Brexit, for better or worse, means a major structural change in how people in the UK think about the food they eat. There is an opportunity to reformulate food policy for the better, but this could be easily squandered if not managed carefully.

Research paper

Published 10 January 2019

Updated 14 December 2020

ISBN: 978 1 78413 304 7

Brexit, for better or worse, means a major structural change in how people in the UK think about the food they eat. There is an opportunity to reformulate food policy for the better, but this could be easily squandered if not managed carefully.

In November 2018 the EU27 and the UK government issued both the draft Withdrawal Agreement and a Political Declaration setting out the framework for the future relationship between the UK and the EU. While the Withdrawal Agreement runs to almost 600 pages, the Political Declaration is less than 30 pages. The detail and much of the shape of the future relationship is still to be negotiated, but according to the Political Declaration, the EU and the UK:

envisage having a trading relationship on goods that is as close as possible, with a view to facilitating the ease of legitimate trade.

and

envisage comprehensive arrangements that will create a free trade area, combining deep regulatory and customs cooperation, underpinned by provisions ensuring a level playing field for open and fair competition.61

The UK government’s stated aim is to secure long-term trading arrangements with the EU by December 2020, the end of the transition period. However, Article 132 of the Withdrawal Agreement makes clear this transition period could be extended once. This is in recognition that negotiations around the future relationship may not be completed within 21 months.

Under this scenario, the UK would remain very closely aligned with the EU either through membership of the EU’s single market and/or a customs arrangement with the EU.62 For example, the UK could look to join the European Free Trade Association (EFTA) and European Economic Area (EEA), aligned with the so-called ‘Norway model’. The Norway model would almost certainly necessitate sacrificing one of the UK’s red lines – the commitment to ending freedom of movement.

Maintaining close regulatory equivalence and a common customs arrangement would facilitate cross-border checks for EU produce and limit delays to trade. This is important because, collectively, NTBs can have a much greater impact on prices than do tariffs (see Box 1).63 In a study for the National

Farmers’ Union, van Berkum et al.64 assumed that additional costs after Brexit through NTBs would amount to between 5 per cent and 8 per cent for imports from and exports to the EU.

One example of this is the phytosanitary checks required for fresh produce. Currently, the European Commission’s Directorate-General for Health and Food Safety (DG SANTE), through its Health and Food Audits and Analysis Directorate, is responsible for inspections of EU produce and production in EU member states. It also checks non-EU exports to the EU for compliance with EU standards.65 These checks and controls can take up to 48 hours. Were the UK to diverge from EU standards – especially around sanitary and phytosanitary standards and under some ‘hard Brexit’ scenarios – this could increase this interval considerably.

Under this scenario, the UK would remain very closely aligned with the EU either through membership of the EU’s single market and/or a customs arrangement with the EU.

Moreover, estimates suggest that it could take between five and 10 years to build the necessary infrastructure at UK ports.66 The remit and resourcing of the UK Food Standards Agency would need to be significantly enlarged to cope with additional responsibilities that are currently undertaken by the European Food Safety Authority, particularly with regard to assuring food safety and authenticity.

A close post-Brexit scenario would be likely to restrict the scope of free-trade agreements that the UK is able to conclude with third countries, as these agreements would almost certainly need to comply with EU standards. It would also mean that the UK became a ‘rule-taker’, whereby it would need to comply to a high degree with EU rules and regulations but would have little or no say in their design.

This scenario may also arise if the UK and the EU fail to reach a free-trade agreement by the end of the transition period and the Irish ‘backstop’ arrangement comes into being. The backstop is intended to serve as an insurance policy that would come into force if no option (whether technological or legal) is found to prevent the reimposition of a hard border between Northern Ireland and the Republic of Ireland. This arrangement would in effect keep the whole of the UK in a customs arrangement with the EU, but would subject Northern Ireland to more EU rules than the rest of the UK. This proposed arrangement has been highly controversial, with critics and opponents asserting that it would undermine the constitutional integrity of the UK. In particular, Northern Ireland’s Democratic Unionist Party, with which Theresa May’s Conservatives reached a ‘confidence and supply’ agreement on critical votes in Parliament following the 2017 general election,67 has been implacably opposed to the arrangement.

