879 MW in 2017, mainly through a handful of very large projects. The target for energy production for the same period was comparable, with production earmarked to rise from 7,710 GWh in 2012 to 34,346 GWh in 2017. As illustrated in Figure 2, however, these targets seem highly ambitious in light of historical trends. In the first two years of implementation of the 2013–17 NDP, a significant gap emerged between annual targets and actual increases in production. That being said, a number of large projects were completed in 2017. This has boosted generation capacity, adding approximately 3,500 MW to existing capacity – 60 per cent of the planned increase – at a cost of more than US$7 billion.20 The shortfall relative to the target has been caused principally by the delay of a mega-dam, the 2,170-MW Caculo Cabaca hydropower project.

The significant expansion in generation capacity and production up to 2012 was not matched by improvements in distribution, however. Angola has continued to face difficulties with energy transmission, and its power infrastructure suffers from major efficiency losses. In 2007, there were reportedly between eight and 16 outages per month, with larger firms hit by more outages than other users. By 2010 the situation had improved to six outages per month, each lasting around 14 hours. Overall, the AICD study shows, Angola lost 36 days to power outages in 2010, twice as much as in other resource-rich African countries.21

The NDP sets quantitative indicators for energy distribution, with projected growth identical to that for production, and distribution equivalent to 85 per cent of planned production (see Table 1). However, these figures do not reflect the quality of distribution (i.e. there could still be frequent outages), and it is questionable whether the projections are realistic given past problems with transmission. A key obstacle to progress is that transmission in Angola relies on three main systems – in the north, central and southern parts of the country, respectively – that are independent and have yet to be interconnected.

|

1999/2002 |

2008 |

2012 |

2014 |

2015 |

2017 |

|

|---|---|---|---|---|---|---|

|

Capacity installed (MW) |

830** |

1,200 |

1,917 |

2,861 |

3,561 |

7,879 |

|

Electricity produced (GWh) |

1,295* |

4,133 |

7,710 |

12,618 |

17,018 |

34,346 |

|

Energy distributed (GWh) |

– |

– |

6,554 |

10,725 |

14,465 |

29,194 |

Sources: Pushak and Foster (2011), Angola’s Infrastructure: A Continental Perspective; and República de Angola (2012), National Development Plan. * 1999 data. ** 2002 data.

A rough indicator of the current state of affairs in the energy sector is provided by the World Bank’s indicators for ‘getting electricity’ in its Doing Business rankings. On this measure, Angola ranked 166th out of 189 countries in 2016, with a score of 0 out of 8 on the ‘reliability of supply and transparency of tariffs index’.22 This compares to an average of 0.9 for sub-Saharan Africa as of 2017.23 The lack of reliable supply in Angola has led to widespread use of self-generation capacity by both households and firms (for the latter, such capacity was estimated at 900 MW in the 2011 AICD study). Self-generation is associated with much higher costs than necessary. Perhaps the gravest finding of the AICD study was the extent of efficiency losses in the energy sector, which is estimated to have ‘haemorrhaged’ US$618 million – equivalent to 0.9 per cent of GDP – in 2009 alone. This was due mainly to under-pricing, distribution losses and low collection ratios. Hidden costs were equivalent to approximately 400 per cent of sector revenue, four to eight times higher than in countries like Zimbabwe, Botswana, Zambia and Mozambique. That said, the efficiency gap cited in the AICD study differs qualitatively from challenges specifically related to infrastructure development.

Investment in hydroelectric dams holds the potential to lower power costs in the medium term. However, it is too early to assess whether the significant capital expenditure involved will offer value for money. Increasing production is pointless unless the transmission system is also greatly improved. The logical implication is that the next NDP (2018–22) needs to prioritize development of the transmission system, include strong indicators, and be subject to mandatory public progress reports as well as a medium-term review.

