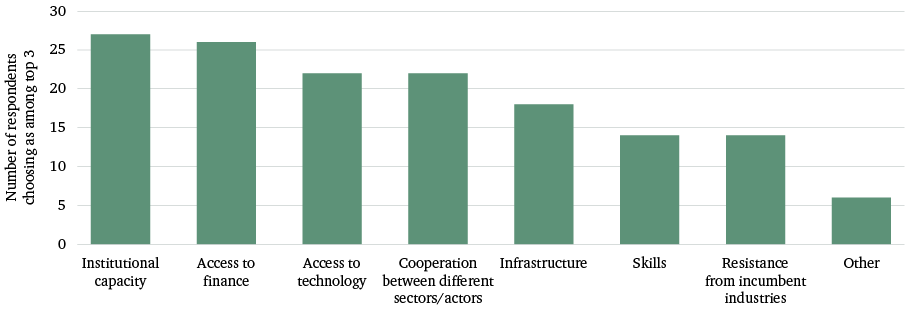

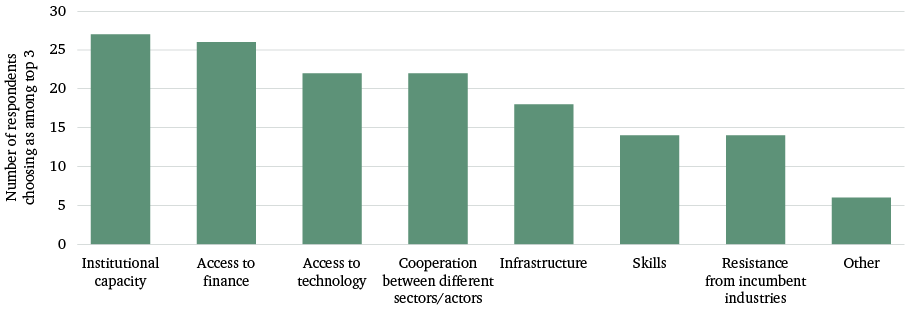

Below we consider in turn challenges relating to institutional capacity and access to finance and technology; economic and structural conditions; and persistent infrastructural deficits and a growing urban population. All of these factors are likely to have a bearing on the ease and pace with which circular practices may be implemented and scaled up in developing countries.

2.1 Capacity and finance constraints

2.1.1 Institutional capacity

The speed of urbanization in many developing countries has led to problems with the establishment and enforcement of appropriate regulations and mandatory standards to govern circular activities. In India, for example, more than 95 per cent of e-waste is processed in urban slums by untrained workers who lack adequate protective equipment and are exposed to a wide range of toxins. In Agbogbloshie, Ghana, large quantities of e-waste are burned, notably insulated copper wire, the valuable metal from which is easily recycled for trade (once the insulation is burned off). The burning of plastics such as this insulation exposes workers to dangerous levels of carbon monoxide and other hazardous substances. A recent report found record levels of brominated and chlorinated dioxins – two highly toxic chemicals – in free-range chicken eggs in Agbogbloshie, linked to the dismantling and burning of e-waste.

Without strong governance frameworks, there is a risk that developing countries will install cheaper but limited-quality technologies and equipment, including those mis-sold under the guise of a CE.

Without strong governance frameworks, there is a risk that developing countries will install cheaper but limited-quality technologies and equipment, including those mis-sold under the guise of a CE. There is evidence, for example, that waste-to-energy technologies reliant on incinerators are regularly sold in developing countries that lack proper testing facilities or oversight for the use of such equipment. In some cases, these technologies would not be approved for use in the countries in which they are made. Some stakeholders in the EU, meanwhile, have expressed concerns that dramatically increasing recycling and creating downstream markets for secondary materials could mean that toxic and hazardous materials that might otherwise be banned from consumer markets will be kept in circulation. The use of recycled plastics can bring health risks, for example via plastic waste streams that contain harmful pollutants such as brominated diphenyl ether (BDE) flame retardants, while water reuse is only beneficial for health if sufficient standards are in place.

Weak regulation is also resulting in substandard practices in construction, a sector in which the design and governance of new building stocks and assets will be critical to enabling longer asset lifetimes and the future refurbishment and reuse of materials (see Section 2.3). For instance, almost 90 per cent of residential built stock in the informal building sector in India is free from regulation, resulting in an increase in unplanned growth and settlements. Even when regulations are in place, such as in Ghana, Kenya, Nigeria and South Africa, persistent non-compliance has been reported, with lack of enforcement cited as a prominent cause. Tragedies including the collapses of a factory in Bangladesh in 2013, a 24-storey apartment building in Colombia in the same year and, most recently, a four-storey building in Nigeria in 2019 have increased awareness of the poor construction quality of many buildings in certain developing countries, and have strengthened demands for improved regulations.

