Many barriers must be considered when planning policy for economic diversification. The first and main barrier is the nature of the ruling elite. In many oil-producing countries, the ruling elite is effectively a kleptocracy whose position has been reinforced by many years of securing oil revenues to support its own interests. By definition, this elite has no incentive to change the status quo. Indeed, its interests are to maintain the sources of its wealth and power. This goes back to the debate in the former Soviet Union at the time of Mikhail Gorbachev, who argued that economic liberalization (perestroika) was not possible without political liberalization (glasnost).

A number of issues follow on from this view of the world. First, diversification requires a dynamic and active private sector. However, to achieve this requires secure property rights and the rule of law, to protect private investors. At the risk of oversimplification, it is not unreasonable to assert that a kleptocracy comes into existence because the ruling elite is not constrained by law. A good example of this has been the recent experience in Saudi Arabia. Following the oil price collapse in the summer of 2014 and the rise of Mohammed bin Salman with the accession in January 2015 of his father, King Salman bin Abdul-Aziz Al Saud, there have been extensive plans to reform the Saudi economy and diversify away from dependence on oil. This has been embodied in the Vision 2030 process. However, in October 2017 more than 100 senior Saudi figures, including many members of the royal family, were arrested and held in detention in the Ritz Carlton Hotel in Riyadh. They were held there until they agreed to pay ‘fines’. It is far from clear what the legal basis of this action was. It simply appeared as a whim on the part of the crown prince and his supporters. One obvious consequence, not surprisingly, has been that private-sector investment in the kingdom has dried up, causing growing concern about prospects for the non-oil economy. Indeed, it has been estimated that since the detentions there has been a capital outflow from Saudi Arabia of more than $100 billion (Dudley, 2018).

A second barrier is that many oil-producing economies suffer from high degrees of state interference in the economy, together with significant distortions associated with mechanisms such as subsidies. This in part reflects the social contract between the rulers and the ruled that has dominated in many oil-producing countries. In return for its acquiescence, the population is given access to goods and services on preferential terms. Changing this social contract is essential for economic reform. However, it is not easy, since it invariably requires the removal of subsidies, which leads to higher prices of basic goods. It also requires political reform on the grounds that there should be ‘no taxation without representation’. This requires the ruling elites to relinquish at least some degree of power and influence. Given that such elites gain so much materially from their exercise of power, voluntary relinquishment is not a plausible option.

A third potential barrier to developing the private sector is the availability of the entrepreneurship and skilled labour required by a modern, increasingly digital, economy. In particular, in many oil-producing countries in the Middle East, the quality of publicly provided education is abysmal. For example, one-third of the curriculum in Saudi Arabian elementary schools consists of ‘Islamic studies’, i.e. rote learning of the Qur’an; in secondary education, the share is still one-quarter. In the kingdom’s universities, some two-thirds of students earn degrees in ‘Islamic studies’ (House, 2012). This is not an adequate preparation for a workforce in a modern economy. Attempts at reform have consistently been resisted by the religious establishment, which the Al Saud family needs to keep on board in its attempts to contain pressure from Islamist militant groups such as Islamic State of Iraq and Syria (ISIS) and Al-Qaeda in the Arabian Peninsula (AQAP).

