This briefing note is the result of a collaborative research process with the Zimbabwean private sector, government representatives, industry organizations and experts, drawing on best practice and senior-level insights to identify policy options for long-term economic revival and expansion in Zimbabwe, and pathways for inclusive development.

Supporting Growth Along the Value Chain of Zimbabwe’s Multi-land-use Economy

The two overarching priorities for facilitating growth to 2030 are enforcing land and property rights, and creating pathways to formality across sectors and value chains. Zimbabwe has a complex structure of land ownership and use, including commercial, smallholding and subsistence farmers, hunters and communities, on land that can be state, private or communal. The private sector requires a workable land management system that will allow it to attract investment and grow, built on respect for and enforcement of property rights to ensure security in land ownership, leaseholding and economic usage. Land in Zimbabwe remains a contentious issue in the wake of the Fast Track Land Reform programme of the early 2000s, but the issues are much broader than expropriation of commercial farmers. There is a need for clarity over usage rights between farmers and miners on state-owned land being used under tenure. The lack of enforcement of land rights is also putting pressure on environmental resources – with informal tobacco farming creeping on to the fringes of national parks, for instance.

Long-term economic planning for job creation and growth also needs to reflect the reality that most Zimbabweans subsist in the informal sector. Some 94.5 per cent of Zimbabwe’s employed population aged 15 years and above were considered to be working in the informal economy at the time of the 2014 labour force survey.45 There is a need to better understand the make-up and role of the current informal economy, and to design policies that can bring the benefits of formalization – including higher wages, and improved health and safety practices and protections – without unduly stifling enterprise: the informal sector has provided an important safety net in a fragile economic context; and informal businesses are frequently wary of government intervention.

Agriculture

Agricultural activities provide direct employment and income for 60–70 per cent of the population of Zimbabwe, but agriculture, forestry and fishing contributed only 12 percent to Zimbabwe’s GDP in 2018.46 There are considerable variations in scale and efficiency within the sector. Commercial agriculture is a major driver of other economic activity, providing around 60 per cent of raw material inputs for manufacturing, and a producer of cash crops – chiefly tobacco – for export.47 Small-scale farming is a primary source of subsistence for much of the population, and is a key factor in livelihood resilience and poverty levels. There is a considerable challenge for policymakers in addressing the priorities and needs of producers at all scales.

In order to be competitive, Zimbabwe needs to develop economies of scale that can in part be achieved through high-tech estate farming. Agribusinesses need to be encouraged in ways that can foster managerial skills and develop sophisticated supply chains, as well as support production of cash crops that have long payment horizons. For instance, tree crops like coffee or oranges require significant investment but are not revenue producing for at least four years, and thus are beyond the reach of most smallholders. Care will need to be taken that agribusiness does not expand at the expense of all those who also have a right to the land, and that it provides jobs and training for those who may potentially be displaced. Labour-intensive agriculture could also be encouraged,48 although water intensity involved in production should be considered when identifying potential new crops, and policy structures need to enable the development of irrigation infrastructure. Horticulture exports have doubled in 2018–19, albeit from a small base. Significant opportunities exist for expanding production of fruit and salad products, including to provide a winter buffer for food retailers and restaurants in South Africa. Commercial farms in Zimbabwe also have an important role to play as ‘nodes’ of economic activity, connected into local supply chains and drawing inputs from the surrounding area through outsourcing and supporting a local market for agricultural services.

Adopting new technologies will also be an important step for Zimbabwe’s agricultural sector. Improved communication systems will enable farmers to share information, including on ‘climate-smart’ agricultural practices, have better access to weather forecasts, and make better advanced planning choices, as well as promote access to agricultural futures markets. Technologies such as blockchain may also help smallholders with no land tenure to build a credit history in order to access capital.49 However, the roll-out of new technologies needs to be supported by training and promotion, including through traditional channels such as radio, to ensure that small-scale farmers are aware of these services. New technologies will also be used for mapping and categorization of land, and boundary definition. Critically, such developments must be supported by the establishment and empowerment of a land tribunal as well as effective local dispute resolution mechanisms.