The UK’s intention to leave the EU single market and customs union is particularly problematic for trade between the Republic of Ireland (ROI) and the UK. The value of trade across the Irish border is estimated at around £5 billion per year (although this is notably less than the trade between Northern Ireland and the rest of the UK, or between the whole of the UK and the ROI). The wider concern is that any barriers to trade (either customs or regulatory) or visible border infrastructure would threaten the political settlement in Northern Ireland.

Food and live animals are also a significant part of the trade between Northern Ireland and the ROI, contributing about a third of the total value of goods traded between the two. Northern Ireland exports £1.5 billion of food to the EU, of which around 70 per cent goes to or through the ROI. In 2015 exports of food and live animals from Northern Ireland to the ROI were valued at £732 million (from a total export value of £2.2 billion); exports from the ROI to Northern Ireland were valued at £796 million (from a total export value of £2.6 billion). Food and live animal exports from Northern Ireland to the ROI are more than three times the volume that goes to the UK. For many food products, the border is crossed multiple times along the value chain (so called ‘pancaking’): for example, foods may be produced in one country, processed across the border, packaged back in the first territory, and then sold into the other.

While the UK’s proposal for a free-trade area for goods combined with a facilitated customs arrangement would help to minimize friction at the border, some checks would inevitably take place. This is because the UK would no longer share a common regulatory space with the EU. In practice, a British company exporting to the EU would need to prove that its products still comply with EU rules, including VAT, phytosanitary and rules of origin (whereby different requirements apply to imports that include materials from more than one country). The same will apply for EU companies exporting to the UK.

Research for the European Parliament has highlighted a range of potentially useful technologies that are currently in use at borders internationally.68 These include automatic number-plate recognition, enhanced driving licences, smartphone apps and barcode scanning. In the case of Northern Ireland and the ROI, these measures could be linked with additional bureaucratic approaches such as mutual recognition of authorized economic operators, or a simplified customs declaration system to significantly reduce or even remove the need for processing at the border. However, the House of Commons Northern Ireland Affairs Committee (NIAC) is less optimistic, stating: ‘[W]e have had no visibility of any technical solutions, anywhere in the world, beyond the aspirational, that would remove the need for physical infrastructure at the border’.69 In any case, such technological solutions would require considerably more time to be developed, tested and deployed than is currently available.

Under this scenario, the UK would have a looser relationship with the EU, outside the EU’s customs union and the EEA. Such a relationship is a looser version than is envisaged in the negotiated Political Declaration on the future relationship,70 and is broadly in line with the Comprehensive Economic and Trade Agreement (CETA) between the EU and Canada. This so-called Canada model would potentially allow the UK greater autonomy in developing trade relationships with third-party states, governed by standards that may not align with the EU’s. (For a fuller discussion, see the section below on the UK’s trade relationships with the rest of the world.)

However, such an arrangement would almost certainly result in the reimposition of some tariffs on EU imports to the UK, and vice versa. Existing EU tariffs vary considerably between sectors and products. A Canada-style agreement could go some way in eliminating tariff barriers, although even under CETA tariffs remain for a number of agricultural products such as eggs and poultry – as do limits on tariff-free trade across many other agricultural areas, including wheat and pork.71 In other words, a Canada-style trade agreement could result in a double penalty of higher prices for UK imports from the EU, due to NTBs and/or tariffs, together with more (cheaper) imports from non-EU countries with poorer quality and sustainability standards. While UK farming sectors that depend on EU markets (for example lamb, where the UK imports little from the EU but exports a high volume to the EU) would suffer because their exports would become expensive, those competing with other EU countries might gain (an example being pork, imports of which to the UK mainly come from the EU, but a significant amount of exports are with third countries).