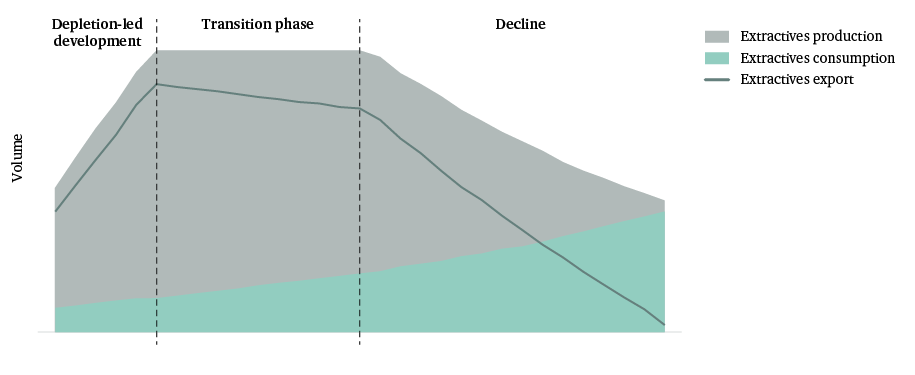

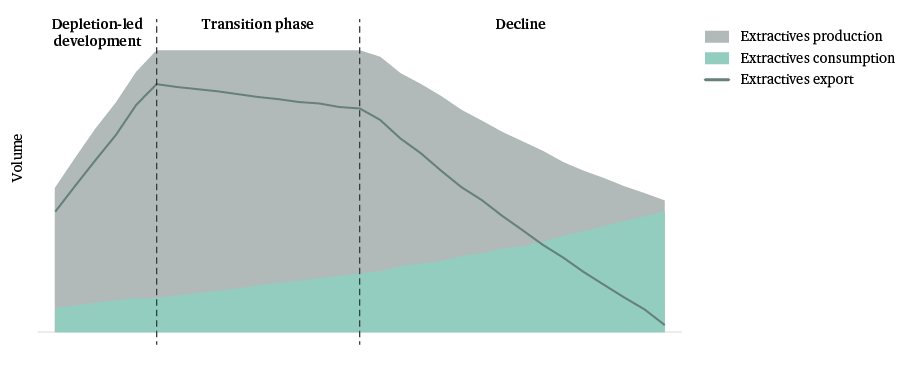

Many of the countries currently dependent upon oil are likely to face increasingly serious economic problems and, as a result, domestic political unrest.