CE policymaking is also likely to demand a level of centralized or distributed coordination across multiple ministries that is often difficult to achieve in developing countries. Governments are still largely organized along sector lines, with ministries focusing on specific areas. In most of these countries, environment ministries are often among the weakest departments in government, with limited influence over the industrial and innovation strategies needed to succeed in a CE. Those responsible for fostering more sustainable resource use will need to work closely with ministries of finance or industry to generate political buy-in and cross-government ownership.

Some of the most ambitious and radical CE-related policymaking is occurring in middle- and lower-income countries. Rwanda and Kenya have imposed total bans on plastic bags in an attempt to stem growing waste crises. Burundi, South Sudan, Tanzania and Uganda are reported to be considering similar measures. Yet even these positive examples have highlighted the impact of limited institutional capacity on policy implementation and regulatory enforcement. In both Rwanda and Kenya, plastic bags are still smuggled into the country, and retailers, manufacturers and consumers are struggling with the lack of cheap and good-quality alternatives. In Kenya, the ban has affected exports of food and flower products as there is a lack of adequate alternative packaging. Developing countries are by no means alone in experiencing these challenges: examples from higher-income countries include a growing illegal waste dumping problem in the UK; and the continued export of e-waste from several EU countries to Nigeria, in contravention of the Basel Convention and the EU’s waste shipment directive. Such cases point to the universal risk of weak governance undermining ambitious CE policies.

2.1.2 Access to finance

Activities associated with ‘linear’ (i.e. non-circular) resource extraction and processing often account for the bulk of financing, foreign exchange earnings and foreign investment in lower-income countries (see Section 2.2.2). Resource-led development – which focuses on leveraging the potential investment in, and revenue and jobs from, natural resource sectors – has been a popular theory among major donors and international organizations in recent years. International partners have often been significant supporters of resource-led development: between 2008 and 2015, multilateral development banks (MDBs) provided over $83 billion in public financing for fossil fuels alone. OECD analysis of private-sector resources mobilized for development reveals that almost half of these resources are focused on energy, industry, mining and construction.

Restructuring economies to accommodate more ‘circular’ activities will require a major shift in infrastructure, industrial processes and innovation priorities. Developing countries are already facing a major infrastructure investment gap in the order of $1 trillion a year between now and 2030; many lower-income countries lack even basic solid-waste management infrastructure. Yet current investment in modernizing solid-waste management processes and establishing the ‘reverse logistics systems’ needed to scale up the reuse of materials and products is inadequate: the European Investment Bank (EIB), for instance, invests relatively little in solid-waste-related activities. Access to finance for existing industry may also be needed to support the transition to CE activities. Without careful planning, many facilities and sites will struggle to function in the move to more resource-efficient economic activity.

MDBs face a number of challenges in scaling up finance for CE activities. For one, MDBs are reactive in their financing: they respond to specific requests for support from public- and private-sector clients, among whom awareness of the potential of the CE is lacking. Investments in unproven business models and new technologies may be seen as too high-risk by many MDBs, while the scale of funding required may be too small. MDBs are often mandated to work with national agencies and are less able to offer smaller-scale funding for subnational or municipal projects. At the same time, traditional project-based finance provided by MDBs is not well suited to the systemic and multi-stakeholder approaches often inherent to CE solutions.

Upfront investment costs for CE solutions may be unattractively high for certain buyer groups in developing countries, particularly in the case of technology-intensive solutions. Vertical farming systems, for example, offer a means of radically reducing the land footprint of agricultural production; crops are grown in layered containers rather than on land. But a vertical farm with the capacity to grow 1 million kg of produce a year can cost between $80 million and $100 million to establish, not counting the investments in research and development (R&D) first needed to build know-how among the local population. To date, lack of access to finance has been a major challenge for smaller firms and individuals seeking to implement innovative business models and practices in low-income countries: around 1.7 billion adults in developing countries do not have a personal bank account, let alone access to complex financial products, although digital technology is starting to transform access to finance in some areas.

2.1.3 Access to technology

Significant progress has been made on the technological foundations for CE activity. A growing range of data and information technologies are making CE solutions practical for the first time in a range of sectors. There has also been a step-change in the technology available to improve supply chain traceability: satellite-based GPS technology, the rise of the ‘Internet of Things’ (IoT), low-power wireless technology, advances in big data and ‘distributed ledger’ blockchain technology, and developments in artificial intelligence and machine learning – all are transforming companies’ ability to track and trace commodities and products and monitor environmental conditions in real time.