This kind of trade deal would also require the EU to revisit its tariff rate quotas (TRQs).72 Currently, the EU’s WTO TRQs are shared between all member states, including the UK. There are currently 128 TRQs on EU agri-food imports, which apply to approximately 6 per cent of such imports by value.73

In October 2018, the EU Council endorsed a joint UK–EU agreement on the initial reallocation of TRQs with respect to a number of agricultural, fisheries, industrial and processed agricultural products. The adjustment of the EU’s TRQs entails dividing up the existing quantities between the UK and the EU based on previous trade patterns. The EU and UK will now have to engage in negotiations with WTO partners for each of these TRQs. Some major exporters of agricultural products have already expressed objections to the agreement, asserting that the changes go beyond reallocation and result in reduced market access. Negotiations between the EU and UK and WTO members are ongoing.74

The ‘no deal’ option would be the default scenario if no withdrawal agreement has been ratified by the time the UK leaves the EU (currently set for 29 March 2019).

Under this scenario, the UK would be outside any existing agreements involving the EU, and would therefore be considered a third country. Exports from the UK to the EU would be subject to the EU’s external tariff system, which would significantly increase the costs of food exports and, presumably, imports if the UK imposed reciprocal tariffs on agri-food products coming into the UK in order to protect British producers or maintain leverage for future negotiations. NTBs would also apply. Immediately, there would be issues at the borders for exports to the EU (and potentially for imports to the UK). For example, any meat supplier would need first to be certified through the EU’s existing system to ensure it complied with EU standards and measures. Transport companies would also need to complete new licensing paperwork in order to export from the UK to the EU. For example, exports to the EU of food of animal origin is prohibited unless the establishment in the UK from which the food is dispatched or prepared is ‘listed’ by the European Commission for public health purposes.75

It is unclear how long border checks would take under a ‘no deal’ scenario, so pressure on warehouses to stock fresh produce is likely to increase dramatically. As previously noted, the UK currently operates a ‘just in time’ food system, maintaining five to 10 days’ worth of groceries in the country (and often less for fresh produce). Already, concerns are growing that food warehouse capacity is likely to be inadequate, putting ‘just in time’ at risk.76

A ‘no deal’ Brexit is not necessarily an endgame scenario, but it could well happen by default if the UK and the EU are unable to approve a withdrawal agreement before the end of Article 50 negotiations. The reality is that the UK’s relationship with the EU is so deep, complex and multidimensional that it is difficult to imagine an outcome in which the UK does not reach a free-trade agreement with the EU in the long run. Given the current volume of UK–EU trade, there would be an imperative to develop a free-trade agreement between the UK and the EU to reduce friction at the borders – through minimizing tariffs and NTBs – and maximize market openness.

CETA, which entered provisional effect between the EU and Canada in September 2017, is relevant in this context. In 2017 Canada exported €2.2bn of agricultural produce to the EU,77 as against the UK’s £13.3 billion (some €15 billion).78 Given the scale and interdependency of trade between the UK and the EU27, it is reasonable to suppose that the UK and the EU would aim to develop a trade agreement – i.e. a deeper relationship than WTO (‘rules only’) – in due course, although this in itself would likely be a protracted and complex process.

The potential for no Brexit, should not be disregarded. The UK remaining in the EU could arise with or without a second referendum. Under this scenario, the UK would continue to be a party to the EU’s extensive web of trade agreements. As an illustration, in 2016 over 50 per cent of UK goods and services exports went to the EU or to countries with which the EU has a full or provisional trade agreement.79 Today, the UK imports food from 168 countries.80

The EU’s trade agreements not only open global markets for EU food products, but also drive competition for EU producers and manufacturers within the EU. Research published by the European Commission highlights that 90 per cent of additional demand for agriculture products in the next decade will come from outside the EU – with greater benefits for the EU economy and consumers.81

For many proponents of Brexit, the extent to which the UK could diverge from the EU, reshape domestic policies and strike independent trade agreements are the key opportunities presented by Brexit.

