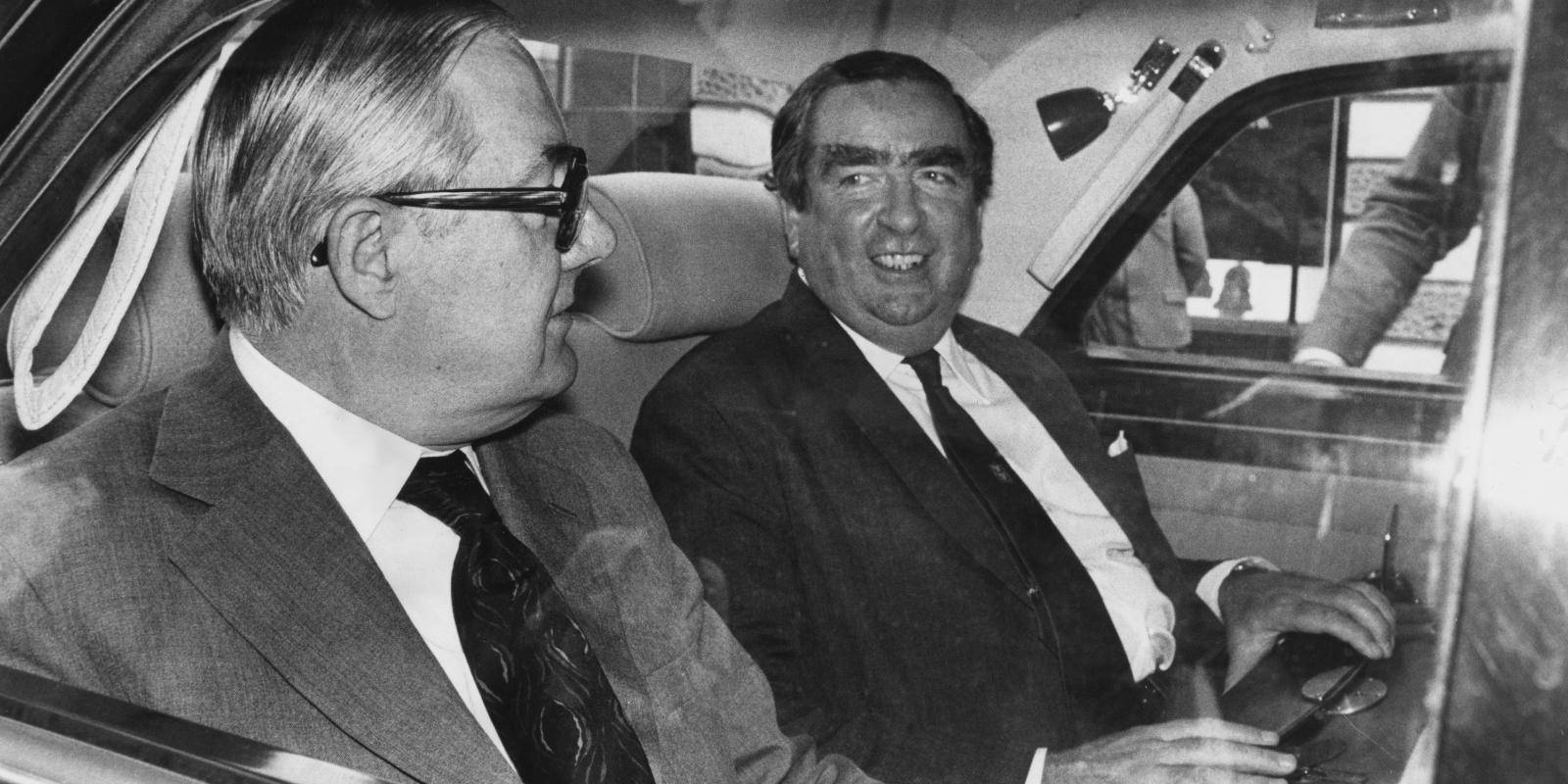

The most potent symbol of Britain’s 1976 economic crisis was the sight of Chancellor Denis Healey turning back at the airport as the pound plummeted. The next day he announced that Britain would be applying to the IMF for a huge loan. And on December 15, 1976, he signed a Letter of Intent to the IMF, committing to significant public expenditure cuts in return for a $3.9 billion loan.

The value of sterling had fallen from $2 in March 1976 to $1.65 as the Labour Party conference began at the end of September. Jim Callaghan’s government, with a wafer-thin majority of five seats, was struggling with the perennial British post-war weaknesses: a fiscal deficit around 10 per cent of GDP, inflation that peaked at 27 per cent in 1975, and a chronic balance of payments deficit. These were compounded by the ‘sterling balances’ problem and the risk of a run on the pound.