Prices in the energy sector have fluctuated considerably since early 2020, primarily as a consequence of the restrictions on movement and economic activity that were enacted by many governments to limit the public health impacts of the COVID-19 pandemic. As far fewer people commuted to work and restrictions were placed on international travel, demand for transport fuels fell, as did the price of oil. At the start of 2020, prior to the pandemic, oil was $67 per barrel; it fell to $17 per barrel at the start of April and rose to $50 per barrel by the end of 2020 and to $78 per barrel by the end of 2021.

In early 2022, as concerns grew over Russian engagement in Ukraine, the oil price rose sharply. By 24 February it had surpassed $100 per barrel, and two weeks into the conflict, on 9 March, it peaked at $128 per barrel. Natural gas and coal prices followed similar trajectories at the start of the pandemic-induced global economic recession, as demand from factories slowed, and prices again rose at the start of 2022 due to geopolitical and market concerns. As tensions grew, it was noted by the International Energy Agency (IEA) that Gazprom had exported about 25 per cent less gas to Europe in the last three months of 2021 than in the same period of 2020.

Prior to the invasion of Ukraine, governments were preparing to respond to higher energy prices, which were having a serious impact on household income and rendering energy increasingly unaffordable for a growing percentage of the population – even in relatively wealthy OECD member countries. At the end of 2021, the World Bank noted that ‘the surge in energy prices poses significant near-term risks to global inflation and, if sustained, could also weigh on growth in energy-importing countries’.