However, agriculture is frequently one of the most contested sectors in trade negotiations, often excluded entirely. Tariffs often remain in place. To illustrate, the EU’s average agricultural tariff on imports from countries with which there is no free-trade or preferential agreement is 8.5 per cent82 but for trade with the US it averages 11.1 per cent.83 This compares with an average tariff between the US and the EU of 3 per cent.84

The US has already indicated that it would seek an agreement with the UK that had zero tariffs across a clear majority of goods traded. This could be possible.

The US has already indicated that it would seek an agreement with the UK that had zero tariffs across a clear majority of goods traded. This could be possible. In the case of the Australia–United States Free Trade Agreement, for example, all tariffs have been eliminated for imported products from the US into Australia, while most tariffs have been removed in the reverse trade.85 But there would likely be new conditions. US trade secretary Wilbur Ross suggested that changing UK regulations such as the current ban on chlorinated chicken in the EU would form a ‘critical component of any trade discussion’ with the UK.86 This is likely to be the case with other candidate countries for new bilateral trade agreements, such as New Zealand and Australia. Geographical indications could also become an issue (see Box 3).

Meanwhile, choices to increase food imports from one country could adversely affect UK exports to another country. For example, a free-trade agreement with the US that allowed imports of hormone-treated beef, which is banned in the EU, may necessitate longer and more rigorous checks at the border to avoid the banned product entering the EU. It is notable that neither Switzerland nor Norway – which are bound to the EU Sanitary and Phytosanitary Standards (SPS) to ensure close regulatory alignment with the EU – have been able to strike wider free-trade agreements encompassing the agriculture sector.

Geographical indications (GIs) apply to products that have a specific geographical origin and possess qualities or a reputation that are due to that origin. Currently, the UK has 86 protected regional and traditional foods and drinks87 – including Scotch whisky, which is by far the UK’s most valuable food and drink export, contributing around £4 billion in annual export revenues and accounting for more than 20 per cent of total food and farming products by value.88 UK goods are currently covered by the EU’s system of GIs and there is a different system in place in the US.

When it comes to the production of whisky, EU legislation requires that the product is aged for at least three years. Yet, the US Trade Representative is arguing that the EU’s age requirements are too restrictive and should be eased.89 In July 2017 Scotland’s then economy secretary, Keith Brown, urged the UK government to protect the Scotch whisky industry after Brexit by applying the current EU definition of whisky in UK law, emphasizing that the industry supports some 20,000 jobs.90

For supporters of the UK’s withdrawal from the EU, one of the benefits of an independent trade policy would be the freedom to import food from regulatory regimes that the EU currently rejects. In fact, some third countries may push the UK to increase its openness to importing their agricultural outputs – particularly if the UK lowers standards for food imports. The former UK ambassador to Washington Sir Peter Westmacott was reported in May 2018 as saying:

The imported chicken may not taste very good and it may be chlorine-washed, but it will be very competitively priced … That is going to be the price of a free trade agreement.91

Despite assurances from environment secretary Michael Gove that the government would not allow a trade agreement with a third country that has lower animal welfare standards and hygiene issues,92 not all Cabinet ministers feel the same way. While giving evidence to the Commons International Trade Committee, the Secretary of State for International Trade, Dr Liam Fox, suggested that there are ‘no health reasons’ why people should not eat chickens that have been washed in chlorinated water, and that he had ‘no objection’ to it being sold to the British public.93

And while UK food producers could continue to compete ‘at the top of the value chain’ on provenance and quality, a rigorous and transparent sourcing and labelling system would need to be in place that allows British consumers to choose and have confidence that ‘when they are buying British labelled food, there will be a warrant that the product has met high quality and more sustainable standards’.94 Given that consumer confidence in their own ability to choose goods based on attributes such as sustainability or health is already limited (and is typically impossible within the hospitality sector, where food is rarely labelled), to fully enable consumers to choose on provenance and wider attributes would require such a significant change in transparency and engagement that it is currently implausible.