A revived agricultural sector is key to reversing the trend of deindustrialization in Zimbabwe, and not only in terms of supply of raw materials for processing. Agriculture is an important purchaser of manufactured products at every level. Large commercial farms provide a small market for more mechanized farming products, but there is also a significant market for basic mechanization and simple capital. But margins can be narrow, and so selling at high volume is in most cases crucial.50 The Confederation of Zimbabwe Industries and the Ministry of Industry and Commerce have identified 18 value chains that link resource sectors – i.e. agriculture and mining – to manufacturing. For agriculture, this includes cash crop production such as tobacco or cotton, manufacture and assembly of machinery, and leather goods.51 To take one example, in 2000 Zimbabwe was producing 17 million pairs of shoes, but economic crisis and rising competition subsequently meant that by 2011 output had fallen to only around 1 million pairs. With almost two-thirds of hides now exported raw, the number of tanneries fell from nine to just four by 2013.52 If the government creates the necessary enabling environment, agriculture could be a key example of a sector where it is possible to reverse decline and create jobs across the value chain.

Productive agriculture in Zimbabwe reflects the legacy of land reform programmes, including phases of post-independence resettlement after 1980, and the Fast Track Land Reform programme of 2000. All agricultural land in Zimbabwe is held by the government in trust and leased to farmers. Establishing security of tenure will be critical to the revival of the sector: uncertainty leads to short-termism, with farmers being reluctant to undertake large capital investment projects, such as installing long-term irrigation systems.53

Tenure is also critical to unlocking finance, in particular for mid-sized and large operations. Improving access to finance was identified as a priority by the Zimbabwe Land Commission in the first phase of its National Agricultural Land Audit, conducted in late 2018. The land audit recommended an integrated Land Information Management System to address shortcomings related to fraudulent land allocations, illegal leasing and the underutilization of potentially productive land.54

Guaranteeing secure tenure does not have to mean a move to an entirely freehold system. The Rukuni Commission on land in 1994 recommended a multi-form tenure system.55 It can provide for communal usage and protect access rights, as well as protecting leaseholder arrangements for larger properties that require collateral. Representatives of the domestic private sector have also suggested the establishment of a market mechanism on land holding to allow the development of economies of scale and improve efficiency through large-scale, high-tech and highly mechanized farming.

Mining

The government has announced its ambition for Zimbabwe to have a US $12 billion mining industry by 2023, a more than fourfold increase from 2017. In August 2019 the cabinet discussed a paper submitted by the mining minister, Winston Chitando, setting out the roadmap to achieving this target.56

If this ambition is to be realized, the government’s primary objective must clearly be to attract investment into the sector. Zimbabwe’s Chamber of Mines estimated that in 2018 the industry required $777 million for maintenance and increasing operations.57 Like other sectors, mining has long suffered as a result of chronic power and infrastructure deficits; it has also been impeded by policies that have acted as disincentives to international investment, such as indigenization and foreign currency restrictions. In 2019, however, Minister of Finance Mthuli Ncube announced investment ‘megadeals’ worth some US $8 billion into the mining sector.58

The Fraser Institute’s most recent Annual Survey of Mining Companies, conducted in August–November 2018, placed Zimbabwe in the bottom 10 jurisdictions for investment attractiveness, on the basis of policy uncertainty, the legal system and uncertainty on land dispute resolution.59 Although it will take time for the government to build a track record and establish confidence among investors, there are some steps that can be taken in the short term to improve investor sentiment. For example, it should reduce the time it takes to execute Bilateral Investment Protection Agreements (BIPAs), and licensing arrangements should allow companies to invest in exploration without fear of expropriation by the state. Meanwhile, the prevailing uncertainty means that there is no incentive for companies to submit reports on geological surveys to government, and thus there is no holistic geological picture of the whole country.

