Public debt in advanced economies has reached such elevated levels that it poses a serious threat to long-term growth and stability. In 2023, general government gross debt (public debt) exceeded $68 trillion – or 111 per cent of gross domestic product (GDP).

Average total debt in advanced economies, including households and business sectors, now exceeds an unprecedented 250 per cent of GDP, compounding vulnerabilities associated with public debt such as increased financial market volatility, structurally slower growth and higher interest rates.

Public debt ratios have increased since the 1990s without major consequence and influential voices have contributed to a benign view on public debt. Combined with the political obstacles to fiscal consolidation, it seems likely that the now more critical debt levels will again not be prioritized by the G7.

How did we get here?

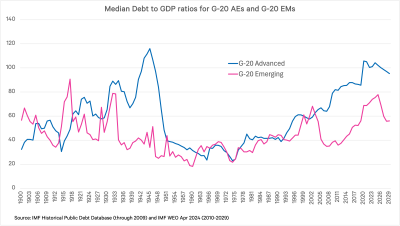

In the post-war period, high growth, higher than expected inflation, a shift to primary fiscal surpluses (total revenue less non-interest expenditure) and financial repression combined to deliver dramatic declines in public debt to GDP ratios in advanced economies.

The UK’s debt ratio fell from 270 per cent in 1946 to 73 per cent in 1970 (and a historic low point of 29 per cent by 1990). The US debt ratio fell from 121 per cent in 1946 to a near-historic low of 36 per cent in 1970.

The inflection point for G7 debt ratios was the 1970s, with a shift to primary fiscal deficits (expansions in welfare not fully funded by tax revenue), accompanied by slower growth and inflation. (Nominal GDP growth fell from more than 10 per cent during 1950–70, to less than 3 per cent during 2000–20.)

Combined with financial liberalization, and real interest rates turning positive in the 1970s, debt ratios climbed by around 20 percentage points between 1990 and 2007.

Median debt to GDP ratios for advanced and emerging economies.

The 2007–09 global financial crisis and the COVID-19 pandemic led to advanced economy debt ratios increasing dramatically, due to stimulus, bailouts and slower growth. Ultra-easy monetary policy (until 2022) allowed debt-servicing burdens to remain contained even as debt levels increased sharply.

Fiscal policy asymmetry, or ‘the ratchet effect’, also became prevalent in advanced economies – stimulus in bad times has been far easier to implement politically than fiscal consolidation in good times.

Why should advanced countries care about high debt?

IMF forecasts suggest that average G7 debt ratios will increase over the medium term. The US Congressional Budget Office forecasts the US debt ratio will continue to increase long term, driven by debt servicing.

Substantial fiscal pressures are looming – ageing/shrinking populations, climate change, geopolitical conflicts leading to higher defence spending. So too are huge contingent liabilities (such as crisis risks related to overall debt, climate-related costs and underfunded social security and pension commitments).

According to one (perhaps prevailing) view, advanced economy debt ratios at current levels are not a concern. Broadly, it argues that as nominal GDP growth exceeds interest rates on government debt, debt ratios can decline even in the context of primary deficits. Paul Krugman is of this view, which was bolstered in 2019 by Olivier Blanchard’s influential American Economic Association presidential address.

But economic history and the academic literature suggest that advanced economy debt ratios, at these elevated levels, are a real concern. They create vulnerabilities to crises (such as the euro area debt crisis); increase fragility (notably the reaction of gilt yields to the UK’s Truss–Kwarteng mini-budget in September 2022); and are associated with structurally slower growth and higher interest rates.

Some academics (including the oft-cited, if controversial work by economists Reinhard and Rogoff) find that GDP growth is slower once public debt goes above a threshold of around 90 per cent of GDP.

Higher interest expenditure on public debt crowds out productive government spending and higher interest rates crowd out private investment. High public and private debt ratios increase the risk of a financial crisis (and large permanent output losses), macro-instability, higher inflation (if debt is monetized), and lower policy flexibility (associated with limited fiscal space and fiscal dominance of monetary policy).

How advanced economies should address public debt overhangs

Reducing the debt to GDP ratio can be achieved through combinations of fiscal consolidation, growth, inflation, financial repression and debt restructuring. The optimal consolidation path, strategy and target debt ratio will depend on each country’s starting conditions (its initial debt ratio and scope for absorbing public debt, higher taxes, expenditure cuts, and so on).

The consolidation path will have to be clear, credible (to anchor expectations when shocks hit) and gradual (to avoid derailing recoveries or growth). This implies high public debt ratios will likely be with us for some time.

Most forecasts of G7 growth are flat to declining over the medium term. Some hope that growth picks up in the context of AI and that this could help accelerate the decline in debt ratios. Yet Robert Solow’s 1987 quip rings true here: ‘you can see the computer age everywhere but in the productivity statistics’. An AI-related productivity boost may be a decade away.

High inflation since late 2021 (and the sharp rebound in GDP) has contributed to a decline in advanced economies’ debt ratio from 122.4 per cent in 2020 to 111 per cent in 2023. However, attempts ‘to keep surprising bondholders have historically proved futile or harmful’.

Financial repression would be required (in addition to inflation) which would be hard to engineer politically (outside crisis conditions) and would result in costly distortions.