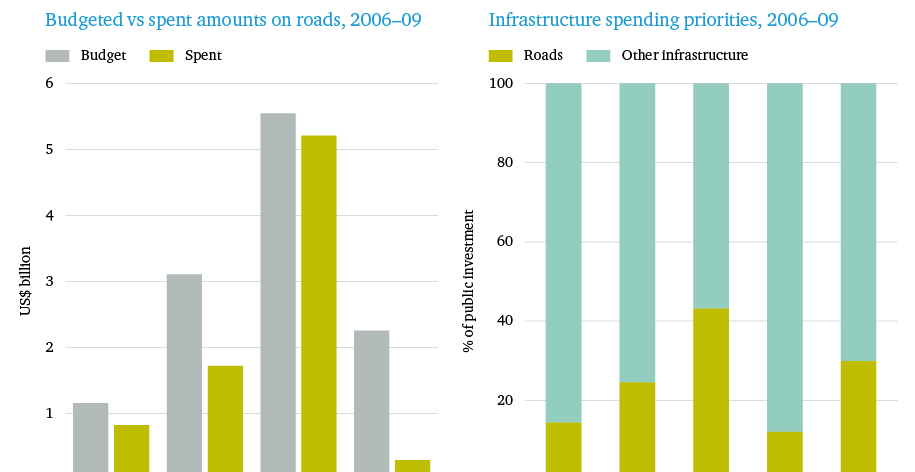

According to the AICD study, roads have been the principal priority of the Angolan government’s reconstruction plans. The study found that public spending on roads had been ‘… averaging a staggering $2.8 billion over the period 2005–09’.24 Data derived from the government’s integrated financial management information system (SIGFE) show that actual expenditure on road infrastructure averaged US$2 billion per year between 2006 and 2009, while the budgeted annual average for this period was US$3 billion, indicating a budget execution rate of 67 per cent. There were significant year-on-year increases in amounts budgeted and spent until 2008. In 2009, many infrastructure projects were halted as a consequence of the global financial crisis (see Figure 3). While underspending in 2006 and 2007 reflected insufficient capacity in the system, in 2009 it reflected stricter budget rules. However, this does not change the finding that roads were given rapidly increasing priority from 2006 to 2008, with 44 per cent of all public investment being spent on roads in 2008 (see Figure 3). Over the whole 2006–09 period, the amount budgeted for roads accounted for 31 per cent of all public investments and 37 per cent of actual expenditure. These numbers reflected both the very poor state of roads in Angola after the civil war, and the determination within the administration to reopen the country to vehicular circulation. The government’s second-highest priority was energy, which accounted for 8 per cent of the total allocation for public investments, followed by communications (6 per cent), education (5 per cent), rail (4 per cent), water (4 per cent) and housing (3 per cent).

Credible and comparable figures on the state of Angola’s road network are scarce, and tend to be described and categorized differently by different sources. The Institute of Angolan Roads (INEA), the government body responsible for the sector, has no functional website. Some useful data can be found at the website of the Ministry of Construction, which oversees INEA, but it is still difficult to get the full picture. Data from the AICD study and other sources are used here to piece together as coherent a picture as possible of the state of the Angolan road network.

At the time of the AICD study, the country had 62,560 km of roads, of which the classified network of primary, secondary and tertiary roads covered 36,399 km. This was complemented by an urban road network of 11,057 km. Unclassified roads made up the remaining 15,104 km. The road network density recorded in the study, measured in kilometres of road per 1,000 sq km, was less than a third of that in low-income, non-fragile African countries. Only 58 per cent of primary and secondary roads and 40 per cent of tertiary roads were estimated to be in good or fair condition – again, proportions substantially below those in other African countries.25