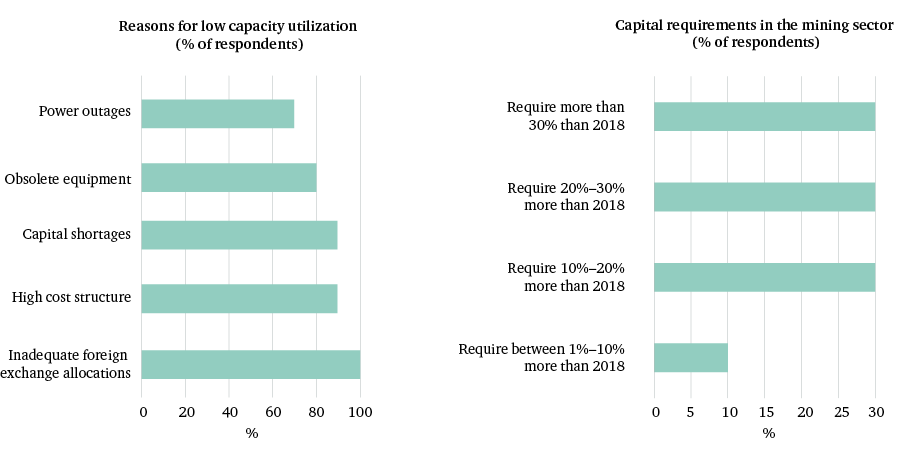

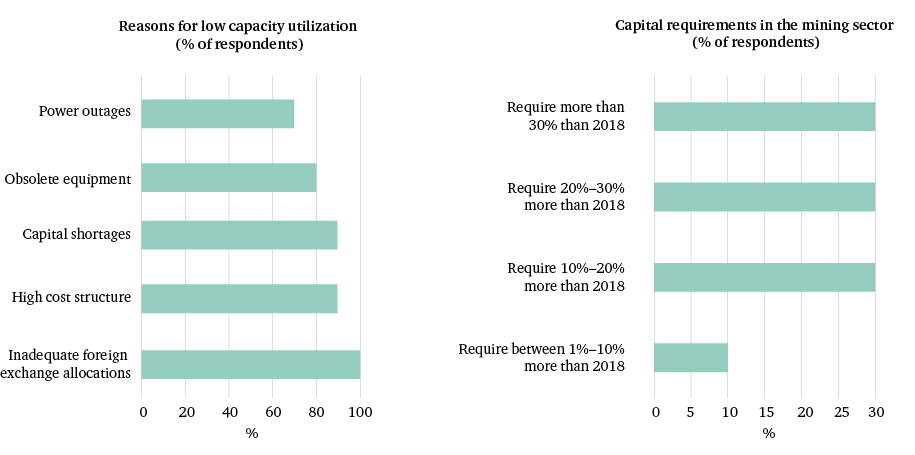

Figure 2: Zimbabwe mining sector survey responses: causes of underutilization, and capital requirements

— Source: Chamber of Mines of Zimbabwe (2018), State of the Mining Industry 2018 Report: Prospects for 2019, using 2018 survey data.

Figure 2: Zimbabwe mining sector survey responses: causes of underutilization, and capital requirements

Zimbabwe’s 2018 State of the Mining Industry survey report assessed the mining industry’s policy priorities as being: establishing a more competitive business environment; simplifying and streamlining royalties, taxes and the rules around value-addition, and benchmarking these to other regional players; and improved title management, including avoiding overlapping titles.60 The survey also points to currency, and financial and physical capital shortages as the biggest impediments to expansion. 60 percent of mines require more a more than 20% increase in capital than they received in 2018 (see Figure 2).

To complement parliament’s ongoing review of new mining legislation, a special committee, involving representatives of industry and civil society, should be formed to identify international best practice – drawing on the mining acts of countries such as Australia and Canada, for example – and make recommendations to government.

The ongoing review of the Mining Act and mining practice is key. As part of this, government should ensure a clear ownership structure for mining assets to guarantee security of tenure and encourage exploration. It should also set out clear valuation and compensation mechanisms for those using land absorbed into expanded mining activities, and streamline taxes and royalties.

The government needs to clearly communicate its vision for how the mining industry can contribute to national development, in particular how society can have a just share of the benefits extractive resources. Currently, mining contributes little to government revenue relative to the scale of the industry.61 The approach to benefit transfer taken by the Zimbabwean government has previously focused on ownership. The indigenization policy acted as a primary mechanism by which Zimbabwe could benefit from its businesses, including in the mining sector, by promoting local ownership. Furthermore, the government sought to extract benefit through state ownership of mining assets, through the Zimbabwe Mining Development Corporation (ZMDC). But Zimbabwe’s state-run mines have failed to deliver benefits to its citizens. As part of the current reform process, the indigenization requirement has been dropped, and ZMDC has been listed as one of the enterprises in line for privatization, sale of assets or entering into joint ventures.62

