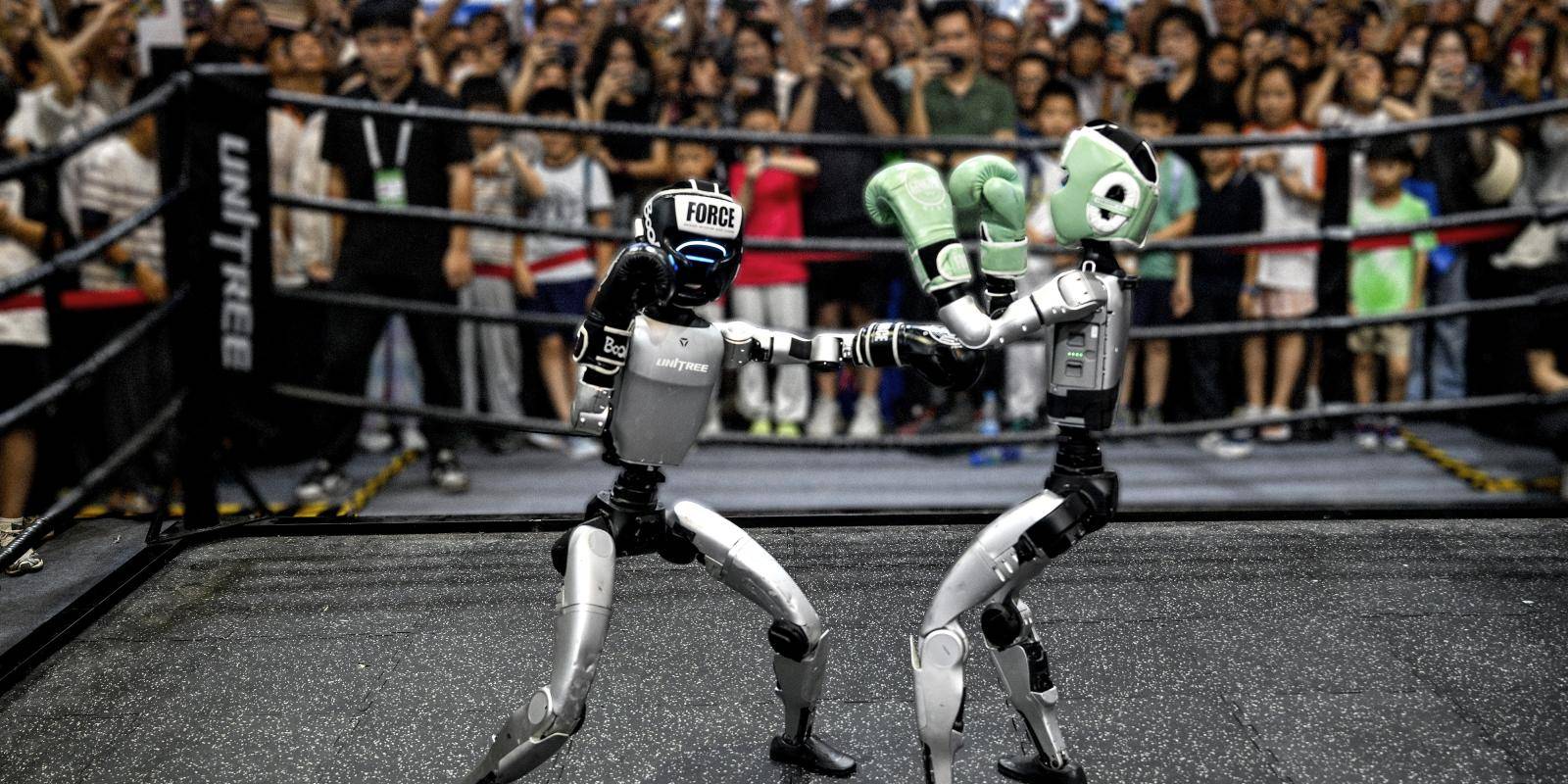

If you had to choose one totem to represent China’s rise to the forefront of global technology, you might pick the Unitree R1 humanoid robot. It can walk, kick, balance, perform a basic range of kung-fu moves and even do cartwheels without falling over. But what makes it a fitting symbol of China’s tech ascendance is its price. The cheapest model costs only $5,900, a fraction of what competitor humanoids made by US companies sell for. Of course, such a price tag is not pocket change, but it does bring it into range for wealthy individuals and corporations, making it the first ‘affordable’ humanoid robot.