Transport and logistics was one of the four priority clusters in the 2013–17 NDP, which envisaged investment in road infrastructure as a means of improving national cohesion. Investment was also seen as a way to interlink the country’s provinces, main cities and distribution infrastructure as part of a broader vision for the establishment of national development corridors, as outlined in the government’s longer-term Vision 2025 plan. Each cluster in the NDP included a subset of projects, with more than a third of all projects and 41 per cent of estimated spending assigned to transport and logistics (see Table 2); more than half of the transport and logistics projects were in the road sector.26

|

2013–17 NDP clusters |

Number of projects |

Estimated spending, Kz bn |

|---|---|---|

|

Energy and water |

65 |

1,384 |

|

Food and agro-industry |

57 |

270 |

|

Housing |

35 |

602 |

|

Transport and logistics |

123 |

2,343 |

|

Non-priority clusters |

51 |

1,081 |

|

Total |

331 |

5,680 |

Source: Republic of Angola, Ministry of Planning and Territorial Development (2012), Plano Nacional de Desenvolvimento 2013–17.

Despite the priority given to roads in infrastructure planning, data from the Ministry of Construction indicate that the actual expansion of the road network between 2001 and 2013 was limited.27 According to this source, only 1,200 km of paved roads were added to the network in this period, relative to the 2001 baseline. The analytical challenge here is that the source does not mention the condition of the roads in question. A high percentage of the roads nominally classified as paved in 2001 were most likely in a state of degradation that, in practical terms, would have required their complete rehabilitation. In a different presentation, the Ministry of Construction said that 6,403 km of primary roads had been rehabilitated by 2010, and that a further 5,837 km were rehabilitated between 2011 and 2014, bringing the total extension of the paved road network to 12,240 km by end-2014. From 2012, the ministry started registering kilometres of rehabilitated secondary and tertiary roads as well, most likely because these types of roads were identified as priorities in the 2013–17 NDP.28

|

Until 2010 |

2011 |

2012 |

2013 |

2014 |

Total |

|

|---|---|---|---|---|---|---|

|

Primary |

6,403 |

986 |

2,581 |

1,156 |

1,114 |

12,240 |

|

NDP targets |

3,000 |

3,500 |

||||

|

Secondary |

– |

– |

412 |

593 |

646 |

1,651 |

|

NDP targets |

1,000 |

1,500 |

||||

|

Tertiary |

– |

– |

539 |

776 |

703 |

2,018 |

|

NDP targets |

15,000 |

15,000 |

||||

|

Bridges |

286 |

8 |

5 |

7 |

32 |

338 |

Sources: Republic of Angola, Ministry of Construction (2013), ‘SIGMINCONS’, presentation, 30 September 2013; and Republic of Angola, Ministry of Construction (2014), ‘Balanço de Actividades do Ministério em 2014 no âmbito do PND 2013–2017’.