The government must now ensure that a transparent and fair tax and royalty regime means that the state gets a fair return from the mining industry over the long term, and allows citizens to feel the value that this creates. Zimbabwe is in a position where it needs to offer generous conditions in order to attract and retain foreign investors.63

Civil society actors have welcomed the government’s stated commitment – including in the 2019 national budget statement – to joining the Extractive Industries Transparency Initiative (EITI). Adherence to best-practice initiatives such as the EITI can provide important third-party reassurance for companies interested in investing in Zimbabwe. Earlier attempts under the Mugabe administration to create a national equivalent, the Zimbabwe Mineral Revenue Transparency Initiative (ZMRTI), were unsuccessful, and there is limited appetite from partners within the Mining Industry Association of Southern Africa, chaired by Zimbabwe, to adopt a specific regional initiative. If Zimbabwe does join the EITI, this will be an important signal of the government’s real commitment to reform.

As part of its commitment to promoting greater transparency, the government should publish revenue payments disaggregated by company and source; and mining contracts and project-specific fiscal terms should be disclosed.64

Informal mining makes a significant contribution to the sector’s output, as well as to foreign currency generation, however the reality of smuggling means that not all revenues are received by government. There are regional examples of best practice for creating pathways to formal status, including through certification schemes. New technologies are providing platforms for this; one such example is TRACR, which uses blockchain to develop a provenance guarantee in the diamond supply chain.65 Linking small-scale miners to big companies can facilitate skills transfers and bring improved health and safety. It is estimated that 80 per cent of artisanal mining in Zimbabwe takes place on land that is owned by mining companies, so both parties have an incentive to work together. There needs to be a more joined-up approach involving artisanal, small-scale and large-scale mining, including linking into beneficiation processes. For example, there could be scope to link chrome into steel production, as well as lithium into battery production. Informal and artisanal mining requires financial support to provide access to geologists, equipment, and training. These could be donor-supported activities under accelerated re-engagement.

Tourism

Tourism is a strategically import sector for Zimbabwe. It is less vulnerable to global exchange rate fluctuations than other export sectors. And wildlife tourism, in particular, can create jobs and support wealth creation in rural areas. Tourism arrival numbers also serve as a barometer of international sentiment towards the country.