In many developing countries, however, the ‘digital divide’ remains a very serious problem, with more than 4 billion people still without access to the internet, and 2 billion people without a mobile phone. Many CE approaches do not require costly technology investments and are already widely accessible in developing countries. Household-level and farm-waste composting, for example, are well proven, low-cost and non-technology-intensive means of tackling food waste and reducing the need for fertilizer. ‘Sharing economy’ business models – whereby physical assets, such as cars and homes, are shared between multiple people – often only require the ownership of a single physical asset and a mobile phone. But other approaches depend on technological innovation. In agriculture, closed-loop production methods such as hydroponics and aeroponics, 3D printing and innovations in waste processing have the potential to transform traditional growing methods, dramatically reducing the resource inputs required and enabling fundamental changes to the spatial patterns of food supply chains (see Section 3.2). At a more fundamental level, asset-sharing frameworks often require digital platforms to link suppliers to consumers, as well as a stable energy supply. In the absence of reliable energy sources or government mechanisms to support universal access to basic digital and communications networks, the roll-out of CE activities risks excluding already marginalized communities.

E-waste imported by developing countries can act as a source of cheap hardware to help close the digital divide. In Ghana, the import and reuse of vast amounts of e-waste have been key to meeting demand for laptops among the student population. Similarly, refurbished phones are helping to expand connectivity, bringing welfare effects. But, under current practices, e-waste is also a far from perfect solution to the lack of access – as the fastest-growing waste stream in the world, it presents serious health and environmental risks, often for the most vulnerable groups.

2.2 Economic and structural conditions

2.2.1 Informal-sector employment

The vital role played by informal labour is one of the most important areas of divergence when comparing CE approaches in developing and developed countries. Developing economies typically have a more fragmented private sector, with considerably higher shares of informal-sector employment, than advanced economies. Almost 70 per cent of the employed population in developing regions is in informal employment, and waste management is among the principal activities of the informal sector. While reliable data are scarce, estimates suggest that waste management provides income opportunities for millions of the poorest people around the world. As many as 0.5 per cent of urban residents are estimated to be working in informal-sector recycling. In India, 1.5 million people are involved in informal waste management.

Informal waste-picking is rarely the most effective means of processing waste, however. Where previously waste-pickers may have been well equipped to process simpler industrial materials, increasingly they are dealing with e-waste – often made up of complex composites – and lack the skills and technology to optimize recycling and repair processes. With the informal sector capturing a large share of material flows, more formalized processes that may be better suited to recycling e-waste cannot source enough feedstock to recycle these products in an economical way. For example, numerous formal facilities in China have been unable to compete with the informal sector due to the latter’s established network, low operating costs and convenience of collection.

2.2.2 Resource-intensive economies

For many developing countries, natural resources – defined broadly here to include both extracted minerals and agricultural goods – account for a large proportion of GDP, employment or both. For countries with large hydrocarbon and mineral reserves, models of extractives-led growth have long been promoted by national governments, multilateral organizations and donor agencies. Resource revenues have been a key driver of development gains and economic growth to date: the majority of low-income countries depend on natural resource rents for at least 10 per cent of their GDP. For many countries, moreover, agriculture continues to be the single largest source of domestic employment: in least developed countries, it accounts on average for 60 per cent of employment, compared with 26 per cent in middle-income countries and 5 per cent in OECD countries.

While the CE has the potential to create new opportunities for value addition and employment – many of them local (see Section 3.1) – the fundamental decoupling of economic growth from resource use nevertheless implies significant changes to industrial strategy. This is likely to meet resistance from governments and industry. Without meaningful dialogue at the national and international level around future growth pathways, there is a risk that natural resource-exporting countries will see the CE not as an opportunity for economic diversification but as a threat to continued growth.

2.3 Infrastructural deficits and urbanization

Key to visions for a CE in developed countries has been the opportunity to tap into an economy’s existing stock of materials – through the dismantling and recycling of e-waste, organic waste and construction materials, for example – and so displace primary production and its associated energy requirements and greenhouse gas emissions. Resources available in unused assets and products, and in abandoned buildings and infrastructure, can be brought back into circulation in a number of ways. Governments may incentivize the reuse of existing buildings over new builds: for example, the UK could remove the 5 per cent value-added tax (VAT) charged for converting buildings into housing, or introduce fiscal measures such as ‘landfill taxes’ to encourage remanufacturing over waste disposal.