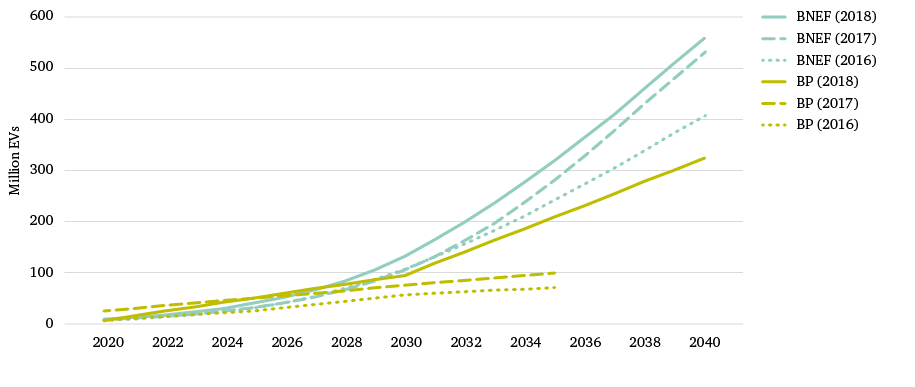

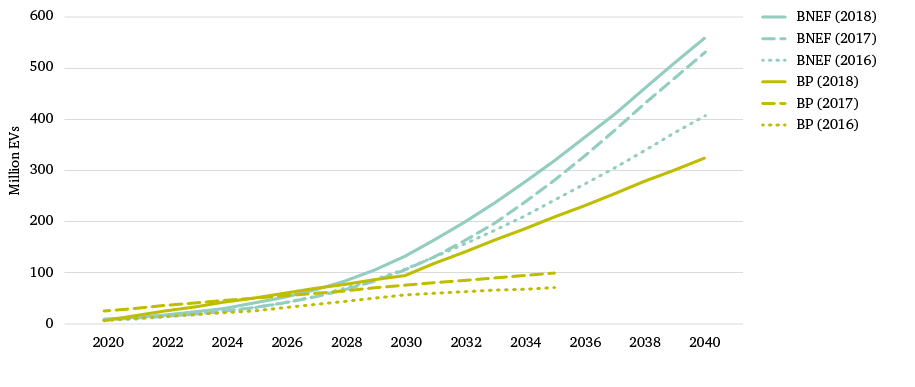

Over the past 10 years or so, projections of EV penetration have, almost without exception, dramatically understated actual penetration levels. Figure 4 shows that major forecasters’ estimates of the size of the global EV fleet have typically been adjusted upwards from one year to the next. That these underestimates are so prevalent is surprising given that EVs tick all the right boxes in terms of attributes for energy technologies. They tick the security-of-supply box. If the Strait of Hormuz – a key transit route for oil – is somehow closed, the consuming countries most reliant on petrol or diesel will be the most affected. The higher the penetration of EVs in a given country, the lower the likely impact of disruptions to oil supply. EVs also tick the environmental impact box – with the caveat, in relation to climate concerns, that this assumes that the electricity such vehicles use is generated by renewables, which may not always be the case. In terms of impact on urban air quality, support for EVs assumes that diesel vehicles are displaced. Finally, EVs also present a potential solution to renewables’ problem of ‘intermittency’ – where natural fluctuations in generation (e.g. when the sun doesn’t shine or the wind doesn’t blow) create reliability-of-supply issues and may require costly back-up generation. Intermittency in renewables can be solved, at least in theory, by storage. One option for short-term grid management is to use batteries. A large car parc would provide significant storage capacity. Thus, the practice of a car in a garage being charged overnight can be replaced by one of a car discharging electricity to supply the grid – with its owner, of course, being paid for it. An even more exciting prospect is that roads could be built with induction strips so that the car can charge itself while driving (Lumb, 2018).

The prospect for a more rapid spread of EVs looks good as the costs of EVs fall, in line with the rapid development of battery technology. Between 2010 and 2016 the costs of an EV battery fell by 73 per cent (BNEF, 2017), and further falls are expected.

Between 2010 and 2016 the costs of an EV battery fell by 73 per cent, and further falls are expected.

Of course, there are barriers to the spread of EVs (Quiggin, 2017). There has been much concern over the availability of lithium, the basis for much of the battery capacity in many EVs. Such concern has arisen because of lithium’s frequent classification as a ‘critical metal’. However, the designation ‘critical’ does not necessarily denote scarcity; it can refer to the criticality of the mineral for certain economic sectors, or the concentration of supply chains. Indeed, the large multinational mining companies are combing their historical records, since historically lots of lithium was found but ignored as having no value. Cobalt, with its heavy reliance on supply from the Democratic Republic of the Congo (DRC), presents another potential supply bottleneck for battery makers. However, researchers are trying to develop batteries that are less cobalt-dependent (Chandler, 2017).