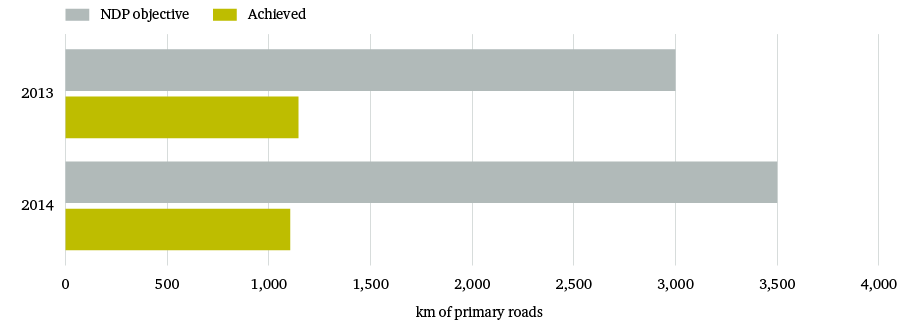

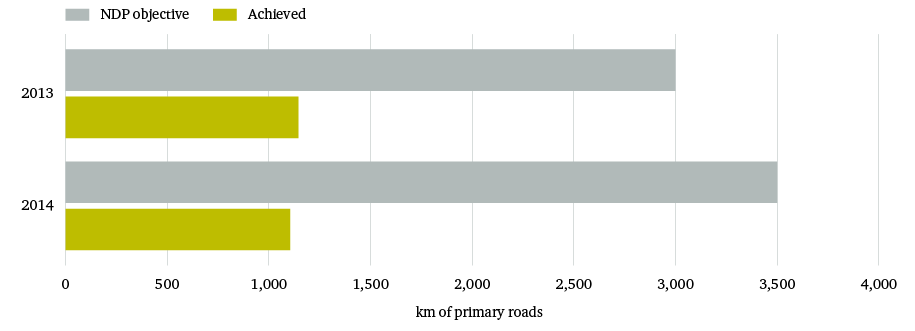

The 2013–17 NDP set ambitious quantitative targets for road ‘construction and recuperation’, with works on 15,500 km of primary roads, 6,000 km of secondary roads and 65,000 km of tertiary roads planned for the five-year period.29 Clearly, the onset of the economic crisis linked to the fall in oil prices from the second half of 2014 affected the government’s ability to meet these objectives. However, the plan was already significantly behind schedule even in the early part of the NDP planning period, when funding was not yet an issue. Only about a third of the works planned for primary roads in 2013 and 2014 (2,270 km out of 6,500 km) were completed (see Figure 4). For secondary roads, about 50 per cent (1,239 km) of the target (2,500 km) was met during 2013 and 2014, while for tertiary roads the figure was around 5 per cent (1,479 km out of 30,000 km).30

As illustrated by the shortfall in meeting targets for road construction in 2013 and 2014, it seems clear that the NDP had overambitious targets, as falling oil prices reduced the amount of funding available only from 2015 onwards. Prior to and in the first half of the 2013–17 NDP period, budgets had fluctuated significantly – with massive increases between 2006 and 2008, a sharp drop in 2009, and then steady increases again between 2010 and 2014. Figures for 2006–08 suggest that absorptive capacity increased almost at the same pace as budget increases, a development explained by the involvement of both domestic and foreign enterprises (including Chinese firms, financed through the credit lines agreed with the Chinese government).

The most likely explanation for the relatively low rates of road construction, relative to targets, is therefore a combination of unrealistic planning in terms of the actual kilometres of road that could be delivered within a certain time frame, and a challenging operating environment for road construction (e.g. difficult projects, a lack of skilled labour, bottlenecks in supply chains). This suggests that the shortcomings in the 2013–17 NDP need to be thoroughly evaluated and the conclusions used to inform future planning and budgeting. Efficiency issues have been a major factor in the government’s inability to deliver on planned targets, as acknowledged in 2016 by the former minister of finance, Armando Manuel.31

Quantitative targets aside, there are no recent assessments of the quality of new roads other than in the 2011 AICD study. It is unfortunate that institutions such as the World Bank and African Development Bank (AfDB) have not used the baseline provided by the AICD study to keep data and analysis up to date. Currently the only source of information is anecdotal evidence from fieldwork in Luanda, which indicates that the quality of the rehabilitated road network is generally low, due to poor construction and inadequate maintenance, and that Angola has missed an opportunity to deliver a key requirement for inclusive economic growth.

In October 2015, the government set up a new Road Fund to improve efficiency in the conservation and maintenance of the road network. This institutional change was a key recommendation of the AICD study, but it remains to be seen whether it will be effective.

In October 2015, the government set up a new Road Fund to improve efficiency in the conservation and maintenance of the road network. This institutional change was a key recommendation of the AICD study, but it remains to be seen whether it will be effective. Given that the Road Fund was created after the onset of the economic crisis, it possibly reflects belated recognition of the need to preserve funding for maintenance of the rehabilitated network, as well as a shift in priority away from new projects.