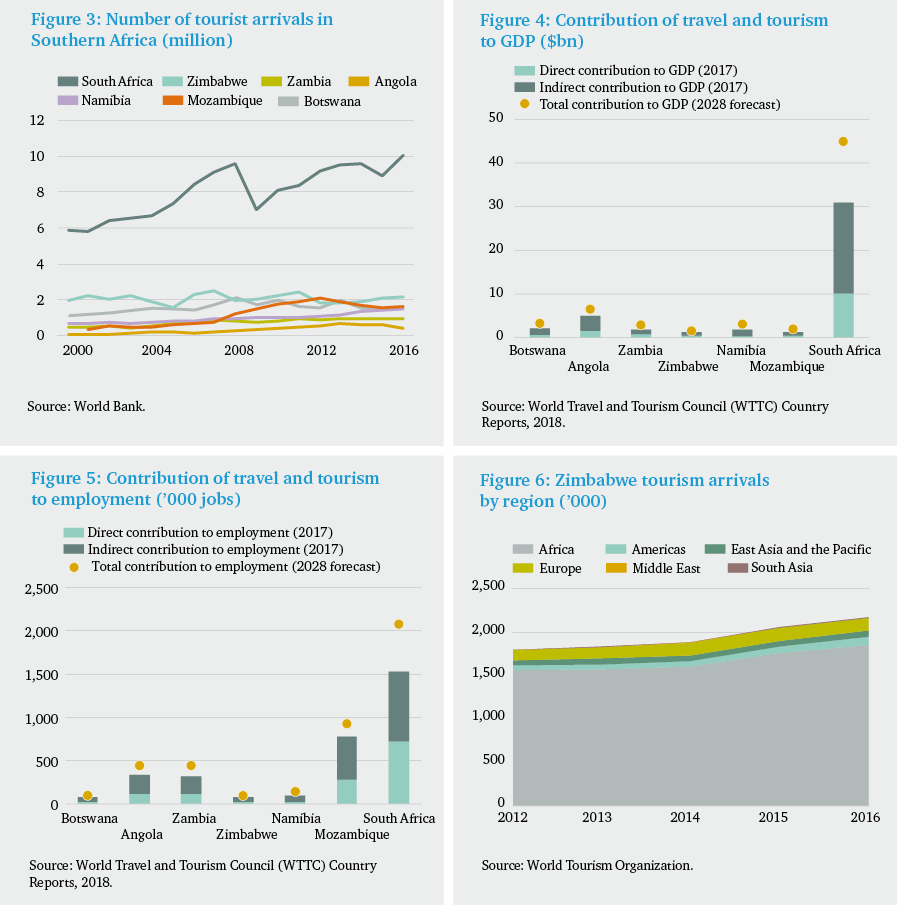

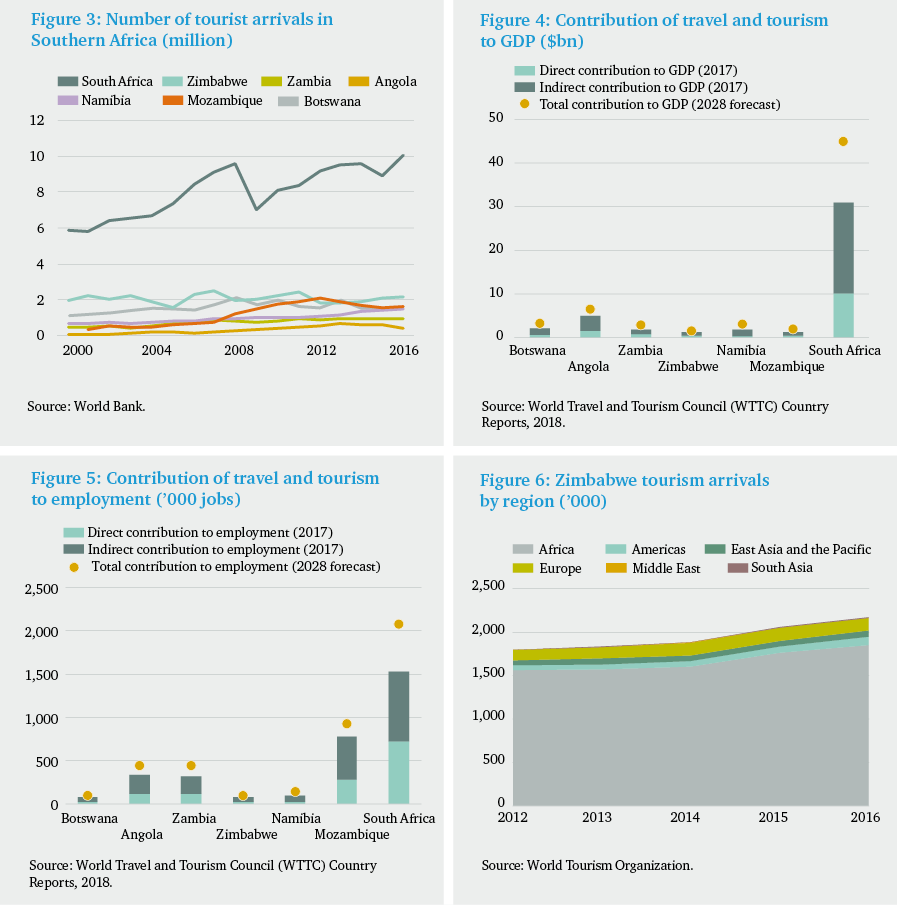

Zimbabwe’s tourism sector – albeit dominated by Victoria Falls as the principal focus of tourism activity and by far the greatest generator of tourism revenue – has proved relatively resilient in recent years, showing signs of renewed growth following a prolonged period of severely reduced tourist inflows from the early 2000s owing to the political situation and economic collapse. There were some 2.4 million tourist arrivals in 2017, up from 1.7 million in 2014.

This resilience is now being tested, however. The tourism sector has suffered operational challenges because of ongoing fuel, power and water shortages. Hotels and restaurants have been unable to operate without electricity or fuel for their generators. Furthermore, a lack of disposable income and the rising cost of living has caused a decline in domestic tourism. Bureaucracy can also be burdensome, and there are quick wins to be made by simplifying regulation and streamlining the number of licences needed by hotels. For example, hotels currently need a licence for each television they have, rather than one for the whole business.

