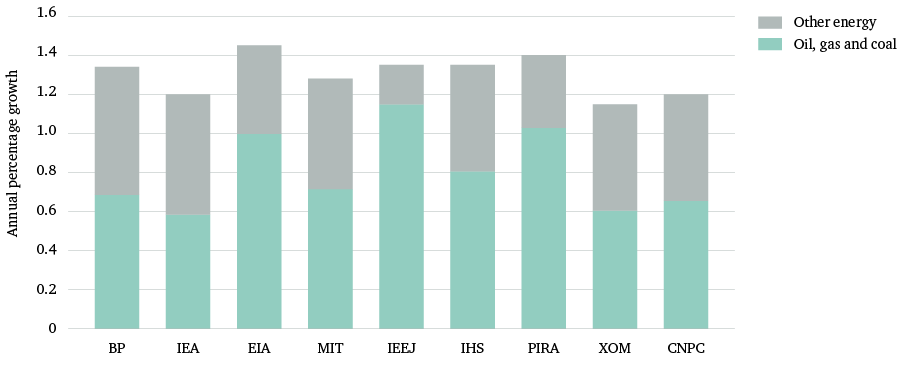

A selection of forecasts by the ‘energy establishment’ is presented in Figure 10. The main observation is that, in the opinion of this author, they underplay the depth and speed of the current energy transition. All of the institutions cited in Figure 10 continue to assume that hydrocarbons will go on dominating the primary energy mix.

It is interesting to speculate why this is the case. One possible explanation is that they are right, and that hydrocarbons will in fact continue to dominate. In most cases, the forecasts contain arguments to justify this view. However, there are other possible explanations. The first is the phenomenon of ‘forecaster cluster’. It is difficult to forecast major changes in trends. It is also very difficult, if not impossible, for a forecast to identify the specific discontinuities in trends that will seriously damage the accuracy of the forecast. Therefore, there is safety in hewing to conventional wisdom, on the basis that ‘if you are wrong, so is everybody else’. There are other factors applicable to specific institutions. In 1974, in the wake of the first oil shock, Henry Kissinger, then US secretary of state, created the IEA in an attempt to dilute the power of the OPEC countries, and to scare consumer-country governments into reducing their imports of oil. It is part of the IEA’s institutional DNA to convince the world that oil demand will continue to grow, and that this will create serious vulnerability for oil-importing countries. At the same time, the IEA is regarded by many as the benchmark for energy forecasting. Other forecasters therefore tend follow its lead. This is despite the fact that over the years many have pointed to the IEA’s relatively poor forecasting record (Huntington, 1994; Mackenzie, 2017; Wachtmeister and Höök, 2018). For example, according to Paolo Scaroni, the chief executive of Italian energy firm Eni: ‘The International Energy Agency (IEA) has consistently overestimated oil demand since 2004, leading many market operators to predict an impending oil crisis’ (Reuters, 2009). More recently: ‘Organizations such as the IEA are consistently behind the curve in their predictions of renewable costs and deployment’ (Carbon Tracker, 2015).

As for the IOCs, they are in a difficult position. Given their dependence on shareholders, they can hardly produce a public forecast that predicts a serious decline in demand for their main product.

However, many other groups take a very different view of market prospects, one far more supportive of the view that the transition away from hydrocarbons will be faster and deeper than expected by the energy establishment. Some examples are provided below.

The financial community

Compared to the established energy forecasters, the financial community appears far more supportive of the idea of a rapid energy transition. One obvious reason for this is that it does not have the same vested interest in the status quo. Its mandate – i.e. to protect investor wealth – allows and in fact requires its members to be more dispassionate about oil demand prospects.

This view was encapsulated in a speech by Mark Carney, the governor of the Bank of England, to Lloyds of London in 2015 (Bank of England, 2015). Another example can be found in the views of BlackRock, a global investment management corporation: ‘… a deep structural shift is underway in how the world’s power industry, homes and transportation operate. The implications for infrastructure investors are significant’ (BlackRock, 2018).

The World Economic Forum (WEF) also takes the view that ‘the world’s energy systems are going through unprecedented transition driven by new technological opportunities, policy shifts and change in energy consumption’ (WEF, undated).

Increasingly, there are efforts by financial managers to include the integration of ‘transition risk’ into investment management frameworks and financial stability regulations.

Increasingly, there are efforts by financial managers to include the integration of ‘transition risk’ into investment management frameworks and financial stability regulations.

The consultancies

A number of consultancies are more aggressive in their views of the speed and depth of the transition. Bloomberg New Energy Finance (BNEF), as can be seen from Figure 4, has been far more optimistic than other forecasters about the penetration of EVs. McKinsey for some time has also been more positive on the issue. Thus: ‘… Globally, energy systems are experiencing significant and fast change’ (quoted in Hund et al., 2012).

Others

The ‘divest campaign’, which lobbies financial investors to avoid investing in companies that produce or use hydrocarbons, has been influential in warning investors about the dangers they face from the current transition. The spread of this campaign, which began in the US, has been impressive (Vaughan, 2014). Many investment funds have announced that they will no longer buy into companies associated with carbon production and use. Several good examples (albeit rather strange ones, given their oil-sector origins) include the Rockefeller Foundation and the Norwegian government pension fund. Linked to this campaign is also the work of Carbon Tracker (Carbon Tracker, 2015), a London-based think-tank, which has been warning of the dangers of ‘straight-line syndrome’ in the energy establishment’s forecasts (ibid.).

Academia

There is also global pressure from university campuses across the world, pressure which to this author is reminiscent of the anti-Vietnam War movements of the 1970s and the anti-apartheid movements of the 1980s. This view is reinforced by the phenomenon of schoolchildren in many parts of the world beginning to hold ‘strike days’ to register their frustrations at the lack of policy action by their governments (BBC, 2019).