This is important because it defines the essence of China’s tech challenge to the West. In industry after industry, product after product, Chinese manufacturers are making cutting-edge technology at prices that western competitors cannot match. A wave of anxiety is sweeping through the boardrooms of famous companies in the United States, Germany, Japan, South Korea, Britain and other countries in the West as executives confront the loss of their technological lead to fast-moving, high-tech Chinese competitors.

The soundtrack to such a sea change is a chorus of panicked utterances from the bosses of well-known companies in the West. ‘It’s the most humbling thing I’ve ever seen,’ said Jim Farley, Ford’s chief executive, after a visit in July 2025 to China left him astonished at the technological advances being incorporated into Chinese cars. ‘Their cost and the quality of their vehicles is far superior to what I see in the West,’ he said. ‘We are in a global competition with China, and it’s not just electric vehicles (EVs). And if we lose this, we do not have a future at Ford.’

Jensen Huang, chief executive of Nvidia, the world’s most valuable company, said in November that ‘China is going to win the AI race’. He later added: ‘It’s vital that America wins by racing ahead.’ Brad Smith, president of Microsoft, said in late 2024 that there was a perception gap in the West with regard to Chinese technology. ‘I think one of the dangers, frankly, is that people who don’t go to China too often assume that they’re behind.’

Andrew Forrest, founder of iron ore giant Fortescue, dropped plans to make motors for electric mining trucks in Britain and said his company will instead make them in China, where costs are much lower and delivery times faster. ‘We’re building up our research in Oxford, but we’re making sure that manufacturing is done wherever it’s most efficient,’ he said.

Such remarks reveal a deep sense of foreboding among the corporate chieftains of the West at the reordering of the world’s technological tectonic plates. History shows that technology is often destiny. The Islamic Golden Age was accompanied by advances in mathematics, medicine and astronomy. When America overtook Britain in the late 1800s as the world’s leading tech power, it presaged the rise of the United States as the global superpower.

Auguries for an era of Chinese dominance are now clear. Researchers at the Australian Strategic Policy Institute have found that China has surpassed the US in cutting-edge research for 57 out of 64 technology areas. Reinforcing such findings, the Information Technology and Innovation Foundation (ITIF), a Washington-based technology think tank, analysed 10 advanced tech sectors and found that China is ahead or ‘near’ the world leaders in six of them.

An electric vehicle automated production line at the NIO factory in Hefei, in China’s Anhui province. Photo: Jade Gao/ AFP via Getty Images.

In terms of intellectual property, the picture is similar. The World Intellectual Property Office found that in 2023 China ranked first among total patents issued, followed by the US in a distant second place with Japan and South Korea in third and fourth. China overtook the US in the 2023 Nature Index, which tracks data on author affiliations in the world’s leading scientific journals, and then extended its lead in 2024. ‘China’s rate of progress in production and innovation across a wide range of industries is striking,’ wrote ITIF analysts Robert Atkinson and Stephen Ezell.

Accusations of intellectual property theft have accompanied China’s ascent. In 2023, the intelligence agency bosses of the ‘Five Eyes’ countries – the US, UK, Canada, Australia and New Zealand – came together to accuse China of widespread intellectual property theft. Christopher Wray, then director of the FBI, said China represented an ‘unprecedented threat’ and was stealing secrets in sectors such as quantum computing, robotics, biotech and artificial intelligence (AI). In response, Liu Pengyu, a Chinese government spokesman, said the country was committed to intellectual property protection.

Mass production drives innovation

Humanoid robots are emblematic of China’s emergence in a number of ways. Speed is one. Until recently, few people had heard of Wang Xingxing, the founder of Unitree Robotics. His first product – a quadruped robot called Go1 – was released in 2021.

