There is a tendency among energy analysts to forget the time lag between price movements and changes in oil demand. Oil demand is what is termed a ‘derived demand’. No one wants a barrel of petrol or a bag of coal. Energy consumers want energy services – light, heat and work. To secure these services requires the use of energy-consuming appliances. A three-stage process therefore affects energy consumption. It involves a series of choices that ultimately determine oil demand. The first is whether to buy the energy-using appliance or facility. While the price of the appliance matters, of greater importance is the income of the consumer. As incomes rise, more appliances are purchased.

The second choice is what type of appliance to buy. Here there are two issues: which fuel should power the appliance, and whether an efficient or inefficient appliance should be preferred. The choice of fuel is determined by the technology. A jet aircraft requires the use of jet fuel, but boilers to generate steam can depend on a variety of fuels. A key determinant of the choice of fuel, depending on the technology available, is the current price of fuels. However, expectations regarding future energy prices are probably an even more important factor. As to efficiency, at least historically, more fuel-efficient appliances tend to command higher purchase prices. So this presents a trade-off between the initial price of the appliance versus any savings on running costs that may result from higher fuel efficiency. Once these choices have been made, the appliance stock is fixed for a significant period (as it takes time to change the appliance stock to any extent). For example, the car parc normally takes around 15 years to change, and the housing stock well over 50 years.

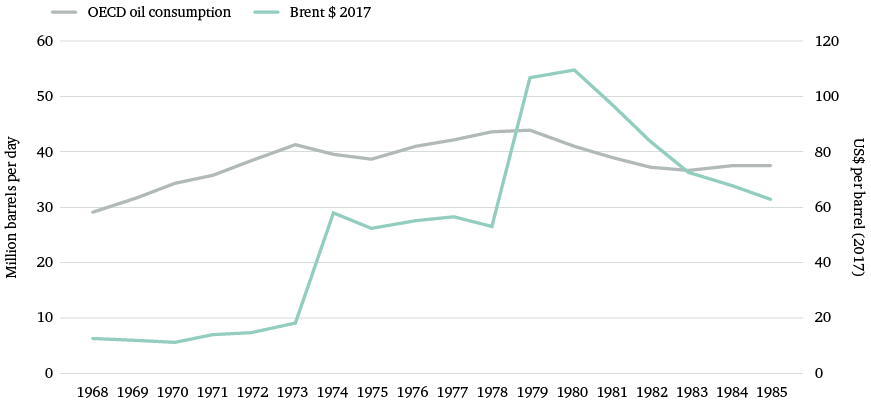

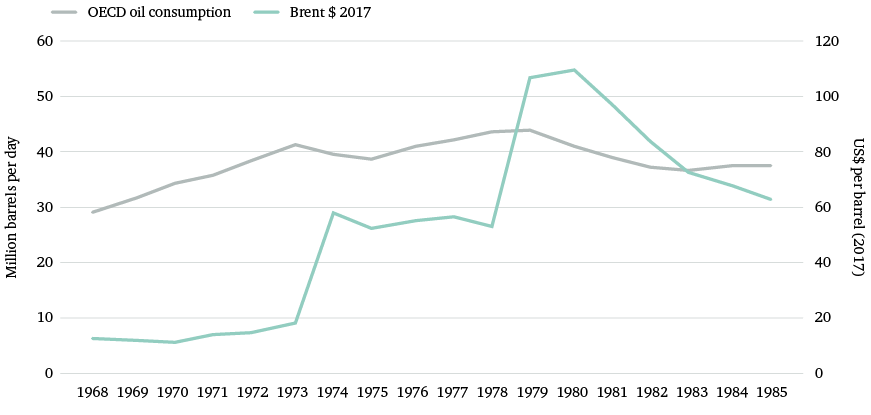

Once the appliance stock is fixed, the third and final choice in determining demand for fuel is the capacity utilization of the appliance. Here there is an important conceptual distinction between ‘conservation’ and ‘deprivation’. Doing more or less the same thing with lower capacity utilization constitutes conservation, and can be viewed as a desirable action. However, to save energy through zero capacity utilization – e.g. turning off all the lights and sitting in the dark – is ‘deprivation’. This might be seen as undesirable. In the short run, when the appliance stock is fixed, and if no deprivation is to occur, it takes time for higher oil prices to reduce fuel demand to any significant degree. Thus, the higher prices experienced between 2004 and mid-2014 will take time to reduce oil demand significantly, but they surely will. The experience following the oil price shocks of the 1970s provides a classic example of this phenomenon of lagged demand response, as briefly outlined in Box 1.