The most significant growth market for Zimbabwe’s tourism is international tourism. In particular, there is potential benefit to be derived from linking into regional tourism routes. Although Zimbabwe typically receives the second highest number of tourists in Southern Africa, it is not converting these numbers into income or employment as effectively as its neighbours (see Figures 3–5). At present, tourist arrivals are predominantly from other African countries (Figure 6). South Africa is by far the most popular tourist destination in Southern Africa for international arrivals. Zimbabwe (and other countries in the region) could tap into this market and encourage visitors to spend longer in the region visiting multiple countries.

Tourism in Zimbabwe: comparative regional indicators

— Sources: World Bank; World Travel and Tourism (WTTC) Country Reports, 2018; Wolrd Tourism Organization.

Tourism in Zimbabwe: comparative regional indicators

Zimbabwe has already taken measures to increase and diversify its tourism arrivals. The refurbishment of the airport and other critical infrastructure at Victoria Falls and elsewhere has brought in international airlines such as Ethiopian Airways and Kenya Airways, and there is further upgrading work in the pipeline.66 Victoria Falls airport also provides a gateway into the Kavango-Zambezi (KAZA) Transfrontier Conservation Area (TFCA), a major regional conservation initiative with considerable tourism potential. As part of the initiative, the introduction of the KAZA ‘UniVisa’ for tourists visiting Zimbabwe and Zambia is an important step in linking into the regional market. These measures could be built on, such as by implementing an e-visa system.

The dominance of Victoria Falls as a tourism hub reflects Zimbabwe’s reliance on ‘Big Ticket’ items, also including Hwange Park and Kariba. There is a need to invest in marketing other attractions to an international audience, including cities, museums and cultural hubs, as well as the traditional options of wildlife tourism, hunting expeditions and Zimbabwe’s natural wonders. This needs to be underpinned by investment in and maintenance of visitor sites, including access roads and facilities at rural sites such as the Khami Ruins.

MICE (meetings, incentives, conferences and events) tourism – in which South Africa has previously been dominant in the region – is also a potential growth sector for Zimbabwe. Business tourism typically brings six times more income than other tourism activities, where fees are paid overseas.67

Zimbabwe’s government must protect wildlife and ecosystems to sustain the eco-tourism industry. The CAMPFIRE (Communal Areas Management Programme for Indigenous Resources) model, which incentivizes conservation by devolving management and usage rights to communities, was regarded as innovative when it was first introduced in 1989. Ensuring genuine local representation in decision-making, in line with other regional initiatives such as the Community Based Natural Resource Management Programme in Namibia, could help revive the programme for the benefit of communities and the resources over which they have stewardship.

45 Zimbabwe National Statistics Agency (2015), ‘2014 Labour Force Survey’, March 2015, Harare, http://www.zimstat.co.zw/sites/default/files/img/publications/Employment/Labour_Force_Report_2014.pdf (accessed 6 Sept. 2019).

46 World Bank (2019), ‘World Bank Data: Zimbabwe Agriculture, forestry, and fishing, value added (% of GDP)’, https://data.worldbank.org/indicator/NV.AGR.TOTL.ZS?locations=ZW&view=chart (accessed 1 Oct. 2019).

47 Chitiyo, K., Vines, A. and Vandome, C. (2016), The Domestic and External Implications of Zimbabwe’s Economic Reform and Re-engagement Agenda.

48 Avocado production was suggested as one example during the Zimbabwe Futures 2030 roundtables.

49 Fresh Plaza (2019), ‘Zimbabwe: Blockchain to release farmers from financial burdens’, 26 June 2019, https://www.freshplaza.com/article/9120797/zimbabwe-blockchain-to-release-farmers-from-financial-burdens/ (accessed 6 Sept. 2019).

50 For example, Zimplow’s Mealie Brand business unit, which is the largest manufacturer and distributor of animal-drawn ploughs, harrows, rippers and planters in Zimbabwe, had a revenue of $12.5 million in 2018 with local sales of 43,490 units. By comparison, the group’s Farmec business unit generated revenue of $17.7m for tractor sales of 166 units. (See annual report: https://africanfinancials.com/document/zw-zimw-2018-ar-00/ (accessed 6 Sept. 2019)).; Mealie Brand’s 48 per cent drop in exports also highlights the pressure that exporters face: the drop could be due to high input costs, or the high value of the US dollar. This reliance on high volume to make up for narrow margins is also prevalent at the retail end of the agricultural value chain. NatFood’s pre-tax profit in 2018 was US $19 million, on revenue of US $298 million, a margin of only 6 per cent. Seven of its 13 subsidiaries were dormant. (See annual report: http://www.nationalfoods.co.zw/Reports/AnnualFinancialReports/NF%20Annual%20Report%202018.pdf (accessed 6 Sept. 2019)).