A widespread shift to the use of EVs also has implications for managing and expanding the power grid. If large numbers of motorists drive home and plug in to recharge their EVs at the same time, it could create an unacceptable peak load on the system. However, this should be manageable given modern metering technology. There is also the issue of access to charging points. Not everybody has a garage, an issue potentially of particular relevance for car ownership in high-density urban areas. Thinking about solutions to the environmental challenges posed by the rise of mega-cities requires ideas other than those related to individual car ownership.

It is also increasingly clear that there is a growing policy drive by governments and automotive manufacturers to develop EVs and phase out internal combustion engines (ICEs). Most notably, recent discussions have considered banning diesel vehicles from many cities because of their contribution to particulate pollution. Many national governments have come out with statements illustrating their desire to phase out ICEs and encourage the use of EVs (S&P Global Platts, 2018). China has indicated that one-fifth of new cars will be plug-in or hybrid by 2020, and the authorities there are reported to be ‘researching a time line for a complete ban on ICEs’. What happens to EVs in China could be crucial to the future of EVs internationally (Butler, 2018), in much the same way that industry developments in China have significantly influenced the costs of solar panels. Both the UK and France have said they will halt production and sales of ICEs by 2040. The Indian government has claimed that all new cars sold in India will be electric after 2030. Germany is proposing an ICE sales ban from 2030. Japan, Austria, Denmark and Ireland are discussing setting targets for EV sales. A similar trend can be seen with automotive manufacturers. Volvo, VW Group and BMW have all stated that all their models will have an ‘electric option’. Toyota and Nissan have also made claims about plans for zero-emission vehicles in the future. In all these cases, it is necessary to point out that talk is cheap. Until specific policy measures to achieve targets emerge, the claims of governments and the automotive industry need to be treated with caution.

BP has suggested that the introduction of an extra 100 million battery EVs would lower oil demand by 1.4 million barrels per day – a reduction of only 1.5 per cent over total consumption in 2017.

Extensive penetration of EVs into the car parc, if it occurs, will not in itself lead to the demise of oil use, and it would be unwise to overstate the anticipated impact of EV growth on oil demand. The IEA estimates that the billion or so ICE vehicles on the road worldwide account for around 40 per cent of global oil demand. BP has suggested that the introduction of an extra 100 million battery EVs would lower oil demand by 1.4 million barrels per day (b/d) (BP, 2017) – a reduction of only 1.5 per cent over total consumption in 2017.

A number of factors complicate the arithmetic of how EVs may affect oil demand in the future. First, there is the legacy of the existing car parc. For example, BP argues in its Energy Outlook (BP, 2018b) that its market scenario in which sales of new ICE vehicles and plug-in hybrid EVs are banned from 2040 assumes that ICEs will still be powering one-third of passenger cars in that year. Second, as EVs begin to dominate the car parc, it is possible that automotive manufacturers will stop investing in research and development to improve ICE efficiency long before any formal ban on ICEs comes into force. This would significantly slow the reduction in oil demand expected from improved energy efficiency. Having said that, much of the improved performance of ICEs over the years has been the result of legislation in the US (for example, the CAFE standards introduced in the 1970s), EU emission standards and policy in China, as part of efforts to reduce dependency on oil imports. There is no reason to assume that effective policy measures cannot be sustained and/or developed in ways that would force automotive manufacturers to continue improving ICE performance.

In terms of the implications for oil consumption, transport is not the only variable to consider, as passenger vehicles that could be replaced by EVs account for less than 20 per cent of total oil demand. Many oil consumption forecasts also assume that the role of oil as a feedstock for petrochemicals will add significantly to future demand. For example, the IEA projects that one-third of the growth in oil demand by 2030 will come from petrochemicals, rising to almost 50 per cent by 2050 (IEA, 2018b). However, as noted earlier, the IEA is arguably highly optimistic about future oil demand. Also, its projection does not take account of growing concerns about the pollution caused by plastics that fail to degrade. This raises a legitimate question: is plastic likely to be the ‘new tobacco’ in popular opinion, and might we thus expect a strong groundswell of activism seeking to reduce demand for petrochemicals in the future? This possibility is reinforced when one realizes that 40 per cent of plastics are used for packaging (Parker, 2018), much of which might reasonably be deemed a non-essential luxury.

There are also other factors at work in relation to oil demand. It is clear that car ownership is declining among much of the younger generation in OECD countries. Rapid urbanization and the spread of asset-sharing models – e.g. car clubs and ride-matching services such as Uber – point to declining car ownership and thus, potentially, lower oil demand in the future. This will be especially true if city planners prioritize public transport and connected-mobility solutions as part of policy efforts to achieve climate and clean air objectives.