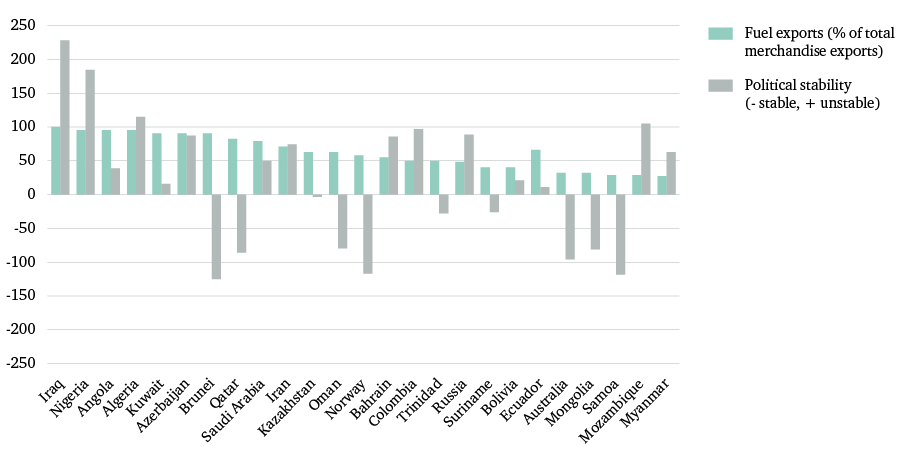

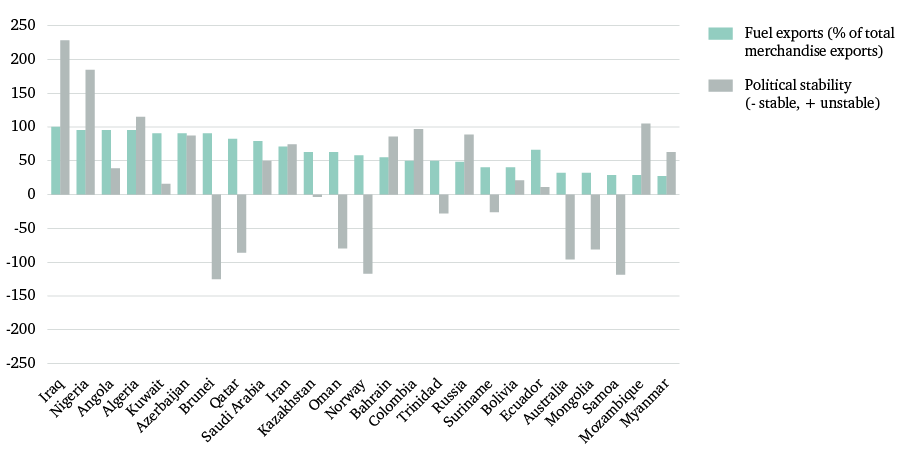

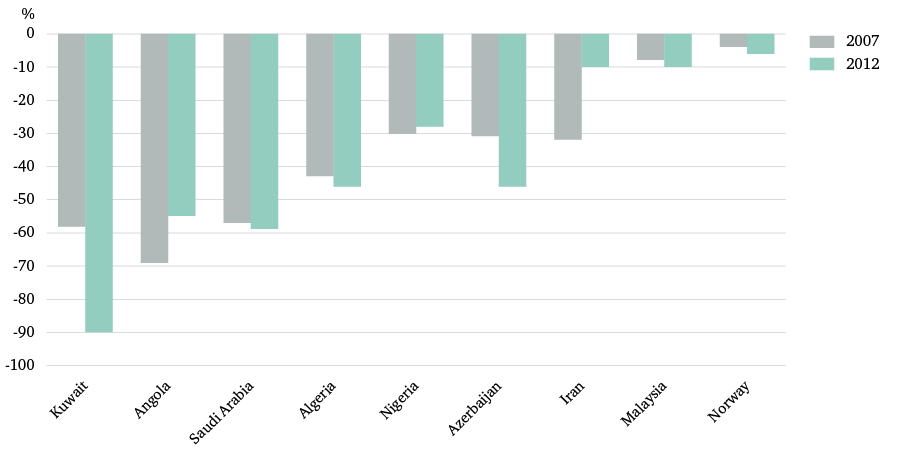

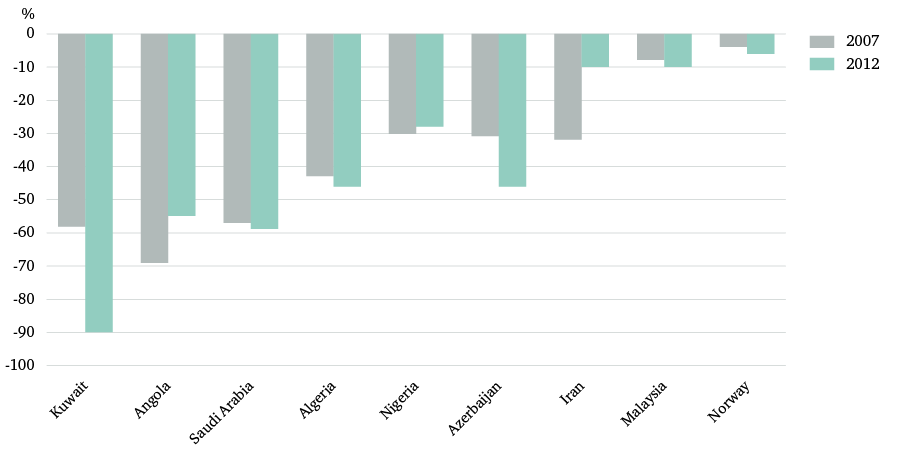

All these barriers present a formidable problem for any Middle Eastern government that is serious about trying to diversify its economy away from oil. There have been some signs of success in a few cases: for example, in Iran and the United Arab Emirates, where oil’s contribution to GDP and government revenues has fallen. However, in most cases the prospects are not good. Thus, many of the countries listed in Figure 11 as currently dependent upon oil are likely to face increasingly serious economic problems and, as a result, domestic political unrest. This risks fuelling regional conflicts that could further destabilize the MENA region, as outlined in Section 3. This in turn increases the imperative for oil-consuming countries to reduce their exposure to oil price instability, thereby increasing the likely pace of the transition to non-hydrocarbon energy. This is a vicious circle as far as the oil-producing countries are concerned.

All of this leads to the final question of this paper: what will be the geopolitical fallout as the energy transition proceeds and speeds up?