At that time, Unitree was lagging behind Boston Dynamics, one of the US’s leading robot makers. Boston Dynamics had brought out ‘Spot’, a quadruped robot, in 2015. But by this year, it became clear Unitree is now a peer competitor to Boston Dynamics’ most advanced humanoid, ‘Atlas’. Like the Unitree R1, Atlas can do a range of moves, including cartwheels.

It is hard to know which of the two companies will eventually pull ahead but Unitree has one sizable advantage. In 2025 it moved into mass production along with several other Chinese robot makers, which were due to make thousands of humanoids during the year. The demand this generates among suppliers of robot components is expected to deliver economies of scale, thus driving down the costs of humanoids and seeding a potentially mass market. Such dynamics are already in play: the latest humanoid produced by Noetix Robotics, a Beijing-based company, sells for only $1,370. Called Bumi, it is not as advanced as the Unitree R1, but it is intended to appeal to home users, according to the company.

The reason why the shift to mass production is transformational is because the root of China’s competitiveness resides with its supply chain. It is possible to source almost every component in the world in China – and at prices that routinely undercut producers elsewhere. Mass production – and thereafter the creation of a retail market – also allows Chinese manufacturers to generate a revenue stream which, in turn, finances the R&D

required for the next iteration of their product. In the case of Unitree, this may hasten the arrival of what Wang Xingxing describes as a ‘ChatGPT moment’ for robots.

This moment, as defined by Wang, will be when a humanoid robot can complete a complex task for which it has not been preprogrammed. This might be cleaning a room that it has never entered before or serving someone in an unfamiliar venue. When this happens it will be a game-changer, industry experts say, because it will mean that humanoids can be genuinely useful in a number of different settings. ‘If things develop fast, it could happen in the next year or two, or maybe two to three years,’ Wang said.

Europe’s car brands overtaken

Supply chain superiority, assisted by mass production, cost cutting and hefty R&D spending lie behind China’s tech emergence. When the technology produced by this vortex of factors arrives in foreign markets, the result is often disruptive to incumbent brands. The most striking example of this is electric vehicles. Chinese brands led by BYD have gone from being also-ran exporters of vehicles in 2020 to the world’s leading exporters, offering high-tech EVs at significant discounts to European and US brands. This has meant that brands such as BYD, Chery, SAIC, MG and Leapmotor are fast gaining name recognition in the West. In Europe, BYD registered a 304 per cent increase in year-on-year sales in the first nine months of 2025, while Chery notched up an 862 per cent rise and Leapmotor, which makes ultra-affordable cars, posted a 7,108 per cent increase.

For European competitors, the impact of Chinese competition has been harsh. Car companies Volkswagen, Audi, Ford and Daimler Truck shed 90,000 jobs in the past year. Bosch, Continental, Schaeffler and ZF Group, all of which supply high-tech motoring components, have shed another 25,000. The share prices of VW, Mercedes Benz, Stellantis and other European carmakers are sharply down, as investors analyse the chances of survival for brands which have for decades been household names.

Carlos Tavares, former chief executive of Stellantis, warned last month that as western carmakers stumble, Chinese competitors will be ready to snap them up. ‘The day a western carmaker is in severe difficulty, with factories on the verge of closing and demonstrations in the street, a Chinese carmaker will come and say “I’ll take it and keep the jobs,”’ Tavares said.

It may be that the story of MG, a venerable UK brand, foreshadows an element of the future for some European car makers. The bankrupt MG Rover was bought by Nanjing Automobile in 2005 for a mere £53 million. Subsequently, Nanjing Automobile was acquired by the state-owned SAIC in China and the reborn brand is now one of the best-selling EVs in Europe.

Other sectors mirror Chinese EVs

Every sector under threat from the disruptive surge in Chinese competition is different. But in varying degrees, a similar dynamic to that seen in EVs is visible in pharmaceuticals, batteries, wind power, solar power, 5G telecoms equipment, factory automation, cellular modules, electrical equipment, shipbuilding and others. In all cases, the competitiveness of the Chinese supply chain, married with innovative products created by indigenous R&D, lies behind China’s success in producing high-tech products at unbeatable prices. For foreign competitors to emerging Chinese companies, the impact can be as unexpected as it is palpable. Merck and Co, a large US pharmaceutical company, saw its share price plunge on a few occasions in 2024 and early 2025 due to the declining sales in China of its drug, Gardasil, used to prevent diseases caused by the human papillomavirus.