Other technological changes

Other areas of technological change may also influence future demand for oil. First, there is the role of artificial intelligence (AI) and automation, which promise to create a so-called ‘fourth industrial revolution’. This takes the third industrial revolution, namely the digital revolution linked to computers and automation, and adds to it cyber physical systems whereby operations are controlled by algorithms integrated into the internet (Schwab, 2016). The implications of this for energy consumption are far from clear. For example, self-driving cars might be expected to operate in a more fuel-efficient manner. But at the same time, there is an interesting potential contradiction between electricity use and information technology. Greater use of information technology may save electricity on the one hand, but on the other hand it may lead to increasing electricity consumption to generate the technology in the first place. AI, automation, the ‘big data’ revolution and the rise of blockchain computing are emerging as important sources of potential disruption to markets and industries. How specifically all this might affect oil and energy consumption is not entirely clear. It might be assumed that all of these developments in communication and connectivity lead to greater operational efficiency, which would improve energy efficiency. For example, already the oil industry is increasingly using big data both to lower upstream costs and to streamline the transport, refinement and distribution of crude oil and oil products (Marr, 2015; Zaidi, 2017). The development of hydrogen-based fuel cells could also be a source of unexpected disruption to oil industry dynamics. It might also be argued that such technical developments will allow a more flexible power sector to emerge, enabling more renewables to be integrated into the power grid, leading to lower costs.

Another oil price shock?

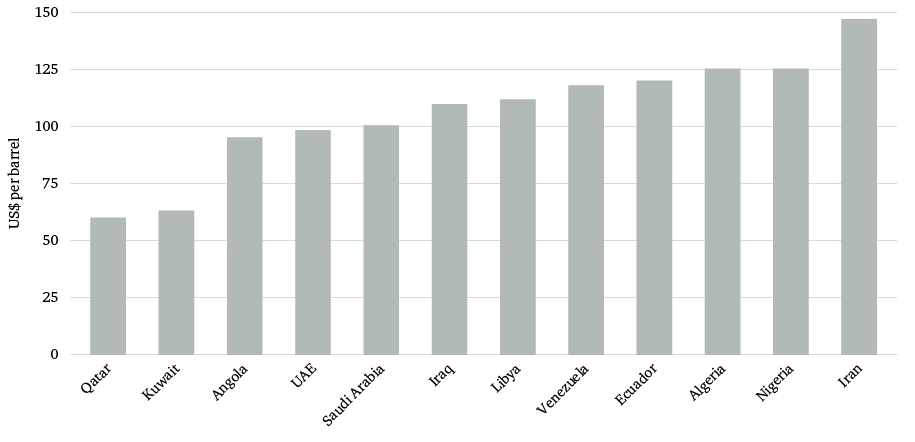

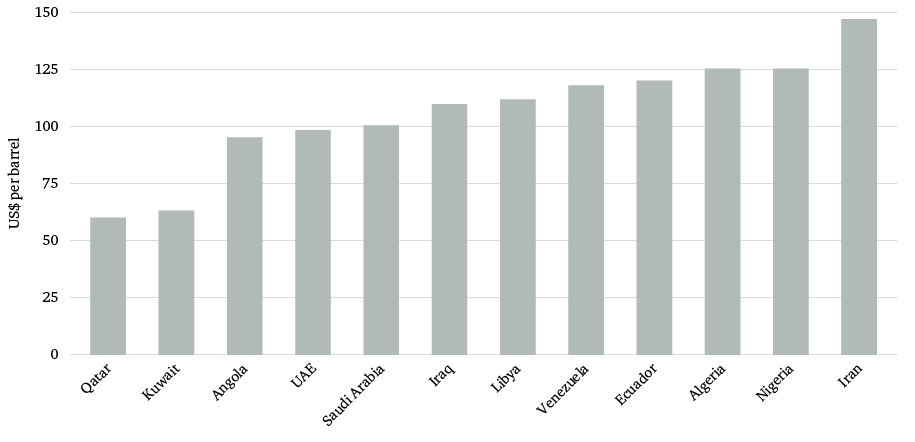

The MENA region, which accounts for 38.6 per cent of global crude oil exports and 51.4 per cent of global proven oil reserves (BP, 2018a), is currently extremely unstable. Indeed, in the view of this author it is necessary to go back to 1918, at the end of the First World War and during the collapse of the Ottoman Empire, to find a period when the region was so unstable and unpredictable. Furthermore, there is a serious possibility of even greater instability to come. Lower international oil prices since mid-2014 have caused serious problems for oil-producing governments in the MENA region, reducing their ability to assuage domestic political unrest through public spending. Figure 5 shows the budgetary break-even oil price for OPEC members shortly before the oil price collapse of 2014.