This also assumes that UK farming would remain the same. Yet, the implications of new trade deals for UK farming will depend upon both market responses (and exchange rates) and the regulatory approaches applied to them after the UK has left the EU and the CAP. If UK farmers are subject to a level and open playing field with importers, this could result in a ‘race to bottom’ whereby values are compromised across the board. Ethically minded consumers who prioritize quality in provenance or animal welfare may only be able to exercise individual choice by paying higher prices, such as buying organic produce – over and above the post-Brexit changes in food prices – through tariff and non-tariff barriers and exchange rate fluctuations.

This restructuring could lead to the creation of a ‘double standards’ system where a two-tier regulation system leads to two-tier consumption – with some produce been created (probably domestically) to higher animal welfare and environmental standards, while cheaper food products with lower standards are imported, without explicitly stating that these lower prices are in detriment of lowering current food standards. This could undermine the trust and satisfaction of consumers and citizens, with implications not only for the food industry but also for government.

In fact, the hidden costs of producing and consuming ‘cheap’ food can be transferred to other areas of public policy. As already noted in Chapter 2, lower food prices are not necessarily in the public interest if they are at odds with environmental or health outcomes. For instance, if nutritious diets become more expensive, access to cheaper food would encourage an overconsumption of calories and diets that do not provide complete nutrition, generating additional healthcare costs. One study has suggested that the impact of changing food prices post Brexit, under two scenarios, might create additional deaths of 2,700–5,600 people over the next decade, with a direct economic cost of £290m–£600m. Using current estimates of society’s ‘willingness to pay’ to avoid unnecessary deaths, this extra mortality would increase NHS costs by 0.9–1.8 per cent.95

The development of a food system with two regulatory regimes would require clear labelling, transparency and information to allow consumers to choose in a market place with double standards. The 2013 Which? report on the future of food in the UK recommends that local production should be supported, and that supply chains should be more transparent, although the report’s authors did express reservations as to the potential for future UK administrations to implement measures to ensure these outcomes.96

As has been seen in recent months, global trade relations are dynamic and domestic political choices can have global ramifications. Most starkly, President Donald Trump has followed through on campaign pledges to impose tariffs on numerous imported goods (including aluminium and steel, machinery and vehicles as well as agricultural commodities) that have impacted a wide variety of countries, among them China, Canada and EU member states (see Box 4).

With Brexit, the UK may be more susceptible to the vagaries of the global market and the actions of the key protagonists. For example, climatic and other environmental changes, and increasing global demand for food, are already making supply chains less resilient and more volatile. Careful consideration will need to be given to the UK’s potential increased dependence on agricultural products from countries that are less politically aligned with its own values, and where the UK has less influence.

In January 2018 the US starting imposing tariffs on a variety of Chinese goods and as China responded, the breadth of products which were affected, on both sides, has increased. Currently, additional tariffs have been placed on 279 product categories that China imports from the US, while China has 333 product categories that are now affected. The US has threated to expand the list further, to include $200 billion in imports.97

For China this has included soybeans, grains and pork. The US is the world’s largest exporter of soybeans, with a value of $22.8 billion in 2016. China is the world’s largest importer of the crop, importing $34 billion, of which one third comes from the US.98 China sourcing more of its soybeans outside the US will have global implications not only for the price of the commodity but also of livestock, as much of the bean is used for feedstocks.