51 African Development Bank (2018), Building a New Zimbabwe: Targeted policies for Growth and Job Creation, https://www.afdb.org/fileadmin/uploads/afdb/Documents/Generic-Documents/Zimbabwe_Economic_Report_-_Building_a_new_Zimbabwe_Targeted_policies_for_growth_and_job_creation.pdf (accessed 6 Sept. 2019).

52 Ibid.

53 Zimbabwe Futures 2030 roundtable series.

54 Chikwati, E. (2019), ‘Zimbabwe: Second Land Audit On Cards’, allAfrica, 21 May 2019, https://allafrica.com/stories/201905210110.html (accessed 6 Sept. 2019).

55 See Scoones, I. (2018), ‘Zimbabwe urgently needs a new land administration system’, The Conversation, 14 January 2019, https://theconversation.com/zimbabwe-urgently-needs-a-new-land-administration-system-89387 (accessed 6 Sept. 2019).

56 Economic News Network (2019), ‘Zimbabwe Mines Minister Presents Details of $12 Billion Mining Plan’, 22 August 2019, https://enn.news/economy/zimbabwe-mines-minister-presents-details-of-12-billion-mining-plan/ (accessed 26 Sept. 2019).

57 Chamber of Mines of Zimbabwe (2018), State of the Mining Industry 2018 Report: Prospects for 2019, http://chamberofminesofzimbabwe.com/wp-content/uploads/2019/05/2018-State-of-the-mining-industry-2018-report-prospects.pdf (accessed 6 Sept. 2019).

58 Sibanda, M. (2019), ‘How Zimbabwe’s New Fiscal Regime Impacts On Mining Sector’, African Mining Brief, 20 August 2019, https://africanminingbrief.com/how-zimbabwes-new-fiscal-regime-impacts-on-mining-sector/ (accessed 26 Sept. 2019).

59 Stedman, A. and Green, K. P. (2018), Fraser Institute Annual Survey of Mining Companies 2018, https://www.fraserinstitute.org/sites/default/files/annual-survey-of-mining-companies-2018.pdf (accessed 6 Sept. 2019).

60 Chamber of Mines of Zimbabwe (2018), State of the Mining Industry 2018 Report.

61 Hubert, D. (2016), Government Revenues from Mining: A Case Study of Caledonia’s Blanket Mine, Publish What You Pay Zimbabwe, http://www.res4dev.com/wp-content/uploads/2017/06/Blanket_Mine_Zimbabwe_Report.pdf#targetText=The%20Government%20of%20Zimbabwe%20does,companies%20provide%20to%20their%20investors.&targetText=Gold%20is%20now%20Zimbabwe’s%20leading,nearly%2014%25%20of%20industrial%20production (accessed 6 Sept. 2019).

62 Njini, F., Marawanyika, G. and Squazzin, A. (2019), ‘Zimbabwe to Scrap Platinum and Diamond Mine Ownership Rules’, Bloomberg, 6 March 2019, https://www.bloomberg.com/news/articles/2019-03-06/zimbabwe-to-scrap-local-mine-ownership-rule-to-boost-investment (accessed 26 Sept. 2019).

63 However, a ‘race to the bottom’ cutting of taxes and royalties to attract investors may be counterproductive. The industry is currently experiencing pressure from rising tax regimes and resource nationalism elsewhere on the continent that have occurred because tax frameworks were initially set too low, in order to attract investment, and then rose considerably after production started.

64 Hubert (2016), Government Revenues from Mining: A Case Study of Caledonia’s Blanket Mine.

66 New Zimbabwe (2018), ‘Victoria Falls airport set for US$200m upgrade’, 18 February 2018, https://www.newzimbabwe.com/victoria-falls-airport-set-for-us200m-upgrade/ (accessed 1 Oct. 2019).

67 Zimbabwe Futures 2030 roundtable series.