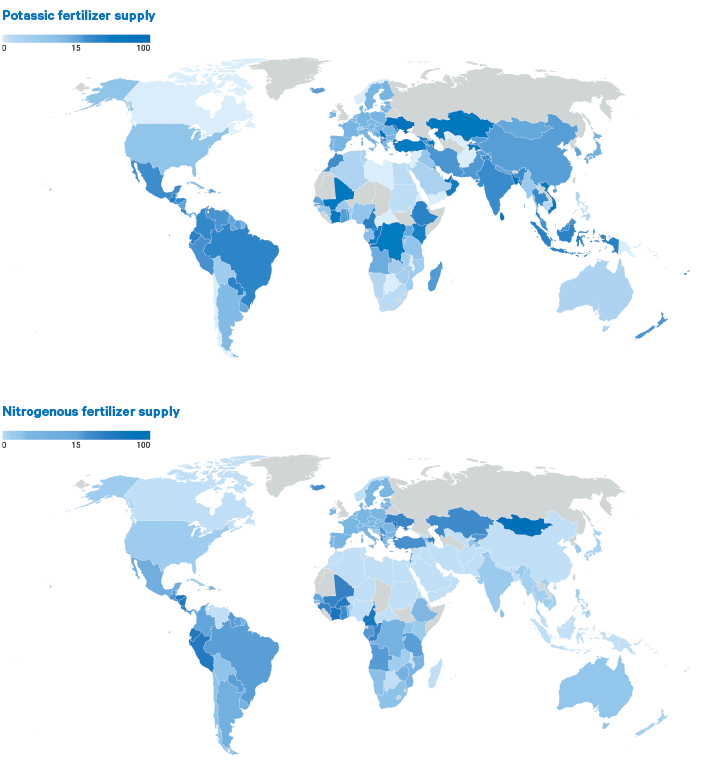

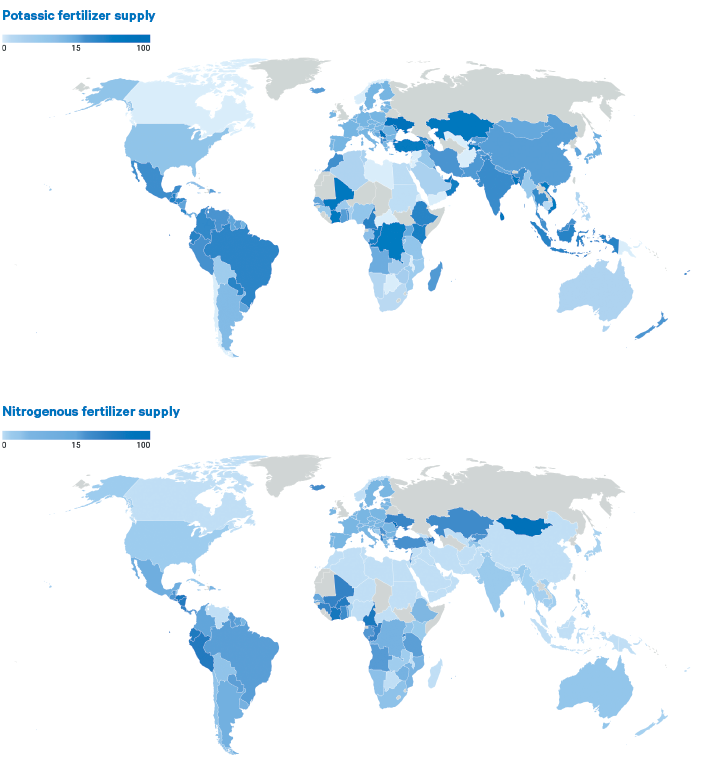

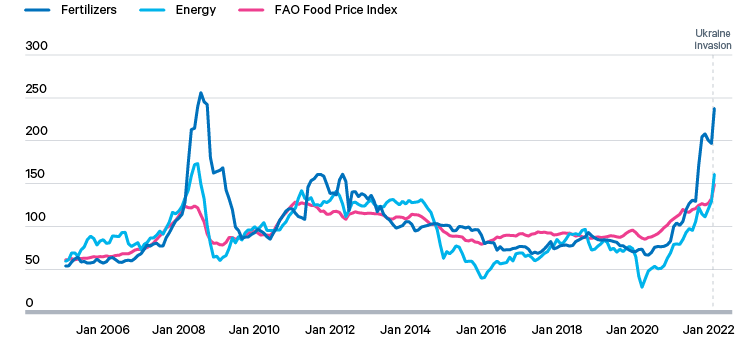

Fertilizer prices had been rising hand-in-hand with energy prices throughout 2021, but took off in October to reach their most elevated level for 13 years (Figure 2). The same fundamental drivers of energy prices applied to the fertilizer sector (given the high energy requirements of nitrogenous fertilizer production), with additional constraints on supply arising from trade policy measures taken by individual countries. China, for example, suspended fertilizer exports – it is a major exporter of phosphate-based fertilizers – in July 2021 until June 2022 to ensure domestic availability, Russia announced restrictions on exports of nitrogenous and phosphate-based fertilizers for six months from December 2021, and sanctions had already been imposed on the state-owned Belarusian potassic fertilizer supplier Belaruskali by Canada, the EU, the UK and the US. Supply constraints and price pressures could significantly curtail fertilizer use in forthcoming planting seasons, especially in the most price-sensitive markets.

Global food prices were already experiencing their sharpest and most sustained increases since the 2007–08 and 2010–11 food price crises, well before conflict concerns were being priced in. At the end of 2021 they were very close to the previous all-time highs of 2011; by February 2022 this peak had been exceeded. While this trend reflects generalized price increases across all food commodity types, meat prices have remained relatively stable and prices for vegetable oils have shown the most dramatic increases.

Global food prices were already experiencing their sharpest and most sustained increases since the 2007–08 and 2010–11 food price crises, well before conflict concerns were being priced in.

Unlike the previous food price crises, which were driven by initial supply constraints and subsequent trade restrictions, the marked increases of early 2022 have largely reflected demand recovery from the early stages of the COVID-19 pandemic and the associated logistical challenges. The stranding of empty shipping containers in Europe and the US in early 2020, during a period of global lockdowns, had slowed supply chains and increased the cost of shipping when Western consumer demand for Asian goods recovered; rising energy prices have fed into agricultural input prices, and increasing demand from the biodiesel sector has also directly contributed to the rise in prices for vegetable oils; recovering demand for grain from China has also contributed, as the country has sought to restore reserves to support the restructuring of its agricultural sector following the 2018–19 outbreak of African swine fever. Planting of crops (for harvest in the summer of 2022) has, in part, responded to higher prices on forward markets. The US Department of Agriculture estimated that the acreage of wheat planted in the US would increase by about 3 per cent in 2022. Whether this mitigates any of the risks discussed in Chapter 4 depends on multiple issues, including the availability of fertilizers during the coming months of the northern growing season, the subsequent southern planting season, the weather, and the capacity to transport harvested grain to where it might most be needed.

The energy transition and its ramifications for Russia

Calls have strengthened from many quarters over the past two decades for the transformation of economies and societies to a more sustainable model of development that tackles some of the fundamental issues contributing to recent crises. Chief among these are systemic inequities and human-driven climate change. Momentum has been building for a shift away from fossil fuels, in particular, and for more sustainable production and consumption of resources more generally, including within food systems.

For Russia, global efforts to realize more sustainable economies pose an existential threat to its own vision for economic growth. Ahead of the UN Framework Convention on Climate Change’s 26th global summit (COP26) in 2021, pledges from over 130 countries – together responsible for around 88 per cent of global greenhouse gas emissions – to achieve net zero by the middle of the 21st century signal an imminent decline in demand for Russian energy. Success in driving emissions down and meeting the collective target of limiting global temperature rise to 1.5°C above pre-industrial levels – as enshrined in the 2015 Paris Agreement – will require an accelerated reduction in the use of fossil fuels in the near term, a longer-term restructuring of global energy markets, the shifting of economic rents and a more diverse energy mix.

Net importers will need to find ways to transform into more sustainable economies while avoiding the social risks of more expensive energy (and food). The EU has been strident in its commitment to the energy transition, but in the process it has increased its dependence on Russian energy, as domestic production has declined and investment in renewable energy has continued to be insufficient. Given the significant transition away from fossil fuels required to adhere to the Paris-aligned pathways, European dependence on Russia’s resources is potentially temporary, but is currently as great as it has ever been.

As the world looks ahead to projected growth in demand for food, land is also becoming an increasingly strategic asset. Russia may well have factored Ukraine’s fertile land into its decision to invade as a means of bolstering its future agricultural power; other neighbouring allies, particularly Belarus and Kazakhstan – major exporters of potash and wheat, respectively – may further add to its sphere of influence if they choose to align with Russia in any future economic war. In the face of the energy transition and declining fossil fuel export revenues, Russia will be looking with urgency for ways to maintain its economic and political power; the current situation shows that no strategy is off the table, whatever the consequences in terms of Russia’s ostracization by the international community.