The EU responded to the proposed US sanctions with suggested measures on iconic products, such as bourbon, jeans and Harley-Davidson motorbikes. However, in July, following a meeting between President Trump and the president of the European Commission, Jean-Claude Juncker, a joint EU–US statement concluded that both would ‘work together toward zero tariffs, zero non-tariff barriers, and zero subsidies on non-auto industrial goods. We will also work to reduce barriers and increase trade in services, chemicals, pharmaceuticals, medical products, as well as soybeans’.99

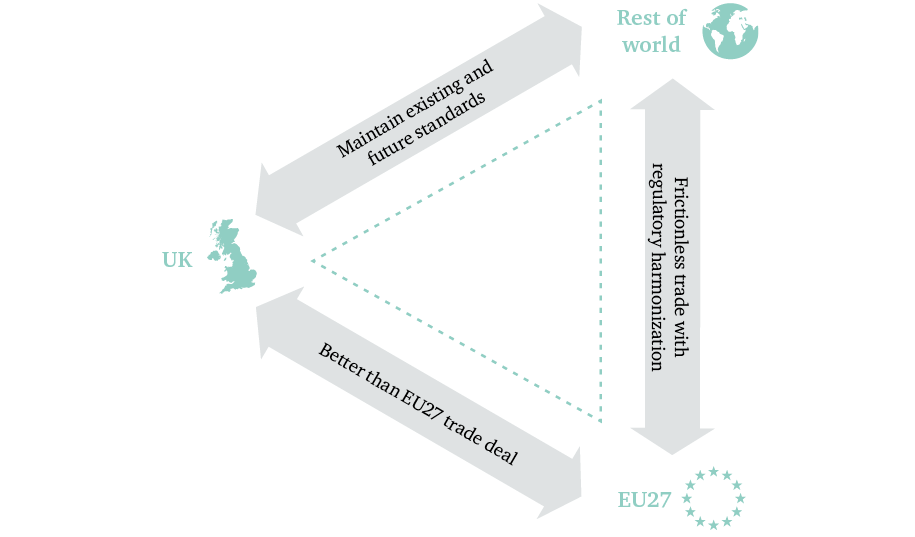

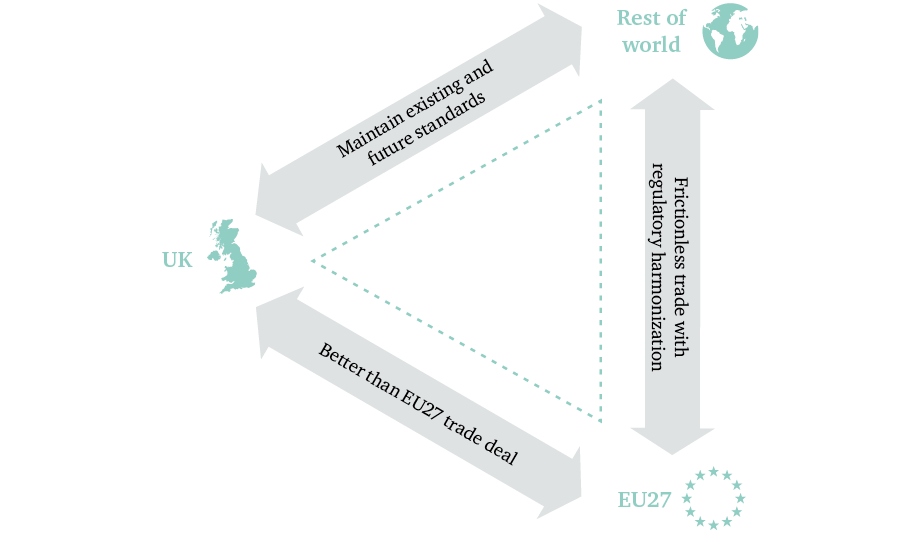

It is not clear in which direction UK trade policy will follow. Brexit negotiations have highlighted that the UK is pursuing an ‘impossible triangle’ of objectives: frictionless trade with the EU, ambitious new trade agreements around the world that respect existing standards and maintaining a profitable agriculture and food sector at home. Yet, as demonstrated above, benefiting from new trade deals is broadly incompatible with being close the EU (Figure 3).