Data on the cost of road projects in Angola are scarce. Institutions such as the World Bank and AfDB have attempted to estimate the cost of roadworks per kilometre, but this has proven difficult. Projects vary greatly, and descriptions and data often have few details beyond the different types of roads involved. Differences in design standards such as lane widths, terrain, traffic, overlay thickness, regravelling thickness, rehabilitation surface and improvement type are often not accounted for. Hence, there are very wide ranges in estimated average costs. The AfDB concludes that no such thing as a ‘typical’ unit cost can be established. Despite these caveats, both institutions have presented broad figures on the cost of roadworks per lane kilometre (in 2006 US dollars).32 For simplicity and ease of comparison, only the highest unit costs by quartile identified by the two institutions are shown in Table 4.

|

Institution/year |

Unit |

US$/lane km |

||

|---|---|---|---|---|

|

Lower quartile |

Median |

Upper quartile |

||

|

World Bank (2008) |

Construction (paved) <50 km |

349,523 |

401,646 |

613,929 |

|

Rehabilitation (paved) <50 km |

220,186 |

352,613 |

505,323 |

|

|

AfDB (2014) |

Construction/upgrading of paved road projects <100 lane km |

166,300 |

227,800 |

425,400 |

|

Paved road rehabilitation projects <100 lane km |

109,800 |

180,300 |

290,000 |

|

Sources: Africon (2008), Africa Infrastructure Country Diagnostic: Unit Costs of Infrastructure Projects in Sub-Saharan Africa, Abidjan: AfDB; and AfDB (2014), Study on Road Infrastructure Costs: Analysis of Unit Costs and Cost Overruns of Road Infrastructure Projects in Africa.

It has not been possible, given the scope of this research paper, to source figures directly comparable to the ones presented by the AfDB and World Bank. The author was able to obtain estimates only of total spending on road infrastructure between 2006 and 2009, and of kilometres of road constructed and repaired until 2010. These two variables can be used to estimate, very roughly, how much the government spent per kilometre of road. Given the post-war acceleration in spending on infrastructure, and on the roads sector in particular, and given the massive reduction in spending in 2009 and 2010, it is reasonable to assume that two-thirds of new roads (4,290 km) were constructed between 2006 and 2008. Another assumption made as part of this exercise is that 75 per cent of the roads constructed were two-lane roads, and that 25 per cent were four-lane roads. Official data indicate that, in these three years, the government spent US$7.3 billion (in constant 2006 US dollars) on road projects.33 Based on these assumptions, the amount spent per lane kilometre of road works out at US$682,762.

A 2015 World Bank paper found evidence that the unit costs of road construction and maintenance are higher in countries with higher levels of corruption.

It should be emphasized that this is a rough, albeit relatively conservative, estimate. Great care should be exercised when making comparisons based on this figure. That being said, it is noteworthy that the amount exceeds the highest estimates of both the World Bank and AfDB, as shown in Table 4 (and could potentially have been even higher than calculated here). A 2015 World Bank paper – drawing on the World Bank’s Worldwide Governance Indicators (WGI) and Transparency International’s 2008 Corruption Perceptions Index – found evidence that the unit costs of road construction and maintenance are higher in countries with higher levels of corruption.34 This finding seems to substantiate the notion of unit costs being higher in Angola than on the rest of the continent as Angola has historically suffered from high levels of corruption. While it is encouraging that the 2015 World Bank paper finds a strong correlation between reduced corruption and lower unit costs, there are no signs that the high corruption levels in Angola have been tackled over the past decade. Indeed, in 2016 the country still ranked extremely poorly in the Corruption Perceptions Index and for ‘control of corruption’ in the WGI.35

All this suggests a need for the government to undertake an in-depth review of the costs of road construction based on more detailed data, for example covering the approximately 60 road projects that were included in the transport and logistics cluster of the 2013–17 NDP. Reasons for levels of spending, and for variations in those levels, would need to be analysed, and ways of reducing costs and increasing value for money identified (with an explicit focus on anti-corruption measures). The data and analysis would also need to be disclosed to the public to allow for scrutiny outside government, in order to promote increased accountability and efficiency in the delivery of public infrastructure.