The impact the company sustained came from an unheralded source. Xiamen Innovax Biotech, a Chinese company little known in the West, came up with Cecolin 9, which sold at a 60 per cent discount to Gardasil, yet performed just as well in trials. The implications of this are considerable. The uncomfortable truth for western pharmaceutical giants is that these days China makes not only the largest amount of Active Pharmaceutical Ingredients – the precursors for medicines – but it is also a leader in R&D for new drugs. AstraZeneca’s decision this year to build a $2.5 billion R&D hub in Beijing shows China as an emerging centre of gravity for the industry.

In solar power, the sun has long set on western industry. China now accounts for 80 per cent of the world’s manufacturing market share for solar panels and this is expected to rise to 95 per cent in coming years, while Europe and North America account for around 3 per cent and 2 per cent respectively. After heavy R&D spending,Chinese-made solar panels now generate the lowest-cost electricity achievable.

In wind power, the fight is on as Chinese manufacturers of wind turbines gain global market share, but western competitors such as GE Vernova, Siemens Energy and Vestas maintain a significant market presence with high-tech turbines. Nevertheless, the challenge that leading companies such as Goldwind, Envision and Mingyang present is that their turbines sell at a hefty discount which can be in the order of 30 to 50 per cent, industry executives said. Shipbuilding shows that China’s prowess includes heavy industry with potential dual-use military and civilian applications. Just over two decades ago, China was a marginal presence in shipbuilding with outdated shipyards run by state-owned enterprises that were overstaffed and inefficient.

But in 2024, China’s share of all newbuild orders rose to a dominant 74 per cent globally, up several fold from two decades earlier and eclipsing South Korea’s shipbuilding giants, according to the China Association of the National Shipbuilding Industry. Much of the new technology being deployed is devoted to powering ships by using green power, such as batteries, hydrogen fuel cells and liquified natural gas.

Overcapacity and ‘involution’

Although many in the West have been too slow to see it coming, it is clear that the era of China as the world’s leading tech power has arrived. Two crucial questions arise. Is it sustainable? And what can the West do about it?

The question of sustainability generally agglomerates around an unusual word – ‘involution’ or neijuan in Chinese. This means excessive, ruinous competition among too many manufacturers that leaves profit margins wafer thin or negative. Some Chinese tech companies have been loss-makers for years, yet state-owned banks keep bankrolling them. At the central government level, China makes no secret of its dissatisfaction with involution. Xi Jinping, China’s leader, used a high-level meeting in July 2025 to rail against ‘destructive discounting’ and ‘unproductive outcomes’ that were behind the country’s persistent deflation for manufactured goods.

If Beijing’s campaign against involution brings at least a measure of success, then the profit margins achieved by tech companies are likely to rebound. Early signs suggest some progress: in the third quarter of 2025, the earnings of China-listed companies rose 11.6 per cent from a year ago, compared with a 1.2 per cent increase in the second quarter and a 3.2 per cent lift in the first quarter. Technology companies led the way, with Cambricon Technologies – an AI chipmaker often regarded as China’s Nvidia – reporting a 14-fold jump in revenue. The impact on the West from low-price but high-tech Chinese products is therefore likely to continue. Thus, policymakers in the West need to decide, with dispatch, what to do now that the Chinese dragon is on their doorstep.

What should Europe do?

The US has adopted a series of policies aimed at combating China’s technology competition, including restricting Chinese companies on the US ‘entity list’ from gaining access to US technology, particularly advanced semiconductors. Sanctions, tariffs and other controls have formed other aspects of the US response. It is now clear that these approaches, although effective in hampering the operations of Chinese companies such as Huawei, have not restrained China’s emergence as a tech power. Indeed, the indigenization of Chinese technology, which drew impetus from the US controls, is now a guiding principle.