Some of the resulting dynamics have been seen recently in the spat between Lithuania and China over Lithuania’s recognition of the Taiwanese representation in Vilnius. China retaliated with economic measures, and threatened others doing business with Lithuania. Although the EU did file a case against China at the World Trade Organization (WTO), the initial response from the German business lobby was to put pressure on Lithuania to reconsider its actions.

There are also clear differences within countries. Those EU member states that are most deeply integrated with the Chinese economy, like Germany, remain hesitant to take a more confrontational approach. While the US approach generally has been confrontational, including under President Biden, the American financial sector is one of the main examples of an industry actually increasing its exposure to China. The market opportunity in China remains large enough to create divisions between those in Europe and the US seeking to profit from it and those looking to push back for either economic or political reasons. Often this is seemingly strategically driven by Chinese policy, as the Chinese government in recent years both opened its financial sector for US firms and reduced joint-venture requirements in the automotive sector; the latter with the intent of attracting German carmakers to invest even more in China.

In the realm of economic policy, and the economic challenge posed by China, the differences between the transatlantic partners are in the perceived scale of that challenge but also in how Europe sees itself in relation to both China and the US. Although the EU has begun talking about China as a ‘systemic rival’ as relations with China have moved up the agenda, it has mainly responded with a series of relatively small policy interventions, aimed at reducing or removing distortions to the level playing field in its single market. These measures have included, for example, investment screening mechanisms, rules on public procurement, a stronger focus on industrial policy and pursuing concessions from China on reciprocal market access. In contrast, for the US, the rivalry with China has become almost a defining feature of its policymaking. Although economic decoupling has become a less overt objective under Biden, policy has not changed to any significant degree compared with the Trump administration.

Differing attitudes on both sides of the Atlantic towards the future of the global economic governance system form another major obstacle to a more coordinated transatlantic response to the economic challenge from a rising China. While the EU has sought to sustain the global multilateral trading system, the US has put it under pressure by undermining the WTO’s dispute settlement system. A similar split has been visible over how to engage with China through multilateral financial institutions and the extent to which both the EU and the US have been willing to engage with new, often China-led institutions such as the Asian Infrastructure Investment Bank (AIIB). The BRI has also proved contentious, with some European countries – mainly in Central and Eastern Europe – actively engaged with the initiative. In contrast, the US has sought to engage European partners in its own competing initiatives, such as the soon to be rebranded Build Back Better World (B3W) Partnership.

Transatlantic cooperation in many of these areas is as difficult to achieve as a broader European strategy. This is because European thinking is often defined as aiming to achieve economic sovereignty not just in relation to China, but also the US. In many ways, this stance is not dissimilar to US policies aimed at bolstering ‘America First’, but within Europe internal competition between member states adds a further layer of complexity.

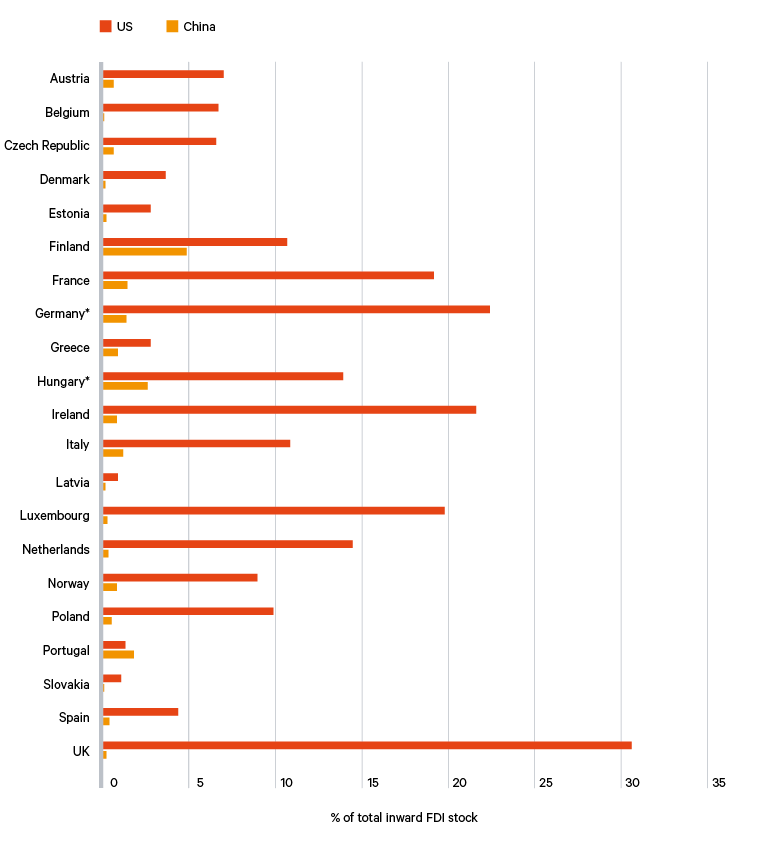

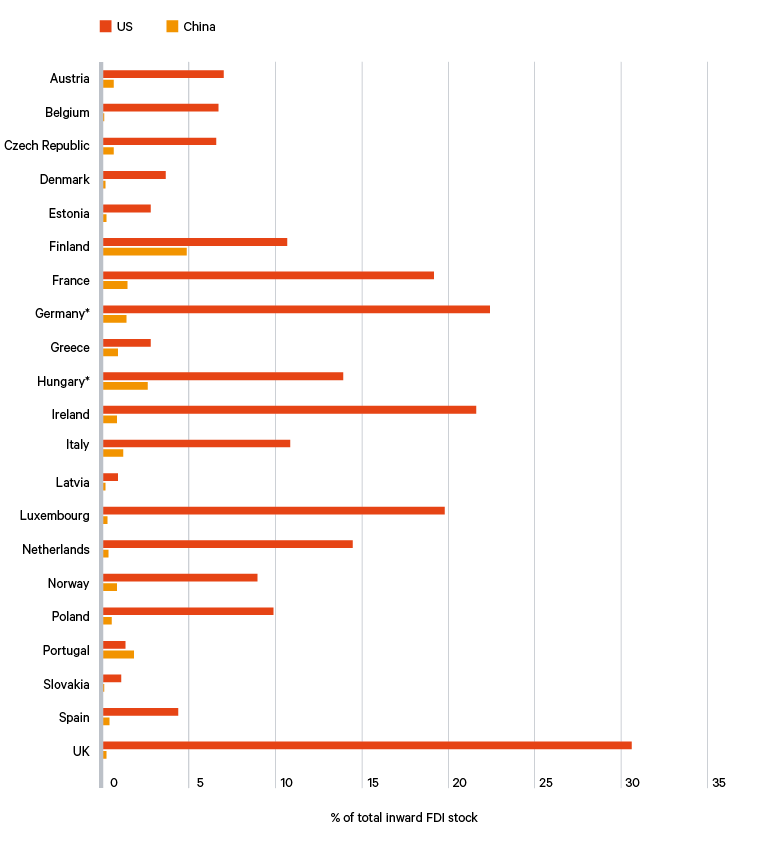

Beyond being significantly closer to each other in terms of values, Europe and the US are also more deeply economically interlinked than China is with either party. Although both the US and the EU import significant amounts of goods from China, other measures of economic interconnection show a much stronger transatlantic bond. For instance, despite a significant increase in Chinese investment in Europe during the past decade, the amount of inward investment in the continent from China is still dwarfed by that from the US (see Figure 2).